US Conference Board Consumer Confidence Preview: Rising confidence supports the economy

-

Confidence projected to rise toward 12 month average.

-

Retail sales rebounded in October from the first negative month in seven.

-

Labor market remains healthy, jobs, wages and unemployment buoy sentiment and spending.

The Conference Board a private non-profit business group will release its November Consumer Confidence Index on Tuesday November 26th at 15:00 GMT, 10:00 EST.

Forecast

The Consumer Confidence Index is expected to reach 127.0 in November from 125.9 in October. The Present Situation Index rose to 173.2 in October form 170.6 in September. The Expectations Index dropped to 94.6 in October from 96.8.

US labor market and consumer confidence

Employment, wages and the very low jobless rate have been the underpinning of consumer confidence for three years. Despite the occasional weak month, as in January of this year during the partial government shutdown, the 34 months from January 2017 have been the happiest for consumers in almost two decades. In the 52 year history of this survey only the period from May 1999 to December 2001 scores higher in satisfaction.

Non-farm payrolls were at a 3-month average of 176,000 and a 12-month average of 174,000 in October. This is down from 235,000 and 245,000 respectively in January but is well above new entrant rate keeping the labor market tight. Wages have been rising at a 3% or better annual rate for 15 months and the 3.6% unemployment rate is 0.1% from a 50 year low.

The consensus estimates of 183,000 for November payrolls, 3% for annual wages and 3.6% for unemployment and the likely continuation into the first quarter of 2020 is the kind of consistency that has supported consumer confidence for three years.

The consumer economy

Consumer happiness has been expressive.

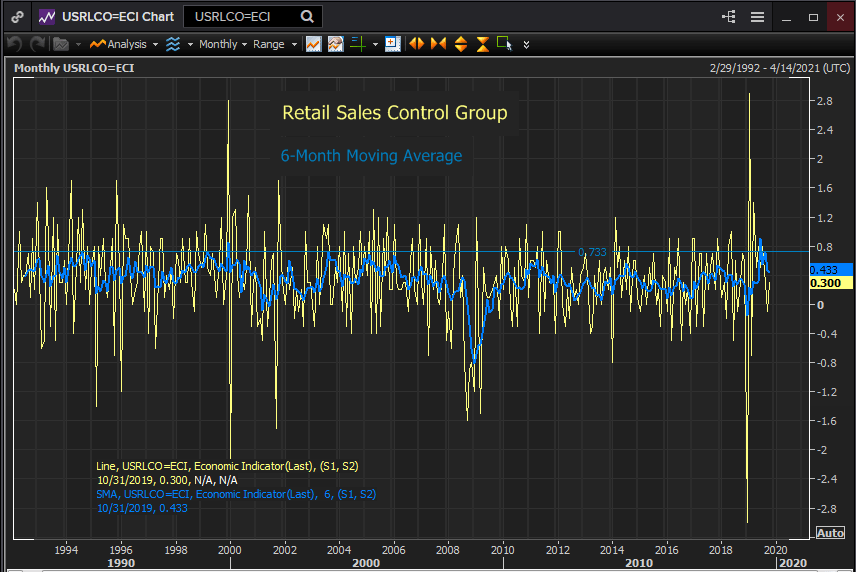

The retail sales control group which is the Bureau of Economic Analysis’ GDP consumption component had a six month average of 0.433% in October and 0.717% in August. Excluding the anomaly of 0.9% in June that was a product of distorted reporting around the January government shutdown that was the best six months for this measure in 16 years.

