Breaking: Canada headline CPI rose 2.3% YoY in January

Canada’s inflation eased a tad in January, with the Consumer Price Index (CPI) rising 2.3% YoY, slightly below what markets were expecting, after a 2.4% increase in December. On a monthly basis, prices came in flat.

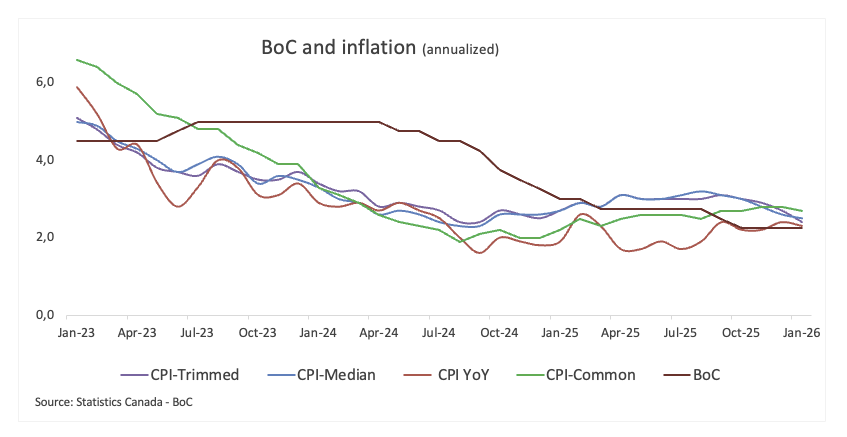

The Bank of Canada’s (BoC) core measure, which strips out the more volatile items like food and energy, rose 2.6% over the past year and gained 0.2% vs. the prior month.

Looking at the BoC’s other key inflation gauges, Common CPI came in at 2.7% (from 2.8% ), Trimmed CPI at 2.4% (from 2.7%), and Median CPI at 2.5% (from 2.6%). Together, they show that underlying price pressures are still fairly sticky, albeit trending downward.

According to the press release: “The gasoline price index was the largest contributor to deceleration in headline inflation, with a larger decline in January compared with December… Indexes with year-over-year movements impacted by the temporary GST/HST break in January 2025 continued to put upward pressure on the year-over-year all-items increase in January 2026. Of the affected indexes, the CPI continued to be most impacted by acceleration in prices for restaurant meals and, to a lesser degree, prices for alcoholic beverages, toys and children's clothing.”

Market reaction

The Canadian Dollar (CAD) remains on the defensive in the first half of the week, prompting USD/CAD to extend its recovery and trade with decent gains around the 1.3650-1.3660 band in the wake of the release of Canadian inflation prints in January.

This section below was published as a preview of the Canadian inflation report for January at 08:00 GMT.

- Canadian inflation is expected to rise by 2.4% YoY in January.

- The core CPI is still seen well above the BoC’s 2% target.

- The Canadian Dollar has given away some gains vs. the US Dollar recently.

The publication of Canada’s January Consumer Price Index (CPI) figures on Tuesday will be the focus of attention. Indeed, Statistics Canada data will provide the Bank of Canada (BoC) with a much-needed update on price pressures ahead of its March 18 meeting, where policymakers are widely expected to keep rates steady at 2.25%.

Economists see the headline CPI rising by 2.4% in a year to January, still above the BoC’s target and matching December’s increase. On a monthly basis, prices are expected to rise by 0.1%. The bank will also closely monitor its core measure (which strips food and energy costs), which held steady at 2.8% YoY in the last month of 2025.

Analysts remain uneasy after last month’s inflation pickup, and the risk of US tariffs feeding into domestic prices is adding another layer of uncertainty.

What can we expect from Canada’s inflation rate?

At its latest meeting, the central bank made it clear that policy is broadly where it needs to be to keep inflation close to the 2% target, assuming the economy evolves as expected. That said, officials were equally keen to stress that they are not on autopilot. If the outlook weakens or inflation risks resurface, they stand ready to adjust.

Indeed, on inflation, the tone was cautiously reassuring. Headline inflation is expected to hover near target, with spare capacity in the economy helping to offset some of the cost pressures linked to trade reconfiguration. Still, underlying inflation remains somewhat elevated, a reminder that the disinflation process is not yet fully complete.

Inflation, therefore, remains the key variable to watch. A glance at the latest figures showed that the headline CPI edged up to 2.4% YoY in December, while core inflation eased to 2.8% YoY. Additionally, the bank’s preferred gauges, CPI-Common, Trimmed Mean, and Median, also moderated, but at 2.8%, 2.7%, and 2.5%, respectively, they continued to run above the 2% objective.

When is the Canada CPI data due, and how could it affect USD/CAD?

Markets will fully focus on Tuesday at 13:30 GMT, when Statistics Canada publishes January's inflation figures. There’s a sense of nervous anticipation, with traders wary that price pressures may prove more stubborn than hoped and keep the broader uptrend intact.

A hotter-than-expected print would likely reignite concerns that tariff-related costs are finally filtering through to consumers. That, in turn, could nudge the BoC towards a more cautious tone in the near term. It would also tend to lend the Canadian Dollar (CAD) some short-term support, as investors reassess a policy outlook that increasingly hinges on how trade tensions and their impact on inflation unfold.

Pablo Piovano, Senior Analyst at FXStreet, notes that the Canadian Dollar has surrendered some gains in the last few days, motivating USD/CAD to rebound modestly past the 1.3600 hurdle, all following its YTD floor just below the 1.3500 support reached in late January.

Piovano indicates that the resurgence of a bullish tone could prompt spot to confront the February top at 1.3724 (February 6), ahead of the provisional 55-day SMA around 1.3760. Further up comes the always relevant 200-day SMA near 1.3820, prior to the interim 100-day SMA near 1.3870 and the 2026 ceiling at 1.3928 (January 16).

On the flip side, Piovano points out that a key support lies at the 2026 bottom, at 1.3481 (January 30). The loss of this level could open the door to a visit to the September 2024 floor at 1.3418 (September 25).

“In addition, momentum indicators continue to lean bearish: the Relative Strength Index (RSI) approaches the 45 mark, while the Average Directional Index (ADX) near 28 is indicative of quite a firm trend,” he says.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Bank of Canada FAQs

The Bank of Canada (BoC), based in Ottawa, is the institution that sets interest rates and manages monetary policy for Canada. It does so at eight scheduled meetings a year and ad hoc emergency meetings that are held as required. The BoC primary mandate is to maintain price stability, which means keeping inflation at between 1-3%. Its main tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Canadian Dollar (CAD) and vice versa. Other tools used include quantitative easing and tightening.

In extreme situations, the Bank of Canada can enact a policy tool called Quantitative Easing. QE is the process by which the BoC prints Canadian Dollars for the purpose of buying assets – usually government or corporate bonds – from financial institutions. QE usually results in a weaker CAD. QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The Bank of Canada used the measure during the Great Financial Crisis of 2009-11 when credit froze after banks lost faith in each other’s ability to repay debts.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the Bank of Canada purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the BoC stops buying more assets, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Canadian Dollar.

Author

FXStreet Team

FXStreet

Composed of a group of economic journalists and FX experts, the FXStreet content team produces and oversees all content published on FXStreet. It provides a purely journalistic approach to the Forex market.