Time to rethink excess savings

Summary

A defining characteristic of the current economic expansion is the uncanny staying power of the consumer. In this report we explain why we are moving away from the “excess savings” measure we previously used and why we will no longer make estimates of how long excess savings will last.

Times they are a-changin'

A year ago there was a general consensus among economists and financial markets that a recession was in the offing. Those forecasts have largely been pared, put off or canceled altogether. To some extent the rationale for these more sanguine assessments is a recognition of the uncanny staying power of the consumer. That consumer resilience, in turn, has relied upon a trio of supporting factors: The first is income, which has generally outpaced inflation over the past year or so. Access to credit is another—credit which was once both cheap and widely available but lately has been neither of those things. Last, and perhaps most unique to this cycle is excess savings. It is this final drive that we seek to better understand in this report.

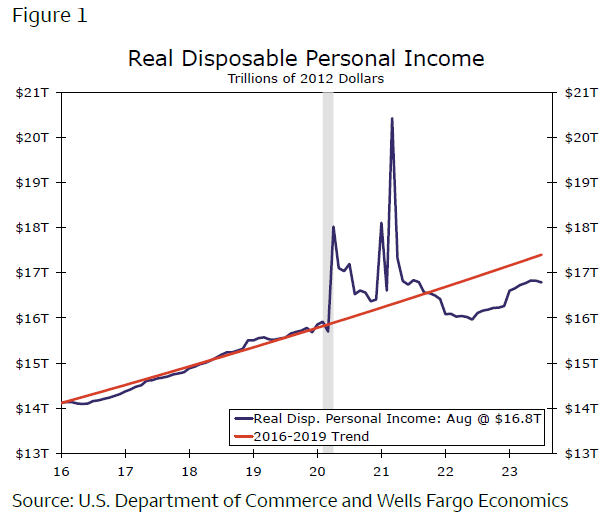

In the first 12 months that followed the pandemic, robust fiscal policy under two different presidential administrations boosted personal income in an impactful way. The three largest of these programs—the CARES Act, the December 2020 COVID-19 Relief bill and the American Rescue Plan in 2021—played the biggest role in boosting pay and are clearly visible in the data for real disposable personal income (Figure 1). There were other measures as well, from student debt relief to provisions that allowed people to stay in homes or apartments rent-free without fear of eviction also played a more marginal, but not inconsequential role in supporting the health of consumer balance sheets.

Author

Wells Fargo Research Team

Wells Fargo