To hike or to hold? Three scenarios for the Bank of England’s next steps

A repeat 25bp hike is largely priced for September, but markets are also factoring in an almost 20% chance that the Bank of England keeps rates on hold.

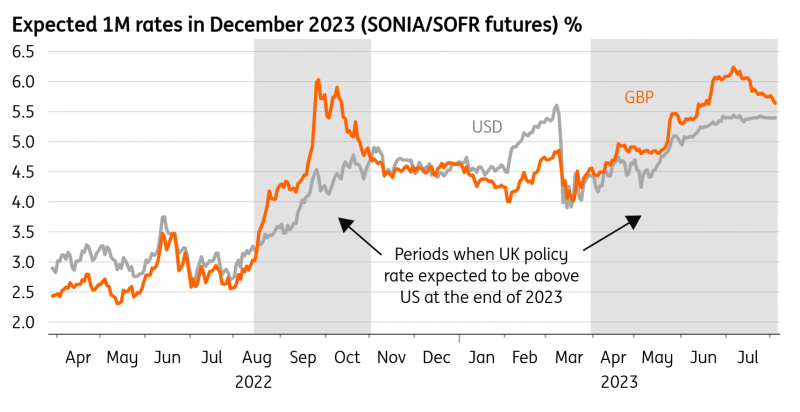

Markets have reappraised the Bank of England outlook

Could the Bank of England pause its interest rate hiking cycle in September? Just a month ago, market pricing implied that would be highly implausible. Investors were close to pricing 50 basis-point rate hikes both in August and September – and indeed expected further moves to take Bank Rate well above 6%.

We warned at the time that this seemed exaggerated, and sure enough there's been a big reappraisal of the Bank's tightening cycle over the past few weeks, culminating in the Bank delivering a more modest 25bp hike at its August meeting. A repeat move is largely priced for September, but markets are also factoring in an almost 20% chance that the Bank keeps rates on hold.

Markets have lowered expectations for UK bank rate later this year

Source: Macrobond

The bank is squarely focused on convincing markets that rate cuts are a long way off

A pause isn't our base case, but we think investors are right to be thinking about one. Central banks across the developed world are grappling with the challenge of stopping rate hikes without markets bringing forward rate cuts bets. The Federal Reserve has managed, with some success, to stem talk of rate cuts with the so-called "skip" strategy. By keeping rates on hold at one meeting (June), with a promise to resume rate hikes later on (July), the Fed has managed to draw out its rate hike cycle. The result is that the debate is still centred on "how many more hikes are we going to get?", rather than "how soon will the first rate cut come?".

The success of this strategy has not been lost on other central banks. ECB President Christine Lagarde has hinted that a pause is possible in September. We'd be surprised if the Bank of England wasn't starting to think along these lines too, and last week's meeting contained a few hints that policymakers are edging in this direction.

The Bank included a new sentence in its statement, signalling it would keep policy "sufficiently restrictive for sufficiently long". Not only does that tell us the Bank is gearing up for a battle with investors to convince them that rate cuts are a long way off, but this is also the first time the Bank has formally stated that policy is now "restrictive". That might be a statement of the obvious, but the fact officials are now publicly saying this says the Bank thinks interest rates are doing their job, and that the job is almost done.

There were similar clues in the Bank's forecasts. Now admittedly the Bank is putting much less faith in its models than usual. But even when policymakers add an "upside skew" to what these models are churning out, the so-called "mean" forecast still points to inflation back at target in two years' time. Curiously that's regardless of whether the BoE hikes rates to 6% (as markets were expecting prior to the August meeting) or keeps Bank Rate at 5.25% indefinitely.

The lesson here is that the Bank is likely to become less focused on how high rates need to go, and instead the central goal will increasingly be to keep market rates (with say two/three-year tenors) elevated long after it stops hiking. Any further rate hikes should be seen as a means to that end. And if the Fed's experience is any guide, a tactical pause in September, and a threat of a follow-up hike in November, could help that objective.

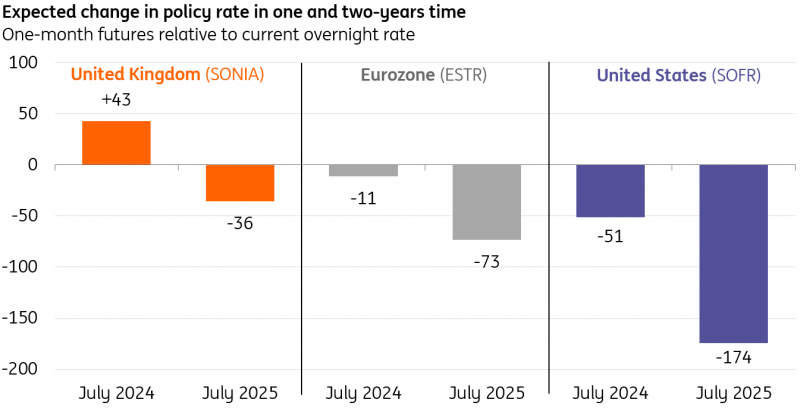

Markets are pricing fewer rate cuts in the UK relative to the Eurozone/US

Source: Macrobond, ING calculations

Data as of 7 August

September is probably too early for a pause

For now, the Bank needn't be too worried. Compared to other developed markets, investors are pricing barely anything in terms of rate cuts over the next couple of years. Investors expect Bank Rate to be just 40 basis points lower in two years' time, compared to almost 200bp at the Fed and roughly 75bp at the ECB. The flipside of course is that there's greater room for repricing as investors come to realise the UK's inflation problem maybe isn't so different to elsewhere. A comment by BoE Governor Andrew Bailey at the ECB's recent Sintra conference, where he made a point of warning markets against pricing rate cuts prematurely, shows the committee isn't being complacent.

So in practice, September is probably too early to see a pause. The BoE has been fairly transparent that further hikes hinge on wage growth, services inflation, and to a lesser extent, the vacancy-to-unemployment ratio (a gauge of slack in the jobs market). We've looked at some scenarios for these in the table below.

On the first of those indicators – wage growth – the Bank reckons it is going to come down only very slowly, and as we discussed a few weeks ago, we tend to agree. The Bank is forecasting private sector wage growth at roughly 6% by year-end from just under 8% now, which seems fair. This is likely to become a central argument for keeping rates "higher for longer".

Where there's greater scope for a positive surprise is in services inflation. The Bank thinks this will be unchanged at 7.2% in August's data (the last reading prior to September's meeting) and will fall only fractionally to 6.9% by year-end. But various surveys have suggested much of the rise in services inflation can be put down to higher gas prices last year, and the subsequent reversal will alleviate one major source of pressure on firms to raise prices. We therefore think there'll be a more noticeable fall in services inflation, although we suspect we won't have seen enough evidence of this by September.

But by November, we expect this story to be more evident, and we should have seen a further gradual improvement in worker supply. Not only that, but assuming both the Fed and ECB appear to have finished hiking by then, the Bank risks being the last hawk standing. Our base case is therefore that the Bank hikes again in September but that this marks the top of the tightening cycle.

Read the original analysis: To hike or to hold? Three scenarios for the Bank of England’s next steps

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.