Traders mostly still believe in TACO

Outlook

Today we get US retail sales. Feb delivered 0.6% m/m, with March expected at a hefty 1.4%, although Trading Economics lowers it to 1.1%. We say the first month of the war was probably not scary enough to put off the endlessly materialistic American consumer.

Attention will be focused on the Warsh hearings and what he says about reforming the Fed. This seems to consist chiefly of objecting to the Fed stretching out into fiscal and social issues (like equality and diversity) which he says is beyond its mandate. He supports Fed independence from political interference, period. The top issue (for economists, anyway) is the too-big Fed balance sheet, which got swollen with semi-social spending, bailing out banks, and some other causes. See the Bloomberg chart. He wants to shrink it, implying lower liquidity availability and probably higher yields.

The Senate committee members are supposed to be the smart and capable ones in Congress, but they are expected to zero in on Warsh’s personal financial disclosures instead of Fed reform. Apparently, the disclosures do not qualify.

Then there is the ever-louder drumbeat of the global catastrophe driven by the closing of the Strait. Yesterday Kuwait declared a further force majeure on shipments of crude oil and refined products, meaning it cannot meet contract obligation even after the Strait re-opens. The fallout is being seen all over the world. Mr. Carney was right that the old global order is finished, and he said that before this war.

Forecast

So far today, traders mostly still believe in TACO and are more sanguine about the war than any cold, hard facts can support. In FX, the pullback didn’t happen to any measurable extent, as the outlook for another Islamabad meeting drifted around all day and all night. Traders believe in TACO but they also believe Iran will show up in Islamabad, giving Trump an excuse to extend the ceasefire deadline.

Extending the deadline is the best we can expect from talks, assuming they happen at all. As all the military and diplomatic experts say on TV, there is no way a true deal can get made in under a day in Islamabad talks. The Obama deal took 18 months. The nuclear part alone would need scientific experts, none of whom are thought to be present on either team.

We still say more things can go wrong than can go right under present circumstances. Risk-off “should” rise and take the dollar with it, despite the irony of the US being the source of the risk.

A great deal of the risk is comprised of the Trump gang gaslighting the public. They lie, they exaggerate, they swagger and strut, they mislead. It’s misinformation and not a little disinformation. The voting public is already getting ticked off, as the cute AI Iranian cartoons so cleverly detect. Trump seems to accept he will lose the midterm elections unless he can steal it, and those efforts are substantial and on-going.

Yesterday we warned against relief rallies, the preferred sentiment in equities and in FX, too. We may well get one today and tomorrow, too. But it won’t be based on anything firmer than cotton candy. All the same, this is not a recommendation to buy the dollar—not yet. We need developments and the charts to confirm, not just an indicator or two. Besides, logic does not, alas, rule.

Tidbit: The Trump government is starting to make the tariff refunds--$166 billion. It took two months after the Supreme Court decision. It “should” have taken two days.

Tidbit: A splendid FT headline in “opinions”: “The European right is pivoting away from America. Electoral logic is driving a shift as polls lay bare European disgust at the US administration.” When did we ever see the word “disgust” in an FT headline?

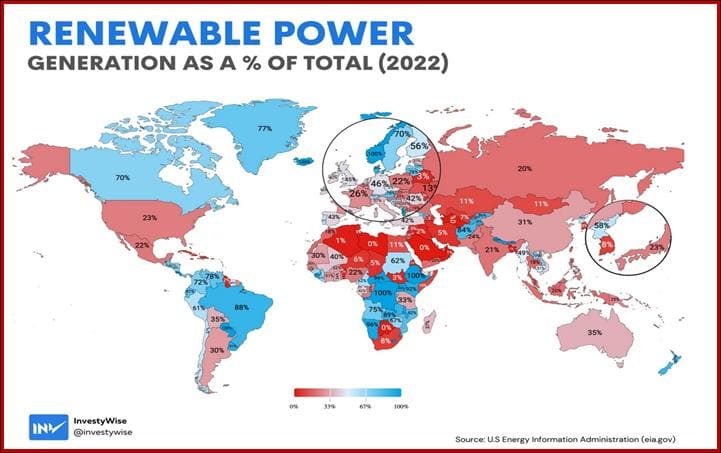

Tidbit: There is only one party benefiting from the Iran war—China. It can tolerate the oil shortages because it has nearly a year of stockpiles, plus it has coal and renewables. The US is circling the drain in terms of global respect, soft influence-- and embrace of renewables. It’s no surprise that China is the leader in renewable energy, too. This is going to be a Big Deal in the history books—after the US ruled new inventions/technology for over 200 years, devised at home or purloined.*

Here’s the Google AI on renewables: “Renewables provide roughly 13–15% of total primary energy globally and about 9% of total U.S. energy consumption. While the total energy share is lower, renewables now generate over 30% of global electricity and over 20% of all U.S. electricity, largely driven by rapid growth in solar and wind power.”

See the map and note that it’s from 2022, so likely bigger numbers today. Some notables: Brazil has 88% of power from renewables. Canada, 70%. Norway, 100%! All oil producers. Even Sweden has 70%. (Sudan is shown with 62%, and Congo and Ethiopia with 100%, but that’s not believable.)

We celebrate American ingenuity and inventiveness but we stole a lot, too. That includes the spinning wheel and looms, the steam engine and thus railroads (from the UK), and a bunch of German inventions after WW II, including von Braun’s rocket. Marconi (Italy) invented the radio, or maybe it was Tesla. The US invented the transistor and the cell phone but it was Japan and Finland that developed them into workablility… before Steve Jobs came along.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat