Trade in a COVID-19 world, Unemployment support, bank stress tests

In a number of areas, the pandemic is accelerating trends that were already in place. Online purchases, virtual meetings and live event streaming are all gaining momentum as the world adjusts to life in the time of COVID-19. Family lawyers are reporting an increase in separations as couples working from home struggle with too much togetherness.

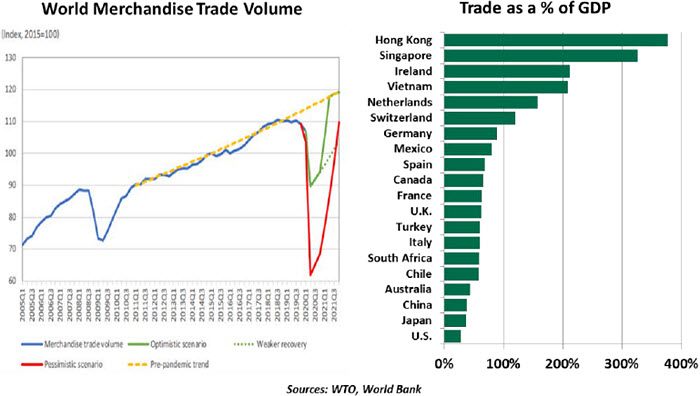

On a broader scale, the pandemic has also accelerated the trend of countries separating themselves from one another. International travel has been severely curtailed, and international commerce may follow. The economic consequences of these developments will be significant and lasting.

Trade has been a four letter word in some quarters for more than a decade now. Imports and exports grew rapidly for a generation, with most countries better off for their participation in the global marketplace. Studies suggest that freer trade has increased incomes, reduced poverty, created jobs and generated substantial amounts of wealth. But studies also suggest that the benefits of globalization have been uneven, with some nations and some communities left behind.

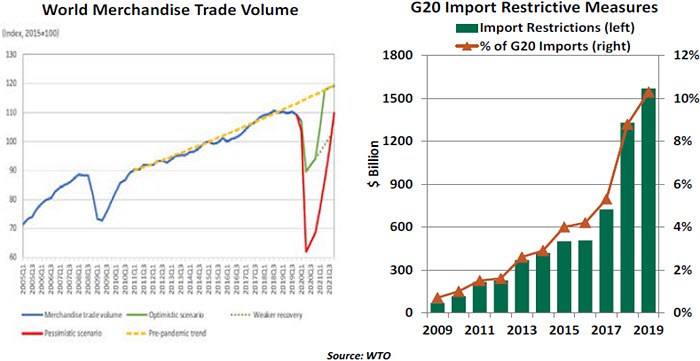

Countries began looking inward in the wake of the 2008 financial crisis. The desire to support local firms and populations led to rising protectionism; measures of trade openness peaked in 2009 and have been declining ever since. The number of import restrictions tracked by the World Trade Organization (WTO) has risen for ten straight years.

The watershed elections of 2016 in the U.K. and the U.S. added impetus to the reevaluation of trade. The outcomes were a surprise, but the groundswell of public disaffection with globalism had been building for some time. In the years since, tariffs and non-tariff barriers have proliferated. China and the United States have come to view each other with increasing mistrust, and have pressured third parties to take a side in the rivalry.

In sum, trade was very much on the back foot when the pandemic began. COVID-19 has made regaining balance even more difficult.

When the outbreak arose in China, it prompted broad-based business closures. The interruption of supply from Chinese factories was a stark reminder of how dependent the rest of the world had become on China’s supplies. As we \discussed recently, modern supply chains are built to be efficient, but we are learning that they aren’t very resilient.

“Global supply interruptions raise issues of economic security.”

The case of personal protective equipment (PPE) is telling. China accounts for about 60% of the global production of surgical gowns and masks. When the virus struck, China kept a greater share of that output at home, leaving others short-handed. China has also been accused of not being fully honest about when exports might return to normal, hampering the development of alternative capacity elsewhere.

This situation raises an issue of economic security. Countries are reluctant to outsource certain products too extensively; if supply chains are interrupted or economic relations sour, domestic alternatives must be in a position to step forward. Food is the foremost example; every country shelters its agricultural sector to one degree or another.

