The weekender: NFP Friday unfolded as a double whammy of the worst sorts

Markets

Friday’s US jobs report detonated like a financial bombshell, sending shockwaves across Wall Street as stocks tumbled and bonds buckled under the unexpected vigour of the American labour market. Nonfarm payrolls skyrocketed to a staggering 256,000, obliterating the forecasts and sending a clear signal: the US economy is not just alive; it's kicking hard. This explosive revelation puts a firm pause on any whispers of imminent rate cuts, with the Federal Reserve now perched on a tightrope of robust economic indicators.

Simultaneously, US consumer inflation fears have been ignited and fueled by the spectre of Trump-era tariffs. The University of Michigan’s survey threw gasoline on the fire, with one-year inflation expectations surging to a searing 3.3%—levels unseen since last May and a stark jump from December's 2.8%. This sharp spike in inflation expectations, especially among the nation's lower-income and politically independent groups, underscores a growing unease about the future economic landscape, fraught with inflationary landmines.

With this week's CPI data looming like another macro storm cloud, December’s job data isn't just a report—it's a dramatic overture to a year that could be dominated by high economic drama and the relentless drumbeat of tariff threats.

December's robust employment data has stoked fears of an overheating economy, and with traders bracing for Trump’s next move and inflationary pressures building, the financial stage is set for 2025 filled with intrigue and suspense, where every economic indicator could drop like a bomb in the ongoing saga of US fiscal and monetary policy.

Surprisingly, "bear flattening" wasn’t on many traders' radars going into NFP Friday, but it sure was coming out. As the US session closed, the front end of the curve took the hardest hit from the fallout of another robust payroll report. Meanwhile, the dollar surged, except for its performance against the yen. It strengthened as hotter US economic data should encourage the Bank of Japan to hike if its focus is genuinely on external economic factors. For the Fed and market bettors alike, Friday unfolded as a double whammy of the worst sort: a vigorous US job market wrapped in escalating inflation expectations, challenging any hopes of imminent rate cuts and stirring a tumultuous end to the trading week.

Last week proved challenging for equity markets as they stumbled into 2025, grappling with tariff concerns and escalating bond yields. The S&P 500 took a notable hit, sliding 1.9% over the week. Sectors like technology, financials, and consumer discretionary bore the brunt of the downturn, reflecting the broader market's struggle to find footing amidst the unfolding economic uncertainties.

Nuts and bolts

As we count down to Trump's inauguration, the economic fireworks are exploding early. In his latest press barrage, Trump lobbed threats toward Canada, Panama, Greenland, and Denmark, culminating with a stark ultimatum about Middle Eastern stability—his rhetoric a potent mix of negotiation and intimidation that’s sending shockwaves through global markets.

Despite the geopolitical drama, the U.S. labour market is a juggernaut. December's job numbers soared to a staggering 256,000 new roles, slashing unemployment to 4.1%. But here’s the kicker: the Federal Reserve, while buoyed by the job surge, is treading carefully, eyes glued to wage data which cooled to a growth of 3.9%, signalling they’re not ready to hit the rate cut button just yet.

Meanwhile, inflation is like a shadow looming over the Fed's shoulder, especially with CPI expected to tick a troubling 2.9%. Core inflation remains stubbornly high, and the ominous ISM Prices Paid Index suggests further heat. If Trump slams down the tariff gauntlet post-inauguration, we could see inflation sprinting, leaving the Fed grappling with an even stricter policy puzzle.

The markets are in a tizzy, with the U.S. Trade Policy Uncertainty Index skyrocketing to heights unseen since Trump’s first term. The absence of a December Santa Claus rally underscores the jittery mood on Wall Street as investors brace for what might be a rugged start to 2025. The bond market's earlier optimism has evaporated, with Treasury yields spiking—a direct response to a Fed suddenly wary of more hawkish horizons.

Moreover, the December FOMC minutes reflect a Fed grappling with the implications of Trump's potential policy shifts. Several members advocated holding off on rate cuts due to rising inflation risks. This sentiment has propelled long-term real Treasury yields to new heights, starkly contrasting the market’s earlier predictions of multiple rate cuts in 2025. Of course, this is bad news on multiple levels for global stock markets.

We're just days into 2025, yet the landscape is already tumultuous with policy shifts and heightened market reactions. As we navigate this storm, one can only hope for stabilizing news that might soothe the markets' nerves and provide more explicit direction. In the meantime, it seems prudent to brace for continued volatility and perhaps keep Alka-Seltzer within reach.

Forex market

When the macro risks align with the Trump risk factors—like a hawkish Fed, higher rates, and a stronger dollar—the market typically sees somewhat of a one-way trend, and that is precisely what happened on Friday as the DXY is nudging ever so closer to the key 110 level. However, USDJPY could be an exception. Recent wage data from Japan for November highlight a robust economic recovery, with significant wage increases pointing to a solid link between wage growth and inflation. This substantial wage growth is tipping the odds in favour of a potential Bank of Japan rate hike in January.

