This week brings earnings reports from some critical techs, including Alphabet, Intel and Tesla

This week we get the flash PMI’s from everybody. On Thursday it’s the IFO and US durables and existing home sales. The biggie may well be US consumer sentiment on Friday. We get eurozone consumer sentiment today. And this week brings earnings reports from some critical techs, including Alphabet, Intel and Tesla.

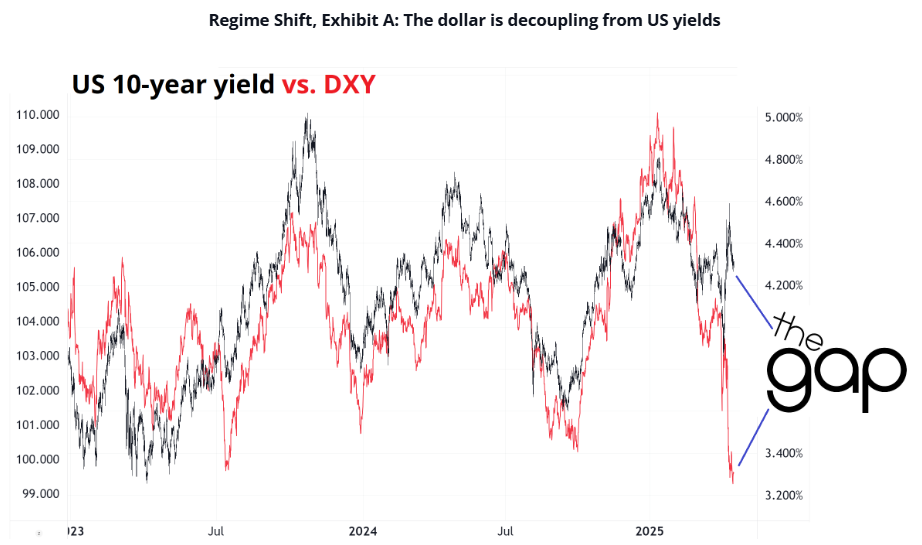

Last week the US stock market shrugged off Trump’s threat to fire Fed chief Powell, but it lingers as a dollar negative this week with as much muscle as the tariff war itself. On Friday Economic Council chief Hassett said Trump is studying it (after a press report that toadies are working on a position paper). Brown Bros says the very idea of studying it is a horrible thing. Bloomberg reports “Hedge funds are now the least bullish on the greenback since October, Commodity Futures Trading Commission aggregated data showed.”

The WSJ names it “Sell America.” The FT names it the top factor in the dollar drop. Reuters pulls no punches and has the headline: “Stocks, dollar slide as Trump's attacks on Fed shake markets.” Bloomberg writes “Trump’s Push Against Powell Fuels Doubts About US’s Haven Status.”

Chicago Fed Goolsbee said yesterday he hopes the independence of the central bank is not at risk. The Fed’s independence from political pressure has been copied around the world, although New Zealand probably get the credit for the origin, and historically, is the lion’s share of its global credibility.

Again we have yields rising but the dollar falling. We even have the yield differential with the Bund rising in the US favor and still the dollar falls. As the TICs report last week showed, foreign central banks are still buying US Treasuries, but fund managers, insurance companies, and other non-government entities are selling. US brokers report big new interest in non-US markets. China is reported to pulling back from US private equity (FT).

We remain puzzled by the collapse in the 10-year yield (tariff-driven) that reversed when Trump announced the pause. Was this a one-time thing? How worried should we be about a repeat that lacks such an easy fix? The very smart Brent Donnelly sees disconnects in several places, especially the yield and the dollar. Also the yen and the Nikkei, and the Bund and the euro, even as the ECB was cutting rates.

Press reports have it that Trump issued the tariff pause on the advice of the TreasSec and CommerceSec while Navarro was out of the room, but still in the building. The tariff pause rescued the stock and bond markets from a crisis meltdown. We guess it will take something equivalent to the pause to halt, even temporarily, the assault on the dollar. Trump will have to say he wasn’t serious about firing Powell. It will be a lie, of course, but it would probably work.

Forecast

There was a mention of the FX market “freezing up” last week. This is not accurate but does remind us that when trading in thin, we get gaps and other abnormalities (like the abandoned baby candlestick).

It was the tariff “pause” that stopped the crisis in Treasuries and it will take some kind of statement supporting the independence of the Fed to stop the dollar crisis. It will take extreme pressure from the TreasSec to get this and since Trump wants a weaker dollar anyway, we doubt it is forthcoming. That means further dollar losses. But again, the slightest whiff of relenting can trigger profit-taking and a big, fat correction.

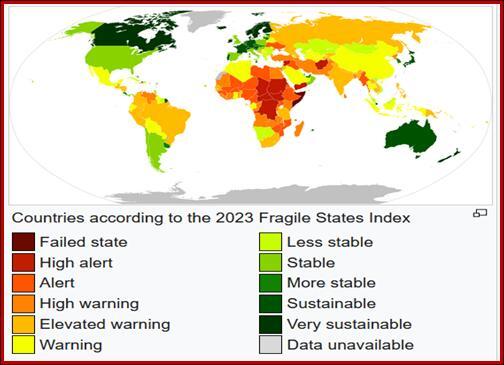

Tidbit: The dollar collapse leads us to wonder how bad conditions have to be, as shown by yields and currencies, before we can name a failed state. What comes to mind instantly? Russia. Venezuela. Iran. A Google search yields Somalia, Sudan, Syria, Afghanistan, Yemen, Haiti, the Central African Republic, the Democratic Republic of the Congo, and Libya.

Since most of those do not have bond issuance or currencies of any meaningful measure, we need another word. Polite sites prefer “fragile” to “failed.” It seems odd to shove the US into either category since the US is hardly an “emerging economy” or similar in any other way. Wikipedia reports that an outfit named Fund for Peace does rank most countries according to a slate of seriousness. See the map. As of 2023, the US was at the 7th level at “less stable,;’ presumably because of the debt. Note that Canada gets the highest rating, “very sustainable.” And we can expect Canada to keep it while the US will likely fall further now that we have an incompetent in the White House.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat