US ADP Payrolls Drop 20 million: And that’s only half the story, NFP is the other

- Private payrolls shed 20.236 million, the prior record was 834,665.

- Markets have become inured to the labor force catastrophe.

- NFP on Friday will be the test for the market acceptance of the employment collapse.

- Dollar and equities should be unaffected if NFP meets forecast.

Private payrolls from Automatic Data Processing didn’t just set a new record in April for the most job losses in one month.

They established a once in a millennium, galactic standard for layoffs. Short of a meteor collision or an atomic war it is hard to imagine an economic scenario with the same instant devastating job losses. Even another pandemic would have a much more measured response, and far less panic.

The point is not to be flippant but to observe that not all information, no matter how egregious, affects markets equally.

Wednesday’s payroll losses were 23 times larger than the previous greatest monthly loss in February 2009 at the height of the financial crisis and recession.

Markets yawned. Old news. Or more accurately, expected news.

The dollar finished the day ahead by small amounts against all the majors except the yen. Equities fell but the first move for the Dow was to shoot to its high for the day three minutes after the 9:30 am open but 75 minutes after the release of the ADP employment report at 8:15 am EDT. The yield on the 10-year Treasury rose 0.052 points to 0.709% its highest return in three weeks.

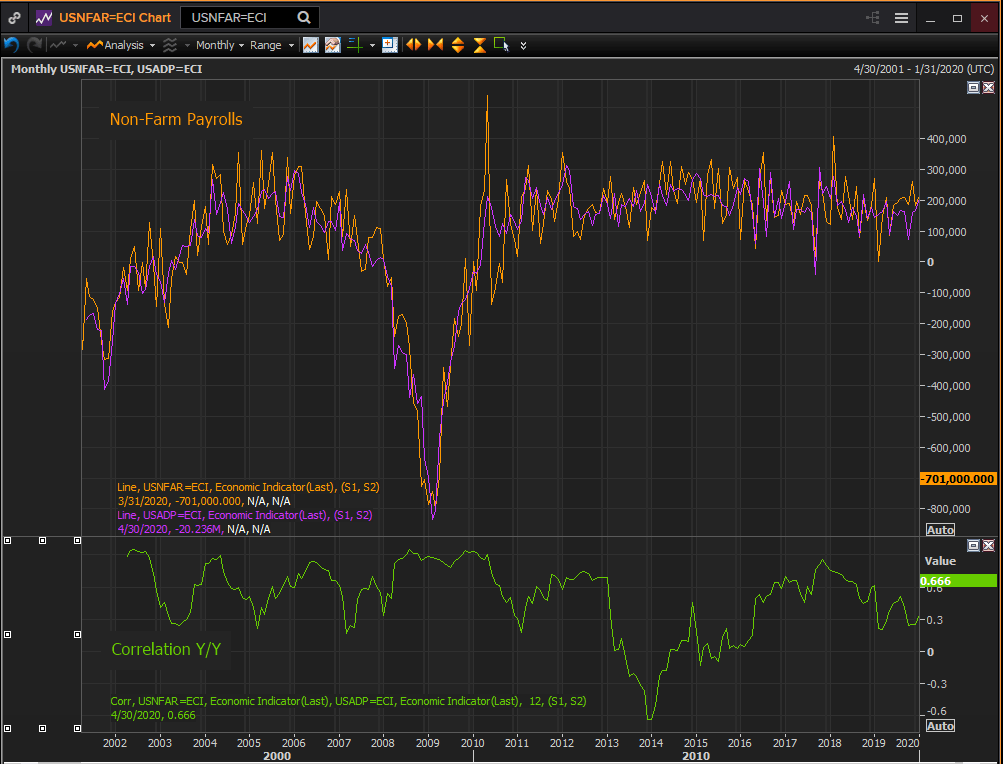

ADP forecast and reality

The consensus estimate for ADP was -20.050 million with a range from -8.79 million to -25 million. The 0.93% miss at -20.236 million was much lower than the 5.93% average forecast understatement on initial claims for the past three weeks or the 2.55% average estimate miss for seven weeks from February 6 to March 19.

ADP Payrolls

There was little reaction because the ADP result was, for market purposes at forecast. The 186,000 discrepancy provided no additional information and did not change the either the depth of the labor market collapse or its potential recovery. Any shock at the astronomically high level of firings has been dissipated by six weeks of jobless claims.

Pricing the pandemic

Equity, currency and credit markets were pricing the economic consequences of the pandemic long before the data description became available.

Credit markets began earliest. The return on the US 10-year Treasury started falling on February 12 with the steepest part of the descent from February 22 to March 9. The Dow began slipping a week later on February 19 with its deepest plunge from March 5 to March 23. Currencies, the US dollar in particular were busy throughout, with the greenback falling and rising in several waves from February 20 to April 4.

The lows in the credit and equity markets came before the first initial claims data confirmed the catastrophic economic impact of the coronavirus closure orders in the US.

The Dow and S&P lows were on March 23. The dollar’s risk aversion high against the euro was on March 19 and versus the yen on March 23. The low yield and high price for the 10-year Treasury was on March 9 at 0.498%. The first of the ascending initial claims reports arrived on March 26.

ADP and NFP forecasts

The ADP April forecast was extrapolated from initial claims data and did not suffer from the informed guesswork of the first two coronavirus estimates for March 20 and 27. The consensus prediction for the NFP number on Friday should have the same accuracy. With variations for the different categories and criteria used, the ADP, NFP and claims numbers are all packaging the same information.

Though the size of the April NFP payroll losses will be beyond anything markets have experienced in the past, the forecast is -21.853 million, it will not be a surprise. The wholesale and perhaps unnecessary destruction of employment is an economic tragedy for the United States and a personal one for the millions of people and families without income, but it is no longer has the ability to shock markets.

Reuters

Trading non-farm payrolls

There are few economic situations without precedence. This labor market is one. Or it was until the last two weeks of March when the initial claims numbers exposed the extent of the disaster. After 30 million layoffs the April ADP and NFP results are simply confirmation.

Market interest has moved to the future, to the incipient restart of the US economy and the re-employment of the labor force.

The trading dynamic for economic statistics is the tension between the forecast, which is known and priced into trading levels and the reality of the data. Surprise and difference drives movement not the absolute size of the number.

Non-farm payrolls are the premier US economic release and the market favorite but its information about April has long since been priced into the markets.

If the NFP forecast is accurate markets will react as they did for ADP, as they do for almost all expected information and do little or nothing. Do not expect nostalgic horror.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.