Trump's first 100 days: the honeymoon period is over

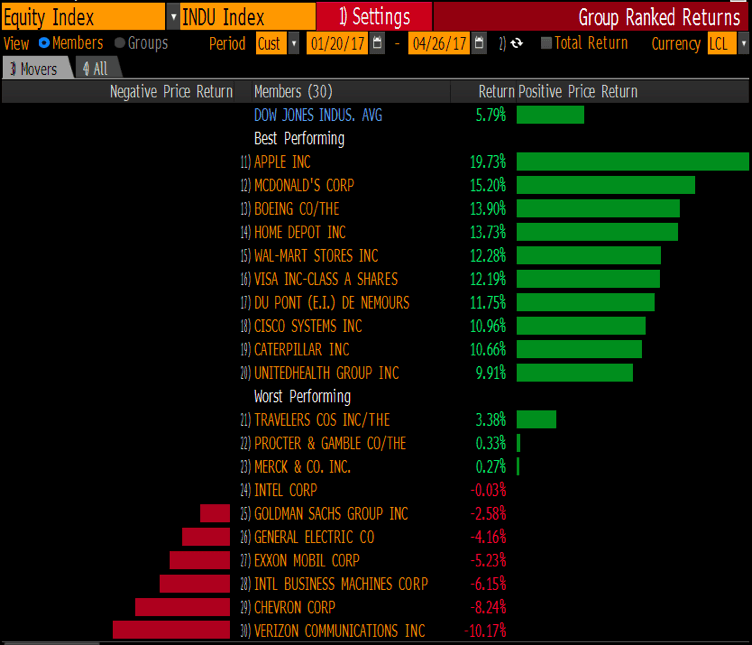

Stock market performance in the first 100 days of Trump: the honeymoon period is over On Saturday 29th April Donald Trump will mark his first 100 days in office. Rather than rehash his political successes and failures, we have decided to let stock market performance do the talking. We have looked at the best and worst performers in the Dow Jones Industrial Average since Trump’s inauguration on 20th January, as you can see in figure 1.

Below we analyse the results and attempt to explain the key drivers of their performance. We will also look at what they tell us about President Trump’s impact on US equity markets, and how the Trump administration could impact asset prices going forward.

Apple boosted by Trump tax plan and defensive status: The tech giant may have gained on the back of Trump’s proposed plan to slash corporation tax and allow companies like Apple to pay a charge to bring back overseas earnings without being subject to punitive tax rates. However, we have also noticed that Apple has developed some defensive characteristics in recent quarters, as its healthy cash position and relatively low P/E ratio compared to the overall market make Apple a safe harbour in the storm. Due to this, if we see Trump policy implementation risk start to erode market sentiment, Apple may continue to outperform due to its defensive characteristics.

Goldman suffers Trump hangover: One of the worst performers was Investment Bank Goldman Sachs, whose share price fell 2.5% during Trump’s first 100 days. Most of this loss was actually down to the bank’s Q1 results, which disappointed expectations and were the weakest compared to its peers. We think that Goldman could still be vulnerable to Trump, especially if the President doesn’t deliver his promised overhaul of financial market regulation. Thus, Goldman along with other financial stocks, could be at risk from policy implementation disappointments from the Trump administration, and the US financial sector may be an underperformer in the coming months.

Boeing brushes off Trump’s Twitter rant: Boeing was lambasted by then President Elect Trump back in December for the spiralling costs of the new Air Force One contract. This caused a sharp drop in Boeing’s share price at the time and it fell 5%, however after two days of losses the stock bounced back and is now one of the best performers in the Dow. This suggests that Trump’s power to move markets with his Twitter rants has diminished, and future targets of his ire may not experience a stock market backlash.

Caterpillar: The heavy machinery company rallied strongly in the first quarter, even though Trump’s infrastructure plan has essentially been put to bed and Caterpillar was expected to be a big beneficiary from an upswing in larger fiscal spending. The boost to its share price was largely due to its stronger than expected Q1 results. Caterpillar’s share price has risen more than 30% since Trump was elected last November. It is worth watching how Caterpillar performs in the coming months, and it could tell us a lot about the future of the Trump trade. If Caterpillar can still rally even though Trump has yet to deliver on his fiscal spending promises then we can reasonably assume that Trump’s impact on the markets could be fading, and other drivers will be key for stock market performance in the coming months. However, Caterpillar could also be vulnerable to a growing fear of policy implementation risk. If Trump’s economic impact is considered a disappointment, then stocks like Caterpillar that have been major beneficiaries of the Trump trade, could see their share prices stall.

Wal-Mart and McDonalds: The outperformance of these two stocks during Trump’s first 100 days is interesting because they both have defensive qualities. This suggests that some capital is moving to the defensive sector of the US stock market due to fears about the end of the Trump trade and a market sell-off. Thus, these stocks are acting like the anti-Trump trade, and momentum in their share prices may be maintained if Trump scepticism starts to infect the market sentiment.

Overall, the US stock market performance in the first 100 days of Trump’s Presidency could be considered a damning verdict on his initial economic policy. It also suggests that the shambolic elements of the President’s first few months on office have reduced the President’s impact on asset prices.

The key conclusions that we can draw from the US stock market performance since January 20th include:

* His Twitter rants at specific companies don’t have a long-term impact on share prices.

* Financial companies are no longer benefitting from the Trump trade, as Goldman Sach’s underperformance shows.

* If Trump can get his ambitious tax plan through Congress in the coming months then this could benefit companies such as Apple and the other tech giants, and we could see the continued outperformance of the “Fangs” (Facebook, Amazon, Netflix and Google), in the coming months.

* Defensive stocks have been top performers in Trump’s first 100 days in Washington, suggesting that there are fears about Trump’s economic policies leading to a market sell off.

* Trump’s fiscal spending programme is conspicuous by its absence, however; so far this is not driving materials and industrial stocks lower.

* Policy implementation risk could be a major theme for stock investors as we move into Trump’s second 100 days’ in office.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.