Yen traders should keep a close eye on the Nikkei press. Given the upheaval in financial markets following the BoJ's last rate hike in July, the central bank is likely much more cautious. They will likely guide the market through press leaks, much like the Fed does with WSJ’s Nick Timiraos and the FT’s Colby Smith to minimize any collateral damage. Bloomberg has already reported that the BoJ is "mulling its January rate decision," with an additional story noting that the BoJ might raise its inflation forecast due to rising rice prices and the ongoing yen depreciation. The actual telegraph, if there is one, however, will come through the local Tokyo press, so it is best to keep an eye on Japanese business news.

Chart of the week

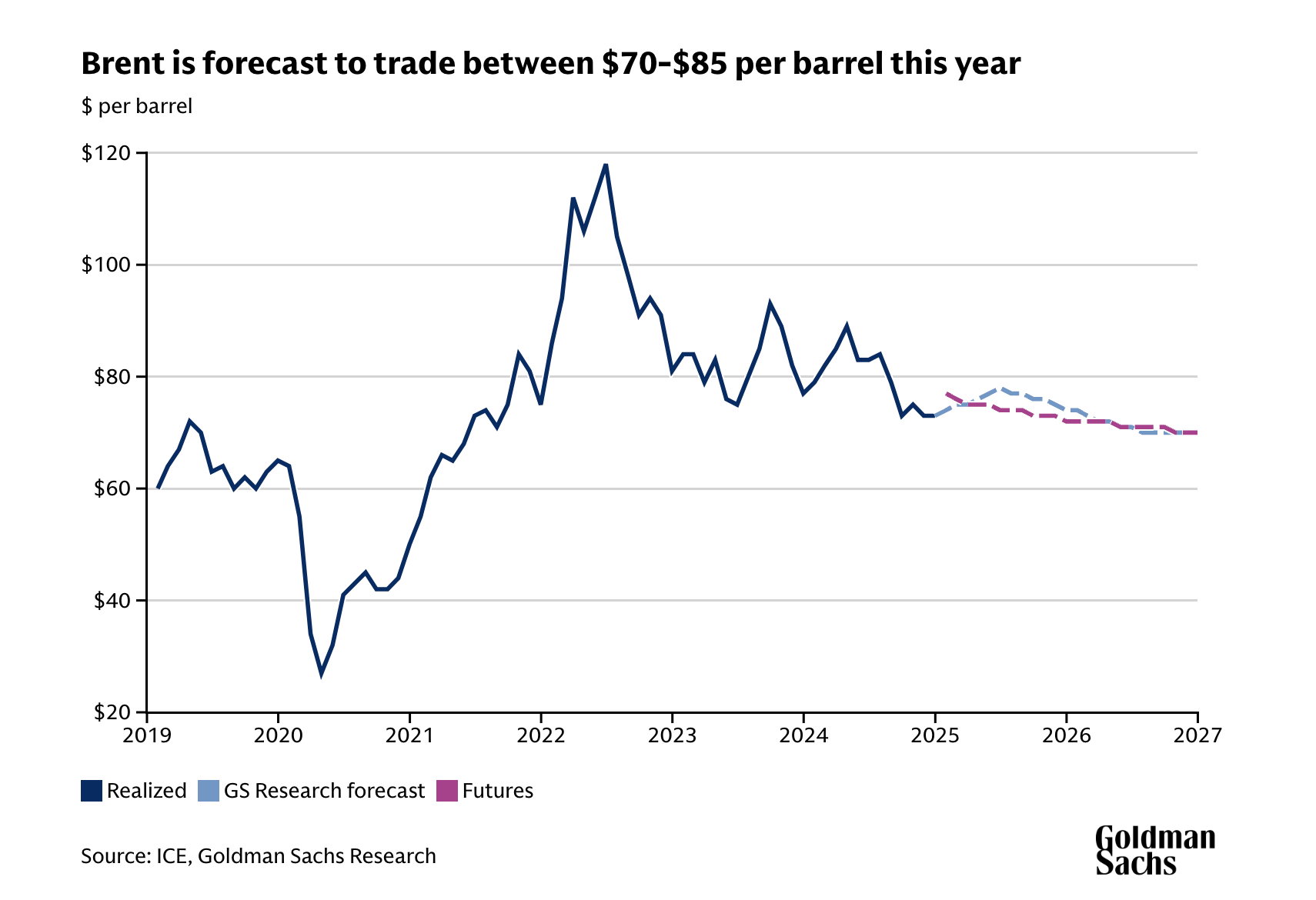

Spare capacity could cap oil prices again this year.

Goldman Sachs Research has set its forecast for Brent crude oil in the upcoming year. It anticipates a trading range between $70 and $85 per barrel, with an average expected to hover around $76. This projection comes after a year in which oil prices averaged about $80 per barrel but experienced dips into the low $70s during certain periods in 2024. This outlook suggests a slight softening in prices but maintains a relatively stable market scenario for Brent crude.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.