Think ahead: Central banks tread carefully, for now

Hotter-than-expected US inflation data has shifted the dial towards a smaller 25 basis point rate cut from the Federal Reserve this month. The Bank of England is likely to do nothing at all. But both may find themselves speeding up the pace of easing as the year wears on. Here’s our guide to the week ahead.

This week’s THINK Ahead is shorter than usual as James Smith is enjoying a well-deserved holiday. He will return next week.

Week ahead in developed markets

United States

Federal Reserve interest rate cut expectations have been building through the summer as the Fed pivoted to put more emphasis on the cooling labour market rather than above-target inflation. On 23 August Fed Chair Jerome Powell was as clear as can be that “the time has come for policy to adjust, the direction of travel is clear”. As such, the main question was whether it would be a 25bp or 50bp cut.

We had favoured a larger move as an insurance policy against the prospect of more significant job weakness in the future, but the most recent jobs report was not as weak as feared and August core CPI came in hotter than hoped at 0.3% month-on-month. Given this backdrop, we have to admit a 25bp move now looks the most probable outcome with the current market pricing being for 35bp – effectively a 25bp is baked in with a 45% chance that the Fed goes for a 50bp cut.

We think there will be some members who do vote for a 50bp move and it will likely be close. Business surveys paint a gloomy picture of slowing activity and hiring while the Fed’s own Beige Book suggested that only three Fed regions of the US experienced “slight” growth in the previous eight weeks – The Fed’s Boston, Chicago and Dallas Fed banks – while the other nine reported flat or declining output. We expect a narrow vote in favour of 25bp, but with the central bank leaving the door open to a larger move at some point. We expect 100bp of cuts this year with a further 100bp next year.

United Kingdom

Inflation (Wed): Services inflation is likely to notch a fair bit higher in the August data. That sounds bad, but this is down to basis effects in price categories that we know the Bank of England is minded to ignore. That’s things like package holidays and hotels which have been volatile recently, and our favoured measure of “core services” inflation that strips out these categories is likely to stay unchanged, down at 5.1%. The Bank itself is braced for a temporary rise in services CPI this autumn before it predicts it will fall back again by year-

end.

Bank of England decision (Thu): With services inflation still elevated, the Bank of England is treading more carefully than the Federal Reserve towards lower interest rates and that suggests the committee will vote for no change this month. We doubt we’ll see officials move in a more dovish direction just yet. That could start to change, however, assuming signs of lower wage/price expectations begin to show through in the official numbers. We expect back-to-back rate cuts beyond November.

Week ahead in EMEA

Poland

Industrial output (Thu): Poor external demand, especially the weakness of Germany's automotive industry, is holding back the recovery in Poland’s manufacturing sector. We expect industrial output growth in August at just 0.5% year-on-year as compared with 4.9% YoY in July, when the reading was boosted by favourable calendar effects. Still, 3Q24 is projected to be slightly stronger in annual terms for domestic manufacturing than previous quarters, supporting the ongoing economic recovery in Poland.

PPI (Thu): Producer price deflation still prevails. We forecast that in August, PPI fell by 4.9% YoY i.e., at a similar annual pace as in July, when prices fell by 4.8%YoY. We project deflation will be seen at least until the end of the year. Price levels have been broadly stable from the beginning of 2024 and annual deflation has been mainly driven by high base effects.

Wages (Thu): Although wages continue to expand at a double-digit rate, the upward pressure has eased somewhat over recent months. According to our estimates in August, average paid wages in the enterprise sector went up by 11.3% YoY after rising by 10.6% YoY in July. In 1H24, average wage growth in businesses was close to 12% YoY. Wage growth should continue to moderate and ease into single digits in 2025.

Employment (Thu): Employment in businesses has been declining slightly this year so far, but the scale of deterioration is small. We forecast that in August, the number of posts fell by some 5K vs. July, which translates into a 0.3% YoY decline after an annual drop of 0.4% in July. Soft indicators and surveys published recently suggest that demand for labour is stabilising and likely to recover in the coming months.

Czech Republic

Given the mediocre performance of domestic and eurozone industries, Czech producer price inflation likely remained subdued. Sluggish foreign demand clearly limits the pass-through of rising wage costs to selling prices, which will be absorbed in margins to a large degree. Lower energy prices will also contribute to tepid pricing in the industry.

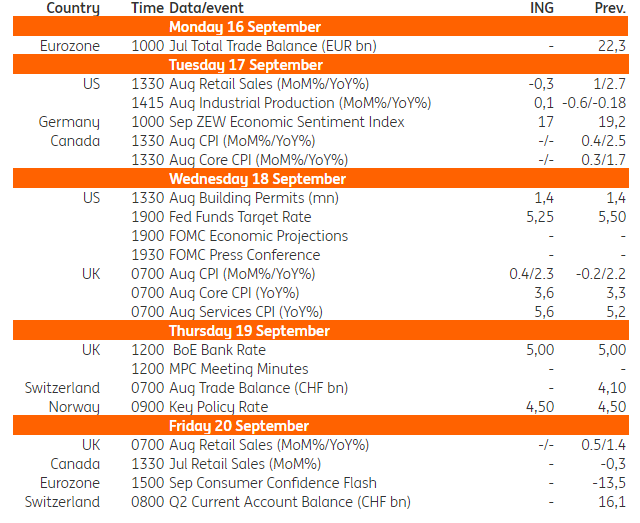

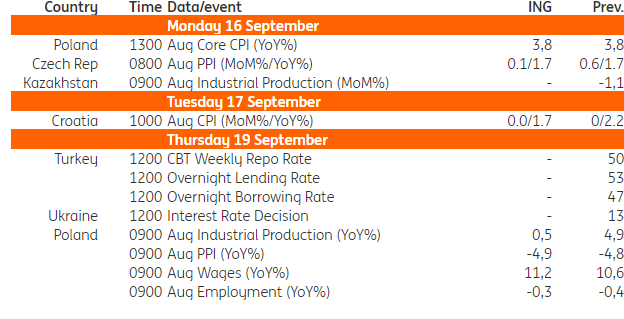

Key events in developed markets next week

Source: Refinitiv, ING

Source: Refinitiv, ING

Read the original analysis: Think ahead: Central banks tread carefully, for now

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.