RBNZ preview: Watch for hawkish hints

The Reserve Bank of New Zealand will likely keep rates unchanged on 18 February. However, inflation and policy rate projections may be revised higher, at least partly validating tightening expectations for this year. We expect two rate hikes from 3Q, taking rates to 2.75% by year-end and offering medium-term support to NZD.

RBNZ must address higher inflation

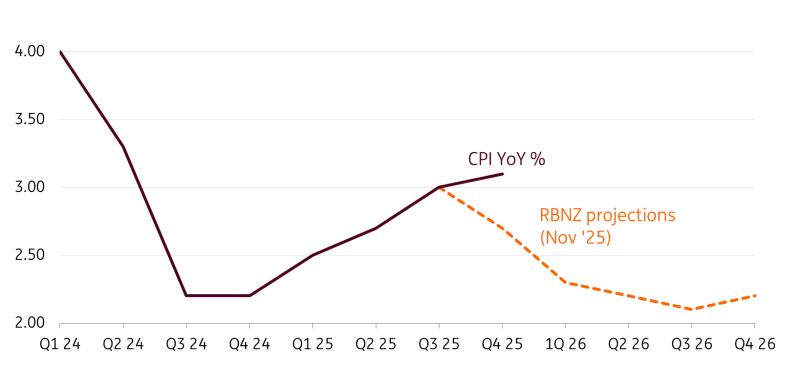

The latest RBNZ projections from November 2025 have proved too optimistic on disinflation. Fourth‑quarter CPI came in at 3.1% YoY versus the bank’s 2.7% estimate, and non‑tradable CPI at 3.5% versus the 3.2% projection. This raises the question of whether the RBNZ cut rates too aggressively last year.

The next few quarterly prints may be a make‑or‑break moment for NZD. Another hot reading could leave the RBNZ with little choice but to start considering rate hikes later this year. However, the 1Q CPI report is only published on 20 April, and there are two RBNZ meetings before then (18 February and 8 April) that should offer some guidance on the policy path.

Inflation projections look too rosy

Source: RBNZ, Macrobond, ING

First meeting for Anna Breman

This February meeting carries significant weight, as markets will get their first real chance to assess the RBNZ’s reaction function to strong inflation data under new Governor Anna Breman. During her time at the Riksbank, she tended to sit on the dovish side of the spectrum, a reputation that may be reflected in the NZD curve, which currently prices no rate hikes until 4Q26. Markets also tend not to price meaningful tightening ahead of a general election, scheduled for 7 November in New Zealand.

Breman’s speeches since taking office have not been particularly dovish, though. She has kept all options open, warned against too aggressive tightening expectations and reiterated optimism on 2% inflation, but equally stressed that tightening in an election year won’t be a problem and that policy will change if the inflation picture does.

New projections will be key

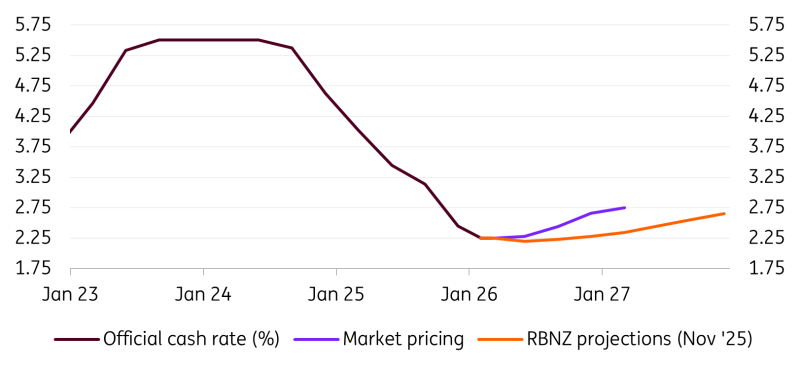

The chances of a rate change at this meeting are very low, so forward-looking language and, above all, new economic projections will drive the market reaction. The November rate path showed a first hike only in 2Q27, but that assumed headline inflation falling to 2.2% in the second half of 2026. A revision higher in inflation numbers would make a strong case for bringing forward the expected rate hike.