Reuters

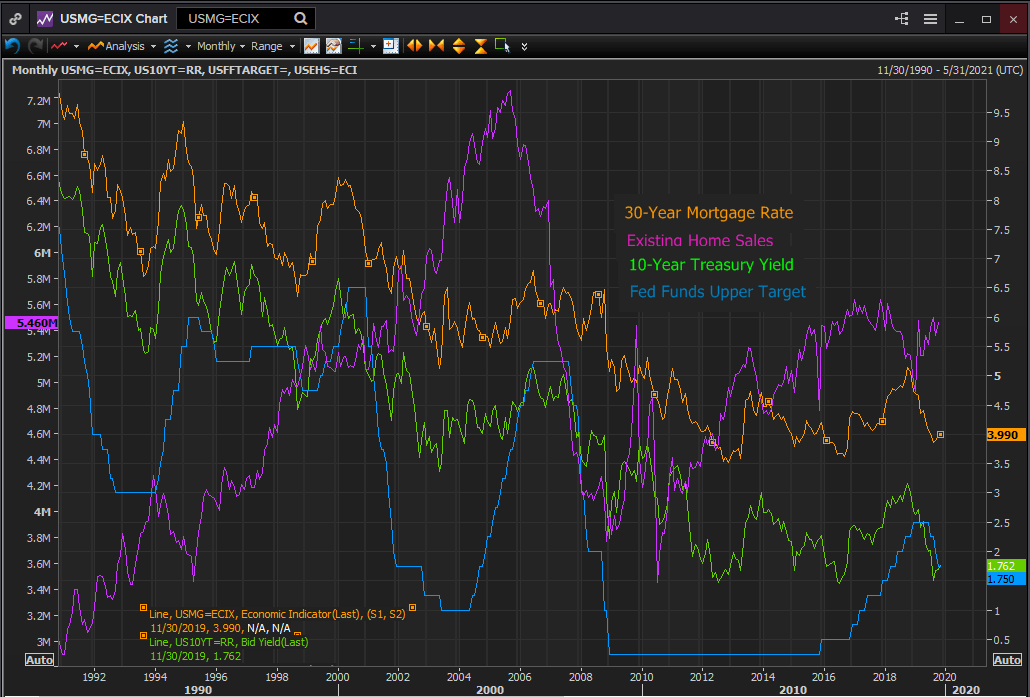

Sales of existing homes, 90% of the US market, have also recovered from their year eleven month slide from an annualized rate of 5.61 million in March 2018 to 4.93 million in January 2019 reaching 5.46 million in October.

Reuters

The decline and return in home sales followed at a two to three month delay the rise of mortgage rates from 4.22% in December 2017 to 5.15% in October 2018 and then back to 3.99% this month.

Home purchases are sensitive to interest rate movements. The rapid recovery of home sales once interest rates had fallen is an indication that the underlying consumer attitude and economy remains strong enough to fund a family’s largest purchase at normal historical levels.

The Fed and interest rates

With business capital spending largely on hold awaiting the denouement of the US China trade argument, the American economy has been carried for more than a year by consumer spending.

The Fed has recognized the resilience of the economy even with one of its main GDP components absent by ending its three month essay into the economic insurance business at the October FOMC meeting. During the three rate cuts it was the potential impact of the China trade war and the global economic slowdown on the US economy and by default the consumer that was chief among the central bank’s worries.

If the consumers had taken their cues from economists rather than their paychecks and cut back on spending the decline in GDP could have precipitated a recession.

Happily sentiment and consumer spending remained robust and growth dropped only to 1.9% in the third quarter.

The Atlanta Fed’s GDPNow model is tracking at 0.4% for the final three months of the year and the New York Fed’s Nowcast estimate is 0.7%.

With the immediate fate of the economy tied to the US consumer any prolonged drop in sentiment could quickly become a growth issue and that would receive swift notice from the data dependent Fed.

The dollar

After three rate cuts which did little to damage the dollar the US economy is set to become the main point of comparison as soon as the China trade dispute is relegated to the background by a signed agreement. The text of the a deal is less important than the de-escalation of trade tensions it represents.

The stronger consumer sentiment is preceding a trade agreement the higher it can go afterwards and the better for the US economy and the dollar.

Conclusion

The labor market continues to supply the consumer with a surfeit of happiness and the consumer continues to spend and keep the US economy afloat. There is no indication that this pleasant state of affairs is ending.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.