The pandemic has illustrated vulnerabilities in other sectors, like PPE, that governments are anxious to patch. So far this year, 90 governments have temporarily blocked the export of medical goods. A desire for increased self-sufficiency will require favoring domestic producers, even if they are more expensive.

That desire intersects with another byproduct of the pandemic. National governments have been forced to step up and support significant domestic companies or industries to keep them from collapsing. In calmer times, trade policy discourages this kind of practice so that international competition is conducted on a level playing field. But the times we live in are anything but calm. Countries that do not have the means to protect their national champions will fall behind.

If the trend towards “re-shoring” gathers steam, China and several of its near neighbors stand to lose the most. Last month, we noted that China was hindered by the pandemic first, and recovered first. But while its factories aspire to restore full output, international markets for some Chinese products may be narrowing. This will make it harder for China to sustain growth, provide employment, care for its aging population and address its substantial indebtedness.

“China could be the biggest loser as re-shoring gains steam.”

Some analysts have suggested that China’s increasingly belligerent posture toward a range of other countries is a reaction to acute economic pressure. Beijing’s aggression has prompted concern in a number of world capitals about accepting Chinese investment or cooperating with China technologically. While this might make sense strategically, raising barriers to capital and collaboration will have an economic cost.

Reshoring will not be easy, or rapid. New facilities may need to be constructed, and regional alliances (like the United States-Mexico-Canada Agreement) may need to accommodate potential geographic shifts. While some countries may hope to regain employment in the process, producers will undoubtedly stress automation and efficiency to preserve some of the cost advantages of global chains.

A little over 100 years ago, the last true pandemic finally began to die down. By that point, the Spanish Flu had infected a third of the world’s population and claimed an estimated 50 million lives. That event combined with the aftermath of World War I to arrest globalization. By some measures, it took a half-century for international trade to recover.

At least for now, neither COVID-19 nor the current set of international frictions is nearly that severe. But the consequences of both for public and economic health are growing.

Unfinished Business

“The hardest work in the world is being out of work,” said civil rights activist Whitney Young. Millions of Americans are facing the demoralizing challenge of unemployment. Recognizing the upheaval to come in the labor market, the CARES Act included provisions to get workers through a dry spell. Despite a job market that is still dislocated, those measures will soon expire.

The CARES Act helped consumers through two channels. One-time payments worth $1,200 per person and $500 per child were made to all taxpayers. Most payments were disbursed in April, and even diligent savers will consume them if their incomes remain impaired.

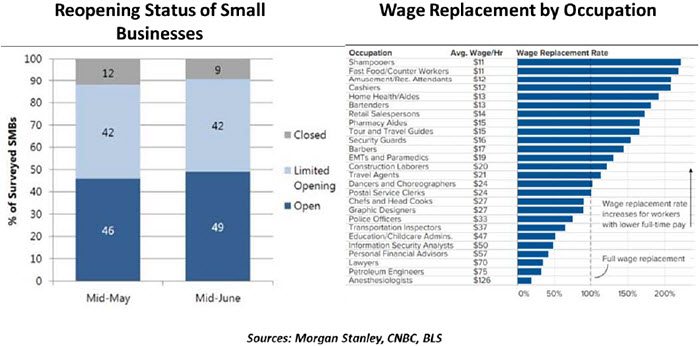

Congress broke new ground by adding a supplement to unemployment insurance (UI) payments. UI is a program managed by each state that provides small amounts of money to help keep workers fed and sheltered. Payouts vary by state and prior income, but are on the order of $333 per week. The CARES Act funded a federal supplement of $600 per week. Most workers were made whole by this addition, minimizing the economic disruption.

The government launched the program quickly to help workers in need as much as possible. But a wrinkle emerged: The supplement meant up to two-thirds of UI recipients received a higher income collecting UI than they did while working. The lowest-paid workers had the most to gain.

Detractors of the supplement say this wage arbitrage is stopping rational workers from returning to their jobs. But this is an oversimplification. Workers who are called back to a job and decline it will lose their eligibility for UI. The problem runs much deeper: There are not enough jobs to return to. Though unemployment is improving, total employment remains more than 14 million jobs below its pre-crisis level. The return to work is not coming as quickly as the decline did.

