Tomorrow it’s going to be a different kettle of fish – It’s back to worries about inflation

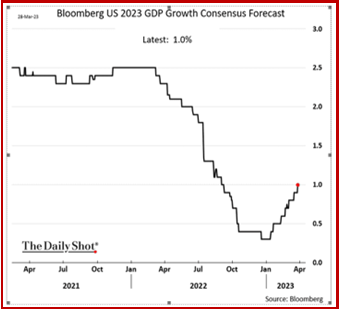

Outlook: Today we get the usual Thursday jobless claims and then the final quarter/quarter GDP for Q4 in the US, previously reported at 3.2% but expected to dip to 2.7%. The Bloomberg chart of forecasts–not actuals, forecasts–bottomed in January before hitting zero and has been climbing ever since. (Funny, this runs counter to the expectation of recession, two quarters of negatives, from the inverted yield curve.)

We tend not to care too much about weekly jobless claims, but Bloomberg is trying to make hay out of straw by warning we could be just beginning to see the labor market crack. See the chart. This is, of course, what the Fed wants. Bloomberg reports its chief economist for financial products “has been tracking the labor talk on S&P 500 earnings calls, and noted recently that there are now more mentions of job cuts than labor shortage on a three-month rolling basis.” Tiny bubbles.

Having said that, the NY Fed just released a paper on the participation rate gap. “The U.S. labor force participation rate currently stands at 62.5 percent, 0.8 percentage point below its February 2020 level. This ‘participation gap’ translates into 2.1 million workers out of the labor force. This post evaluates three potential drivers of the gap: baby boomers reaching retirement age, putting downward pressure on participation; the rise in the share of retirement age individuals who have retired since the onset of the pandemic; and long COVID and disability, which may induce more people to leave the labor force.”'

Bottom line–the labor shortage issue is not fixed, but rising and wider-spread layoffs may halt the wage increase movement dead in its tracks.

We also get German inflation later this morning with plenty of uproar already from the Spanish number–3%!!–if due almost entirely to energy costs plunging. Spanish core remains sticky at 7.5%. Whatever Germany and the eurozone report for headline, that sticky aspect for core is going to remain and prevent traders from imagining rate cuts.

This has been an uneventful week so far, with all eyes on the banking sector but nothing to see. In fact, markets are happy to have unraveled the issues behind the failure of two US banks and having found a hero for UBS/Credit Suisse. Regulators are speaking loudly and in the US, the FDIC has already announced the price it will charge the banks for the bailouts. One and two weeks ago, stories about botched supervision and incompetent management ruled the day. Confidence in both banking and government was already low and falling further. Now the tension has eased almost entirely–maybe too far.

Morgan Stanley just downgraded Charles Schwab, on clients subtracting deposits at a furious pace, the stock falling, and earnings outlooks grim. This may or may not be the start of a series of single-name targeting that drags out the banking crisis. This does not, so far, affect FX. A separate issue is going to hit the banks and their earnings–the new charges the FDIC plans to impose for the cost of the bailout so far. It needs to get almost $23 billion and is proposing special assessment, to fall more heavily on the big banks like JPMorgan , Bank of America and Wells Fargo, according to Bloomberg.

Tomorrow it’s going to be a different kettle of fish. It’s back to worries about inflation. It starts with PMI in China and CPI in Japan, but moves on to eurozone's CPI and the PCE deflator in the US.

Forecast: We worry about a lack of momentum in the FX market and the eerie calm that makes a 30-50 point move interesting or suggestive (except for the dollar/yen). To speak of consolidation is to say traders are clueless and so inactive. The month and quarter are ending, and the big Easter and Passover holidays are beginning, so we need to wonder if this sideways tendency can go on for another couple of weeks. It seems improbable because a trigger almost always comes along to spark movement. We don’t know what it will be–maybe sticky inflation, although we are kind of tired of that. Beware rumors.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat