Today the data menu includes final ISM manufacturing and PMI, and JOLTS

Outlook

Today the data menu includes final ISM manufacturing and PMI, construction spending and the most important one, JOLTS. Job opening are forecast lower at 7.674 million from 7.7 million. We don’t’ see how that can be stretched to a crisis reading and Mr. Powell’s “np hurry” stance yesterday may tame the panic beast.

Aside from the question of Middle East war and after Powell tried to pour cold water on gung-ho rate cut frenzy, the most important FX development is the Bank of Japan minutes from Sept 19-20. We often get comments from BoJ and MoF officials but we can’t’ remember the last time the press took up the minutes themselves.

According to the Reuters story, caution was the tone. Even those members who want to normalize said tightening can wait while watching what happens in various markets. Besides, the sharp change in the yen that tanked the Nikkei could go on to damage sentiment, not to mention profits. As far as we can tell, the phrase “carry trade” was not named.

It's interesting that the Fed’s 50 bp rate cut the day before caused concern about the outlook for the US economy. What data were they looking at? We can recommend the Atlanta Fed. “Even a proponent of future rate increases called for patience in pulling the trigger, the summary showed, a turnaround from the previous meeting in July when many in the nine-member board voted for a rate hike to pre-empt the risk of too-high inflation.”

This is not an impressive performance. The next policy meeting is is Oct. 30-31 and will contain new quarterly growth and price forecasts. The BoJ ended zero rates in March and raised once in July. Delay in Sept suggests cold feet. We shall see if the incoming new government puts some starch in spines.

Tidbit: The longshoremen strike could subtract as much as $3.8-4.2 million per day from the US economy, according to JP Morgan. The strike is for better wages and job security. The top three ports to be affected are New York, Baltimore and Houston. The price of everything from socks to Cheerios may go up.

Forecast

Mr. Powell told the rate-cut market to chill and while it seems he had only a small effect on them, FX traders were paying attention and the dollar got some demand--enough to move the needle, at least for a while. Again, we can’t tell whether the Middle East situation is driving any serious risk aversion, not with oil prices back down (Brent at $71).

The US economy mostly delivers a rosy picture (and the worry about the labor market a sham), while the eurozone economy is struggling and about tof all into the slough of despond. Of course the dollar should not be on the for-sale list. But stranger things have happened and we hesitate to say the move yesterday is the start of a correction, let alone a reversal.

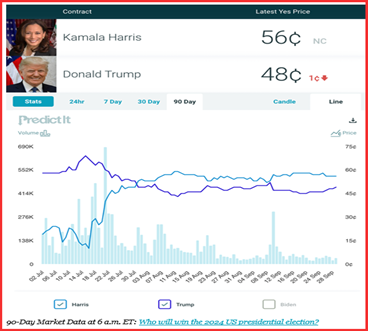

Political Tidbit: As everyone points out, the surveys are not to be trusted even as they show Harris inching ahead even in the critical swing states. The VP debate tonight is not lijely to move any needles. But yesterday PredictIt had this summary. Should we assume the bettors are pricing in the electoral college?

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat