Traders brushing aside US political risk as sentiment remains positive [Video]

![Traders brushing aside US political risk as sentiment remains positive [Video]](https://editorial.fxstreet.com/images/TechnicalAnalysis/Sentiment/business-people-40397018_XtraLarge.jpg)

Market Overview

President Trump has been impeached. However, markets are paying very little attention. US politics has become hugely partisan during the time of an incredibly divisive President. The Democrat-controlled House has been perusing this impeachment process, but it is little more than political theatre. A simple majority in the House of Representatives was needed to “impeach” President Trump. However, the process needs to be “convicted” in the Senate by two thirds majority. The Republicans enjoy a 53-47 majority and thus means a highly unlikely 19 Republicans would need to vote against their President to convict the impeachment. The chances are extremely slim. So the political risk is being all but brushed off (although this could impact on Trump’s electoral chances of a second term). Risk appetite remains relatively high and this is reflected in the underperformance of safe havens. VIX Volatility remains around multi-month lows, whilst Treasury yields moved higher (with a yield curve steepener). Equities and forex majors have become are a little cautious, but, this is more a function of a lack of conviction surrounding the true implications and components of the “phase one” US/China trade agreement. The Dollar/Yuan rate hovering almost bang on 7.00 in recent days reflects this. The Bank of Japan did very little to change the narrative in its latest monetary policy decision.

Wall Street closed a very subdued session around the flat line yesterday, with the S&P 500 -1 tick at 3191. With US futures again all but flat today, Asian markets have struggled for direction (Nikkei -0.3% and Shanghai Composite flat). European markets continue this theme with FTSE futures and DAX futures all but flat. In forex, there is a slight improvement in risk which has allowed EUR and perhaps more interestingly, GBP to find support. The big mover of the early part of the session is outperformance from AUD which is higher on better than expected employment data. In commodities, we see the continued consolidation on gold whilst oil is also consolidating its recent run higher.

There is a UK focus on the economic calendar early today. At 0930GMT UK Retail Sales (ex-fuel) are expected to grow by +0.3% for the month of November (after falling by -0.3% in October) which would mean that the year on year growth drops back to +1.9% (from +2.7% in October). The Bank of England monetary policy is at 1200GMT with the MPC not expected to move the interest rate at +0.75%, but of more interest will be on how many members vote for a cut. In November there were 7 votes to hold and 2 votes to cut. This is expected to be the same again in December. On to the US data, US Current Account is at 1330GMT and is expected to see the deficit improve slightly to -$122.1bn in Q3 (from $-128.2bn in Q2). Weekly Jobless Claims are at 1330GMT and are expected to moderate slightly to 225,000 (from the spike to 252,000 last week). The Philly Fed Business index at 1330GMT is expected to slip slightly to +8.0 (from +10.4 in November). Existing Home Sales at 1500GMT are expected to drop by -0.2% to 5.44m in November (from 5.46m in October).

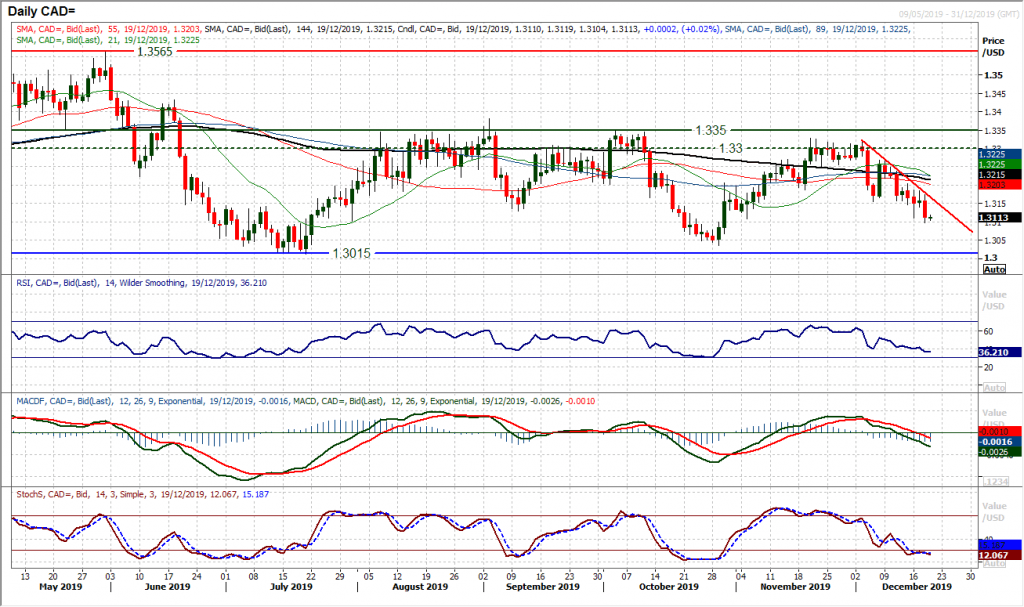

Chart of the Day – USD/CAD

The Canadian dollar has consistently repelled US dollar strength throughout 2019 and once more is finding positive traction towards the end of the year. For the past six months, the price has traded in a broad range between 1.3015/1.3350. Resistance around 1.3300/1.3350 once more found Canadian dollar buyers willing to come back in to pull USD/CAD lower. This move is now trending decisively and eyeing a test of the range lows again between 1.3015/1.3035. A two week downtrend of lower highs breached support at 1.3150 this week and with continued deterioration in the momentum indicators, there is downside potential in this latest bear run. The RSI confirms the recent breach of support and is negatively configured below 40, whilst the MACD lines are now falling below neutral and Stochastics are bearishly configured. Into today’s session, the mini downtrend is resistance at 1.3165 with the old support around 1.3150 now resistance and we look to sell into near term rallies. The near term resistance at 1.3185/1.3205 is key to the continued correction lower. A move below support at 1.3105 opens 1.3015/1.3035.

