UK hiring demand falls as long-term sickness rates rise further

Hiring appetite is undoubtedly past its peak, but there isn't much sign that the acute labour shortages are easing. We expect the Bank of England to pivot back to 50bp rate hikes from December, though if we’re looking for signs that the Bank is about to halt its tightening cycle, the jobs data probably isn’t the place to look.

UK hiring demand is clearly slowing

The UK jobs market is clearly past its peak. The question is whether we will see a significant deterioration as the economy slips into recession over the winter – and so far the signs are mixed.

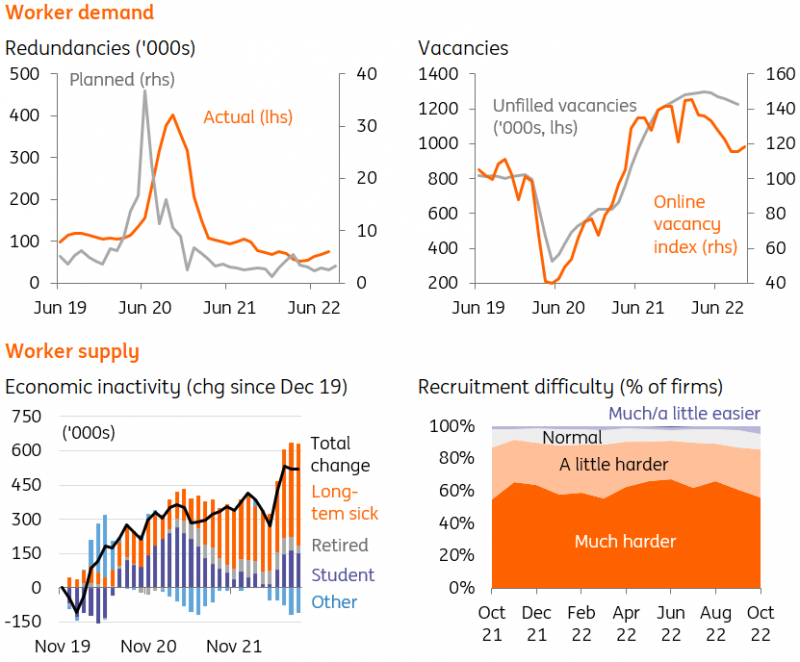

Hiring demand is undoubtedly falling back now, and we can see that most clearly in a downtrend in unfilled vacancy numbers. But so far this is manifesting itself more as a hiring freeze rather than via layoffs. Redundancy numbers, be they planned or actual, are showing little-to-no sign of increasing from their lows – albeit we’d expect that to start to change fairly soon.

UK labour market dashboard

Source: Macrobond, ING, Bank of England

Worker shortage data is based on a question in the Bank of England's Decision Maker Panel survey

The unemployment rate edged higher too – from 3.5% to 3.6% – though given the sharp rise in inactivity numbers through the pandemic, this perhaps isn’t the best gauge of hiring demand right now. This rise in inactivity – ie those neither employed nor actively seeking a job – is increasingly linked to long-term sickness numbers, which rose yet again in the latest data.

There are now almost half a million additional people registered as out of the workforce due to long-term illness than before the pandemic began. Unnervingly, this seems to be a fairly UK-specific issue, and most countries have seen inactivity rates resume a long-term downtrend as the Covid shock has faded.

Recent ONS analysis confirmed that there’s no single condition that's causing all this, though it’s hard to escape the conclusion that ballooning NHS waiting lists are a contributing factor. Those workers that have left a job due to illness are predominantly in lower-paid sectors and roles, most noticeably in consumer services. That suggests it may well be a contributing factor to the worker shortages we’re seeing in hospitality. But generally those sectors with the highest ratio of vacancies to existing employee numbers – the likes of IT and professional/scientific/technical roles – are the ones less affected by the loss of workers to long-term sickness.

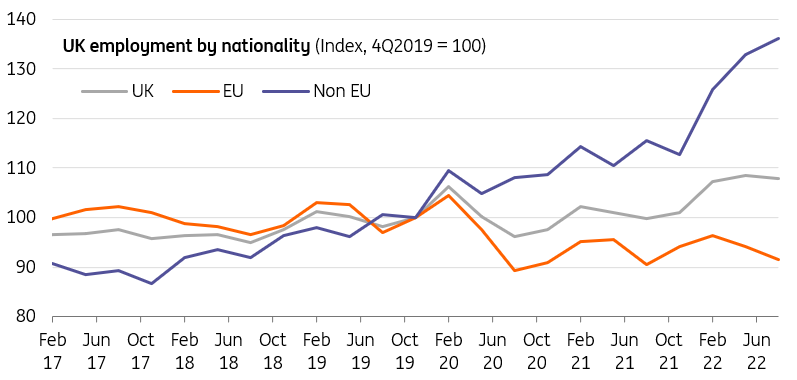

In other words, sickness isn’t the only factor driving labour shortages right now. Immigration is also playing a role, and the latest quarterly data showed that the number of EU nationals working in the UK fell again in the third quarter. These numbers are down by roughly 9% since late 2019, though interestingly, the number of non-EU (and non-UK) nationals employed in Britain is up by a third over the same period.

The number of EU nationals working in the UK has fallen through the pandemic

Source: ONS

The bottom line for the Bank of England is that skill shortages are unlikely to be resolved quickly. Its own surveys have shown that the percentage of firms reporting difficult hiring conditions has stayed resolutely high, and wage growth expectations have climbed to almost 6%. If we’re looking for signs that the Bank is about to halt its tightening cycle, the jobs data probably isn’t the place to look.

Nevertheless, with inflation close to a peak and the economy headed for recession, we still think investors are overestimating the scope for further rate rises – albeit less so than a few weeks ago. We expect a 50bp hike in December and the Bank rate to peak around 4% early next year.

Read the original analysis: UK hiring demand falls as long-term sickness rates rise further

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.