There's no universe in which no-deal Brexit favors the Pound

Outlook:

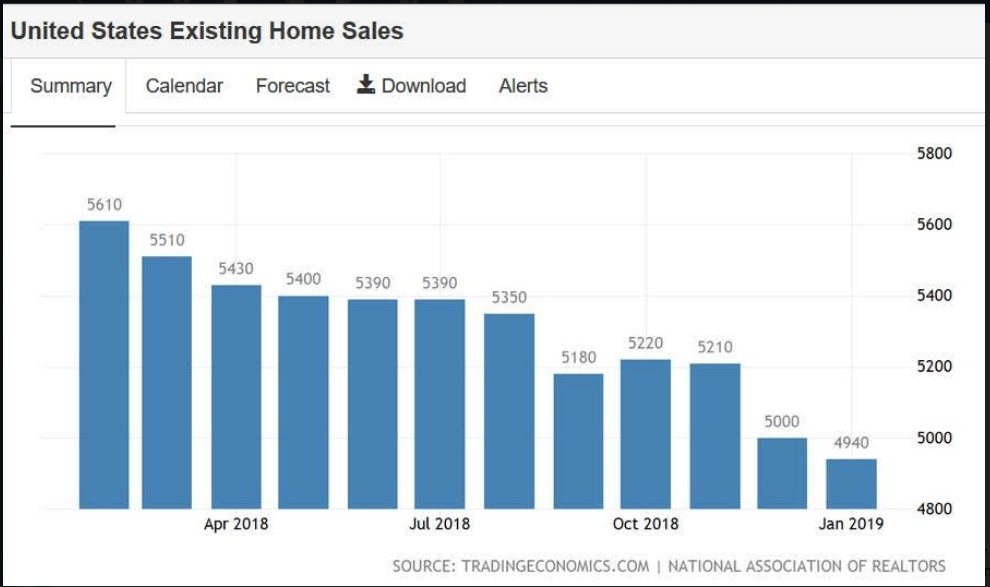

We get the flash PMI today and existing home sales, likely to show the downward slide has ended now that mortgage rates are retreating. See the chart. Economic data has only a fleeting effect these days—central banks rule the airwaves, and politics. One cause is the 35-day government shutdown that has delayed data. We seem to think that because it’s old data, it can be ignored. We doubt that, but never mind. Nobody else’s data is delayed. And even with delayed data, the Atlanta Fed is going to issue a new Q1 GDP forecast today. It was 0.4% last week. What’s going to happen to the stock market if the Atlanta Fed comes up with zero? Or 1%? The Atlanta Fed overshoots but gets the direction right.

Next Friday is Brexit day, now postponed to April 12 or if Parliament passes the Withdrawal Bill on the third try, May 22. EC Pres Tusk said the UK has a choice among the May deal, no deal, a long extension, or revoking Article 50. Tusk went on, “The 12th of April is a key date in terms of the UK deciding whether to hold European Parliament elections. If it has not decided to do so by then, the option of a long extension will automatically become impossible."

There is acutally a fifth choice—a new deal, aka pulling a rabbit out of the hat. How on earth could May cobble together an alternative plan in two weeks? Not likely—but not impossible. The bill has to be changed in order to be allowed on the floor, anyway. But May doesn’t have an alternative plan, does she? Or we would have seen it before. Assuming an alternative plan is fiction and assuming Parliament rejects any and all plans anyway, the UK is going to crash out of the EU without a deal. From this side of the pond, it seems May must resign, too.

Sterling has recovered over 100 points off yesterday’s low at 1.3003 for reasons we cannot fathom. The mini-chart below shows the pound has been flat, net-net, for almost two years (since June 2017). Granted, where you start a channel has a lot to do with whether it’s sloping up or down, and we could draw it seventeen other ways, but the point of this particular chart is that uncertainty breaks about 50-50. It shouldn’t. There is no unvierse in which crashing out of the EU without a deal or a domestic plan can favor the pound. It’s possible that a May resignation will deliver a rally, but a short-lived one.

Sterling aside, it’s hard to see why the dollar recoverd so robustly. The only reason we can find is that conditions are so bad elsewhere and those central banks are retreating back into QE/stimulus, and that includes Japan and Europe as well as China. The Markit PMIs from Europe today are really, really bad. The German manufacturing PMI is the lowest since 2012! Bloomberg notes the reading of 44.7 misses the forecast of 48 by a lot. The Bund yield even turned negative for a few minutes. The Japanese 10-year is also negative (-0.07% from -0.04% yesterday).

Not to be old-fashioned, but negative yields in major countries is just awful. The Fed may have capitulated, but we still had four hikes last year and a contraction of the Fed balance sheet. It ain’t normalization by a long short, but nobody else is even close to normalization. The Fed may have only one or two arrows left in the quiver, but nobody else has any.

And not to beat a drum, but Trumpian destabilization of the world stage provides an incentive to seek a safe haven. In foreign affairs, the Trump gang is throwing crockery against the walls. It wants to sell fighter jets to Taiwan, annoying China. It wants to recognize the Golan Heights as Israeli territory, something that violates a UN resolution saying territory taken in war can’t be kept permanently. Russia is cheering (because now it can keep the Crimea with the US’ blessing). Bibi is putting up posters of Trump all over the place in his bid for re-election in the face of a charge of corruption. And both China and Russia, which lent vast sums to Venezuela, are supporting Maduro while the US supports the contender. Whatever happened to the Monroe Doctrine? (everyone else stay out of the Western hemisphere, it’s the American sphere of influence).

Given negative yields elsewhere and uncertainty about quite how deep the soup into which the US economy is plunging, maybe the dollar has a fighting chance—and that upside euro breakout was, indeed, false.

Tidbit: In domestic affairs, chatter is getting louder about the imminence of the Mueller report on Russian interference in the presidential campaign. It has no basis except wishful thinking. Even if the report were issued soon, it goes to the Attorney General first and he may sit on it as long as he likes. He can also show it to the White House and allow redactions in the name of executive privilege. In the absence of a smoking gun, nobody expects an indictment of Trump himself or Don Junior; undoubted campaign law violations are not substantial enough to trigger an indictment or impeachment. Mueller may have other stuff that is substantial enough—money laundering, for example. There’s a small possibility that Trump disrespecting war hero McCain repeatedly will ruffle Senate Republican feathers enough for them to grow a spine, but we can’t count on it.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat