TIC: Who Bought all the Treasury Securities?

About a year ago, we published a report titled "Who Will Buy All the New Treasury Securities?" In this onepage report, we provide a brief update using data from the Treasury and the Federal Reserve's Flow of Funds.

Who Bought all the Treasuries? Us.

A little over a year ago, we published a report titled "Who Will Buy All the New Treasury Securities?" which focused on demand for the looming surge in net Treasury issuance in 2018. This surge came to pass, as net Treasury issuance in 2018 will be about $1.3 trillion (counting Federal Reserve redemptions), up from just $568 billion in 2017.

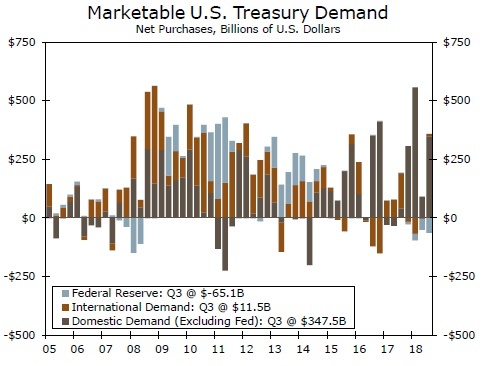

So who ended up buying all of these Treasuries? In short, it was overwhelmingly Americans. The top chart illustrates both the surge in total supply and the extent to which Americans stepped in to fill the gap. Over the past four quarters, domestic buyers (excluding the Federal Reserve) have absorbed more or less the entirety of the marginal increase in marketable Treasuries outstanding.

Who are all these domestic buyers? For a more granular look at Treasury holdings, we have to turn to data from the Financial Accounts of the United States. In last year's report, we argued that "U.S. households seem like the most obvious candidate to absorb a large chunk of the new supply." This appears to have proved correct. U.S. households are the largest domestic holder of Treasury securities (excluding the Fed) through both outright holdings and holdings through mutual funds and exchange-traded funds. Holdings of Treasuries in these two categories rose by just over $1.0 trillion over the year, accounting for nearly the entirety of the overall increase.

As we noted at the time, the household sector in the Financial Accounts is a residual that is undoubtedly capturing some non-household Treasury holders, but the trend appears clear even if the exact magnitude is not. In contrast, U.S. banks, which saw significant growth in their Treasury holdings from 2014-2017, picked up very little of the new supply. U.S. banks' holdings of Treasuries rose just $21 billion between Q3-2017 and Q3-2018.

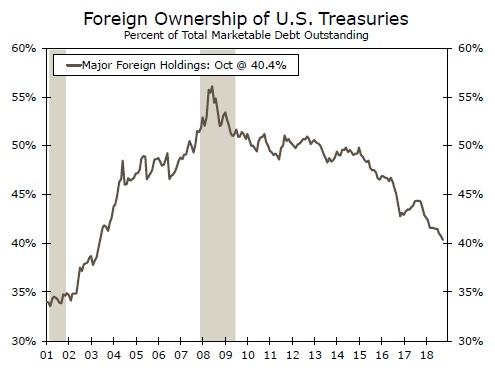

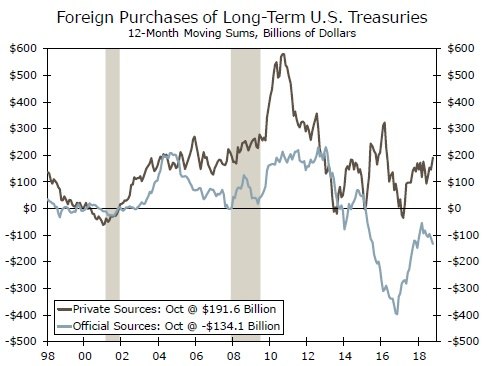

Against this backdrop, international holdings of U.S. Treasuries as a share of the total have continued to fall, reaching a 15-year low in October (middle chart). Foreign private buying has remained positive over the past 12 months, though it is well below its recent highs. Holdings by "official sources", predominantly central banks in the form of FX reserves, have been in decline for several years (bottom chart). Continued weakness in several foreign currencies has likely contributed to the extended decline in foreign official holdings, while expensive hedging costs and a steady decline in bond prices have likely limited foreign private demand for the time being.

As we look to next year, we believe the pace of growth in net Treasury issuance will slow significantly, but the overall level should be about the same as it was this year. This unusual late-cycle pattern of robust Treasury supply, coupled with continued fed funds rate hikes, underpin our forecast next year for a continued increase in Treasury yields across the entire curve.

Author

Wells Fargo Research Team

Wells Fargo