US ADP Employment Preview: Good numbers, weakening trend

- August private payrolls expected to be at trend

- Job averages have declined this year

- The China US trade dispute is at the center of the slowdown

Automatic Data Processing (ADP) the private payroll company will release its National Employment Report on Thursday September 5th, at 12:15 GMT, 8:15 EDT.

Forecast

The business clients of ADP are expected to hire 148,000 new employees in August after adding 156,000 in July and 102,000 in June.

FXStreet

ADP and NFP

The ADP report is a precursor to the Bureau of Labor Statistics (BLS) Employment Situation Summary commonly called non-farm payrolls (NFP) for its most widely cited jobs statistic.

The ADP figure is issued on the Wednesday or Thursday before the NFP report which is slated for Friday September 6th at 12:30 GMT, 8:30 EDT.

The NFP report is the most widely quoted and analyzed US statistic. It provides the most complete coverage of the American labor market including job creation and payrolls, wages, unemployment, labor force participation, average work week and several other topics. It took on added importance in the wake of the huge jobs losses during the financial crisis and recession of 2008-2009.

The BLS information is organized into a number of categories--private and government payrolls, type of employment, age, racial and gender differentiated unemployment rates and many alternatives. In all the BLS report contains 25 different tables of employment statistics.

ADP and NFP: Part and Whole

The ADP and NFP reports both list current payrolls and track the increase or decrease from the prior month.

There are three main differences between the reports. The ADP information is limited to the payrolls of its 411,000 US clients. The BLS report covers the entire American economy including government employment at local, state and federal levels.

The ADP report is essentially a one topic brief for current payrolls. The BLS assessment charts an extensive array of labor market information from unemployment rates to wages and the work week and classifies the data by age, race gender and other parameters.

The final difference is that ADP is factual. It only counts actual new hires whose paychecks are processed by the company.

The NFP figures from the BLS include a monthly estimate for the number of jobs created by startup firms that have not yet been listed with the government. This number is estimated by the so-called birth-death model and is revised after comparison the tax rolls. The NFP job figures are adjusted each year to correct for the variation which has in the past been 500,000 or more.

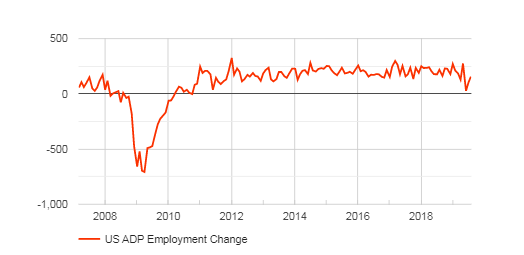

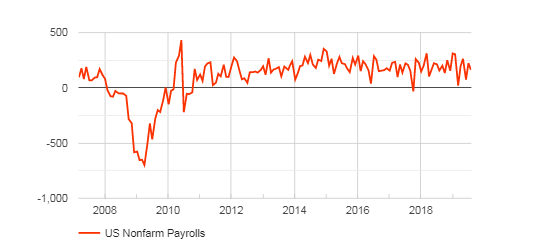

NFP and ADP Trends

Last year’s expansive pace of job creation has moderated with both reports showing a substantial decline.

The 3-months moving average for ADP payrolls has fallen from 244,000 in February to 135,000 in June and 95,000 in July. The July plunge was due to May’s anomalous 27,000 and June’s weak recovery to 102,000. If the return to trend at 156,000 in July is seconded by August’s projected 148,000 it would leave the average at the June level of 135,000.

The NFP averages have moved in similar fashion. The 3-months has decreased from 257,000 in January to 187,000 in June and 154,000 in July. Again one month, May at 75,000 drew the average south. If the 158,000 forecast for August is accurate the average will rise to trend at 182,000.

FXStreet

Both payrolls have exhibited considerable volatility this year. The ADP numbers dipped below trend in May and June, 27,000 and 102,000 and the NFP figures in February and May, 20,000 and 75,000. Such variation is common in both sets though the occurrence of two non-trend numbers in such a short space of time is a bit unusual. The weak results excited a good deal of speculation that the slowdown in job creation was becoming serious but the more recent data has put that concern at least temporarily to rest.

The Labor Market and the US Economy

American economic growth has been slowing since the first quarter’s 3.1% annualized expansion dropping to 2.0% in the second and an estimated 1.5% in the third in the Atlanta Fed’s latest (September 4th) forecast. The trade dispute with China has taken a heavy toll on the optimism and overseas business of many large US corporations with the ISM exports orders index in contraction in August.

While retail sales have remained relatively strong averaging a 0.74% monthly increase from March to July with the control group contribution to GDP at 0.88% in the same period, business spending has been lackluster.

The current growth rate of the 70% or so of the US economy that is fueled by consumption is sufficient to propel overall GDP to between 2.0% and 2.5%, but without the contribution of business investment prospects are capped.

The decline in GDP has affected the labor market. The NFP and ADP averages have retreated more than 100,000 as noted above. But even with the decrease in the NFP 3-month moving average to 154,000 in July--possibly 182,000 in August—more than enough jobs are being created to provide new entrants with positions and maintain the 3.7% unemployment rate and upward pressure on wages.

Manufacturing employment has also seen a recovery in June and July averaging 14,000 for those months after falling sharply for the first half of the year.

Conclusion

The almost two year old trade war with China is beginning to encroach on the labor market. While hiring has remained firm its decline from last year is notable. Though initial jobless claims do not give any sign that employers are releasing workers, they remains near five decade lows, such terminations would come for most firms only after hiring ceased. The backlog of unfilled positions that has built up over the past few years and the still abundant job creation have kept the economic impact of the decrease in new work marginal. That is not a situation that will endure forever.

The US job machine is under increasing threat from the US China trade war and its ramifying global economic costs.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.