In our estimates, inflation will not fall below 2.4% at any point this year, and we currently expect a 1Q print around 2.7 to 2.8%, well above the RBNZ’s 2.3% estimate. If the RBNZ staff are using similar assumptions, we could see a materially higher revision in inflation and the rate path.

Even if that doesn’t fully align with the roughly 40bp of tightening priced in for year‑end, simply signalling a first hike in 1Q27 would likely validate current market expectations, and could even prompt investors to price in a second hike for 2026. The recent move by neighbouring Australia to lift rates to 3.85% may also be adding a touch of marginal hawkish pressure.

Rate projections dislocating from pricing

Source: RBNZ, Refinitiv, ING

Labour market and growth look OK

The jobs market is also sending relatively hawkish signals. The unemployment rate was 5.4%, slightly above the RBNZ’s 5.3% estimate for 4Q25 – but the entire surprise came from a jump in the participation rate. Underlying momentum looked stronger: 4Q employment growth was 0.5% QoQ versus the RBNZ’s 0.2% forecast, and sharper‑than‑expected declines in net migration could prompt some labour market tightening in 2026.

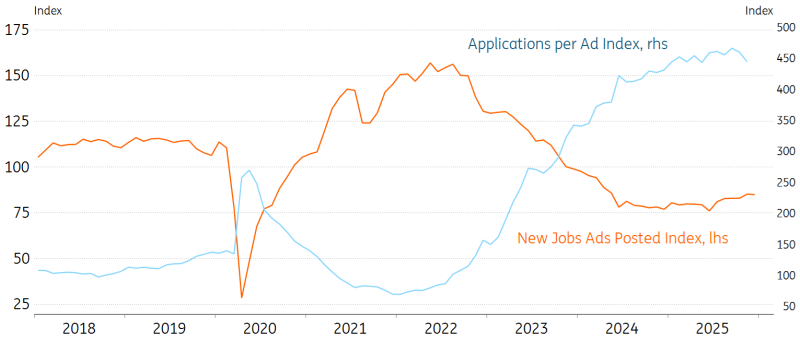

Indicators from SEEK (New Zealand’s largest employment marketplace) show that applications per job ad have remained significantly elevated post‑Covid, while new job ads have been much lower. However, some improvement emerged in 2H25, with these trends gradually starting to reverse.

On the growth side, we do not expect 4Q GDP to deviate much from the RBNZ’s 0.7% QoQ estimate. Forecasts for 2.9% growth in 2026 may not be materially revised at this meeting. The latest Services PMI came in at 51.5 – the first print above 50 since February 2024 – and manufacturing PMIs have been steadily climbing through 2H25, remaining in expansionary territory. Despite a drop in Business Confidence in January, the figure still matches the 2025 average and follows a clear upward trend throughout

Stabilisation in excess jobs applications

Source: ING, Macrobond

Our RBNZ and NZD calls

We expect two rate hikes to 2.75% in New Zealand this year, starting in either September or October. In our view, this will be driven primarily by sticky headline inflation, which should make clear that the 2025 easing cycle went too far. We also think another hike will be needed in 2027 to bring rates back to the 3.0% neutral level.

Market pricing currently implies around 40bp of tightening by the end of the year, with 18bp priced for September, leaving expectations not far from our own call. Rate‑hike speculation has tended to generate an outsized positive currency reaction in Australia, and some hawkish signals at this February RBNZ meeting could see NZD outperform AUD in the near term.

We see upside risks for NZD/USD after the meeting as well, although we remain cautious on further rallies given recent excessively rapid appreciation relative to short‑term drivers. Correction risks remain elevated in the current fragile equity environment. Still, in line with our medium‑term bearish USD view and expectations for RBNZ tightening, we forecast 0.62 by year‑end with upside risks.

Read the original analysis: RBNZ preview: Watch for hawkish hints

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.