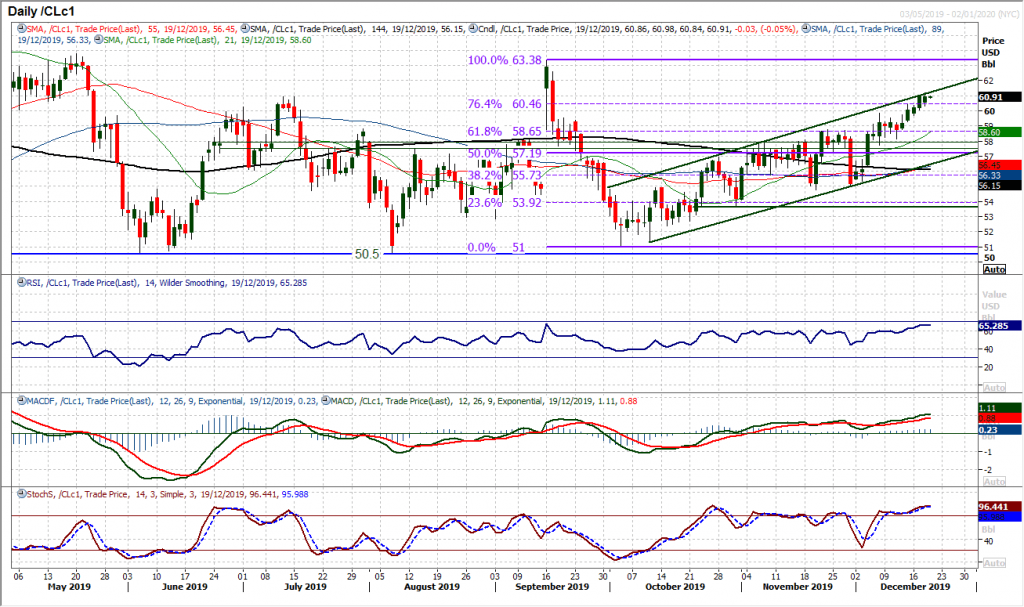

WTI Oil

The market has consistently looked to buy into intraday weakness since the OPEC meeting a couple of weeks ago. A run of positive candles have pulled the market to the top of the uptrend channel (which today comes in at $61.25). Of significance also, the move has also now started to pull higher above the 76.4% Fibonacci retracement (of $63.40/$51.00) at $60.45. Closing decisively clear above would open a full retracement back to the high again at $63.40. The move in the past week has also looked to strengthen the importance of the breakout support band $57.85/$58.65. For now, we see strengthening momentum with the RSI into the mid-60s and MACD lines at seven month highs. Ultimately we are still mindful that retracements of bull breakouts are frequent within the trend channel and therefore weakness would be a chance to buy.

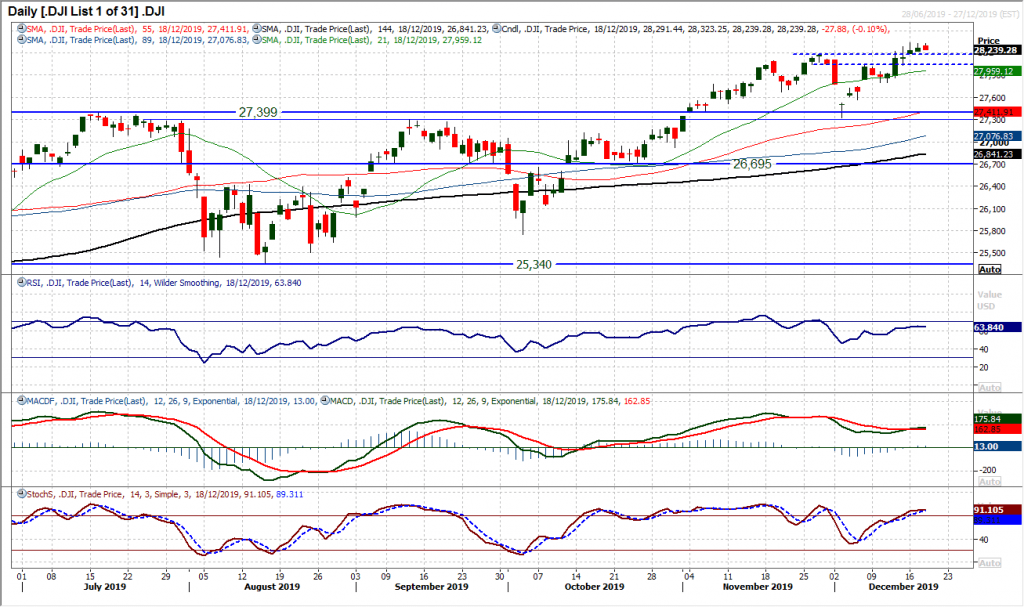

Dow Jones Industrial Average

Equity markets have been somewhat tentative in recent sessions. Since the turn of the week and a questioning of the phase one agreement between the US and China, the Dow has been slightly edgy in its breakout to new highs. Small candlestick bodies and three daily ranges well shy of the Average True Range of 219 ticks. The momentum indicators are positively configured but in the wake of yesterday’s marginal close lower (also at the low off the day) there is a tempering of the impetus. However, RSI remains above 60 and Stochastics above 80. We could continue to see near term corrections as a chance to buy (US futures are all but flat this morning). There is a band of initial breakout support at 28,035/28,175 and the bulls would be in control whilst the support at 27,800 remains intact. The Dow would turn corrective on a move below the December low at 27,325.

Author

Richard Perry

Independent Analyst