Consumers have already buckled down in preparation for a prolonged recession. The savings rate spiked as consumers received government payments but had less willingness and fewer options to spend it. Personal income grew due to fast-acting government programs. But in a worrying sign of the pandemic’s ongoing fiscal toll, over 100 million consumer credit accounts are reported as being deferred due to economic circumstances.

The CARES Act’s UI supplement will expire at the end of July. If allowed to lapse, the shock will be sizeable. Over 19 million UI recipients would see a $600 per week reduction in their incomes. That is a shock that can lead to lasting damage: a crisis of confidence, repossessed vehicles, evictions, foreclosures and even social unrest. But it need not be so severe.

Some proposals would realign incentives by paying workers a one-time bonus upon their return to work, giving a greater value to working than collecting UI. But this assumes workers are staying home voluntarily. Many are sidelined due to a slow economic recovery or lack of childcare, and no payment can recreate jobs or reopen schools.

“Cutting insurance benefits amid record unemployment would be an unforced error.”

Proposals are emerging to make a more gradual transition from $600 to $0. One replacement system would calculate individual supplements as 40% of a worker’s pre-crisis income, capped at $400 per week. Combined with state benefits, workers could receive up to 80-90% of their past income. Supplements would be phased out as local employment improves; once a state is below a 7% unemployment rate, the support ends.

The next round of stimulus is under debate in Congress, and talks are stuck on UI support. Thus far, the federal expansion of UI has kept households afloat during unprecedented uncertainty. The UI expansion and direct payments together cost $561 billion, about one-quarter of the total cost of the CARES Act. The hope for a quick recovery by July was misplaced, but this remedy was appropriate and helpful. Negotiations may be hard work, but surviving unemployment is harder.

Gearing Up

We on the economics team had expected a summer reprieve. Starting in 2020, the U.S. Federal Reserve no longer requires mid-year stress tests, which meant we no longer have to create stress test scenarios. We planned to use the free time for holidays and other projects. But the reprieve has been revoked.

Last week, the Fed released results from its annual stress test. While the banking industry fared well under the severe scenario that was composed earlier in the year, that scenario was mild compared to the real circumstances of 2020. As a result, the Fed has asked banks to submit new capital plans later this year. Banks will need to demonstrate their performance during the current uncertainty from the pandemic, an economic shock far worse than any other in the post-war era.

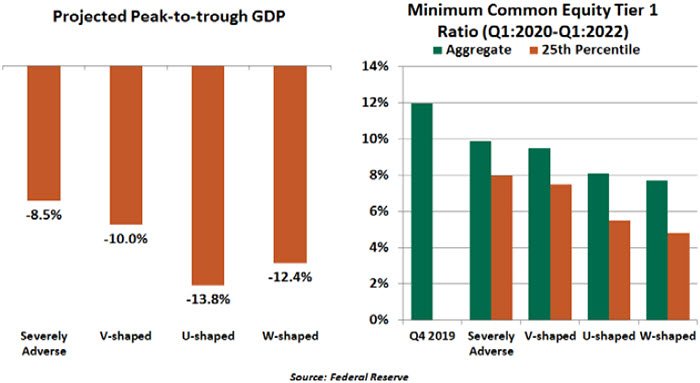

It wasn’t a surprise to see that most firms under the “normal” stress scenario would remain well capitalized. The regulatory requirements for higher capital levels imposed after the 2008 financial crisis have bolstered the banking system’s resiliency. But the Fed went further, performing additional tests under hypothetical downside scenarios, characterized by recovery paths in the shapes of the letters V, U and W.

In such tough operating environments, large banks show some vulnerability. Under the “W”orst case scenario (reflecting a second wave of infection and second downturn), aggregate loan losses for the 33 banks tested were projected to climb to $700 billion, with a handful of firms expected to see their capital ratios fall close to regulatory minimum of 4.5%.

“Under a W-shaped recovery, several banks will likely see substantial capital depletion.”

As a precautionary step, the Fed told banks to suspend share repurchases during the third quarter and capped dividend payouts at second-quarter levels. This should help the weakest banks to improve resiliency.

The resubmission will help provide better evidence of the resiliency of the banking system amid an unprecedented economic crisis. The exercise will also give firms and the Fed a better window into what might lie ahead. While we’re none too happy about having a busier summer, we think the effort will be worth it.

Author

Northern Trust Economic Research Department

Northern Trust