US: Bubbling inflation pushes Fed into action

Inflation pressures are broadening and intensifying through every sector of the US economy. At the same time, Covid is waning and activity is rebounding. This heady mix is set to ensure a swift conclusion to the Federal Reserve's QE tapering operation and a growing risk the Fed ends up raising rates more than the two 25bp rate hikes we are forecasting for 2022.

3Q soft patch gives way to stronger growth

The US economy entered a soft patch in the third quarter as the Delta variant of Covid spread across the country and led to heightened caution amongst households. Ongoing supply constraints also hindered economic activity as growth slowed from 6.7% annualised in 2Q to 2% in 3Q.

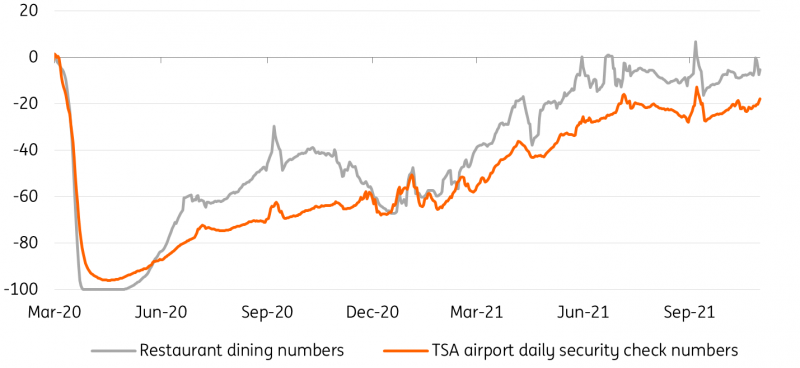

Thankfully, Covid case numbers have fallen sharply since peaking at 200,000 per day in early September. The seven-day average is now down to around 70,000 and we are seeing a rapid rebound in the willingness of consumers to get out and about and spend money. As can be seen below, air passenger numbers and restaurant dining visits are rising once again while hotel occupancy is back up to 64%, having got as low as 60% in September.

Air passenger and restaurant dining numbers - percent change versus same date in 2019

Source: Macrobond, ING

This gives us confidence that the fourth quarter will experience much better growth despite concerns surrounding the increasing cost of living. The combination of strong labour demand amidst a dearth of supply will keep incomes rising while households have the resources to weather this latest storm. After all, nationally their wealth has increased by more than $26tn since the end of 2019, equivalent to $78,000 for every American.

Outside of the household sector, strong capital goods orders point to good prospects for business investment while net trade should be positive given the disruption in Chinese output due to Covid constraints and the long queues of ships trying to get into West Coast ports. At this early stage, we think the US growth story will get back on track with the economy set to expand by 6.5-7% in 4Q.

We are hopeful that strong momentum will continue into 2022 given we expect long anticipated government spending on infrastructure and social policy to eventually come to fruition. Add in more corporate capital expenditure, inventory rebuilding as supply chain problems ease, and the return of foreign visitors in significant numbers, and we feel the economy can expand by more than 4.5% next year.

Inflation pressures get even stronger

This does assume that we see supply chain issues ease and that labour supply starts to increase. After all, schools are back to in-person tuition so parents don’t have to stay home, there is an effective vaccine so Covid anxiety should be waning and the extended unemployment benefits that may have diminished the financial need to get a job have concluded.

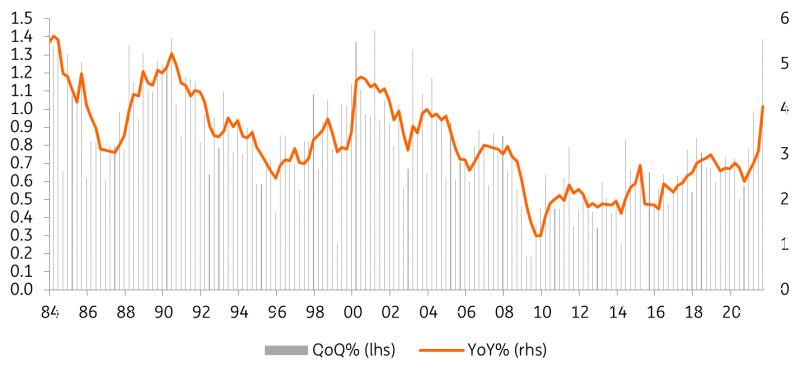

Nonetheless, we suspect wage pressures will continue to build as companies compete for workers in an environment where there are already 10.5 million job vacancies. The quit rate – the proportion of workers quitting their job to move to a new employer – is at a record high, which suggests companies are not only having to pay up to recruit new staff, but also pay existing staff more in an effort to retain them.

US employment cost index (1984-2021) shows labour market costs are soaring

Source: Macrobond, ING

The fact that the latest employment cost index readings accelerated sharply shows that inflation pressures are no longer impacting just the goods sector, but increasingly infiltrating the services sector. With housing costs on a sharp upward trajectory, energy prices moving higher and second-hand car prices getting a second wind on the lack of new vehicles, we now expect headline inflation to break above 6% around the turn of the year with core inflation moving above 5%.

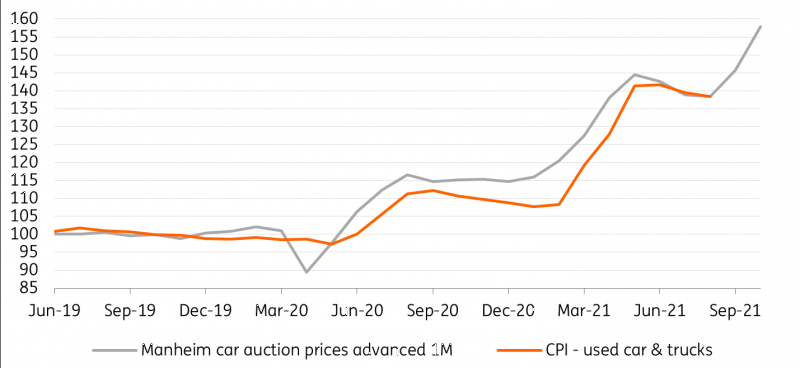

Second-hand car prices to push inflation above 6% – price levels indexed to 100 for June 2019

Source: Macrobond, ING

An early QE end with at least two rate hikes in 2022

With market and consumer inflation expectations looking less and less “anchored,” the Fed’s confidence that inflation is transitory has weakened and the bank has finally announced a taper of its QE asset buying programme. Purchases are set to be reduced by $15b each month, which would mean it is concluded before June. However, given our growth and inflation projections, we see a strong chance of it ending sooner, possibly in 1Q 2022.

We don’t think interest rate increases will be far behind. We continue to forecast two 25bp interest rate moves in the second half of 2022 – one in September and one in December. However, given the evident intensification of inflation pressures, the risks are skewed towards earlier action, which could open the door to the possibility of three hikes next year.

Read the original analysis: US: Bubbling inflation pushes Fed into action

Author

James Knightley

ING Economic and Financial Analysis

James Knightley is the Chief International Economist in London. He joined the firm in 1998 and has been covering G7 and Western European economies. He studied economics at Durham University, UK.