The week ahead – End of the month, OPEC, PCE and Chair Powell

Previous trading day events – 24 Nov 2023

US stock markets closed flat for the day on Friday after limited opening and low volumes. However, there were strong gains for a fourth consecutive week, ranging from +0.91% (US100) to +1.27% (US30). The S&P500 added +1.00% last week and peaked at 4575, the next major resistance area remains at 4600.

The decline in the USD and recovery in US Treasuries continued with the USD index closing at 103.42 down -0.39% for the week having hit a 3-month of 103.20 on Tuesday. The bellwether US 10-yr Treasury yield closed at 4.468%.

USOil remained pressured to the downside last week as markets look to this week’s OPEC & OPEC+ meetings in Vienna. African producers are looking to increase caps for 2024, whilst rumors about further Saudi Arabian production cuts in 2024 continue. Gold turned to the upside last week, with a breach and break of $1990 and the key $2000 level. The next key upside levels are $2009 from October and $2015 from May.

The short trading week last week continued the theme of earlier in the month as stocks gained and the greenback moved lower, while commodities and Treasurys also gained.

The week ahead

The week ahead brings a close of trading for the month of November, a mix of GDP, CPI & more PMI data and the latest central bank announcement, this week from New Zealand. The key data point could be the Federal Reserve's favoured measure of inflation - personal consumption expenditures - on Thursday.

Monday – November 27

A light data day with ECB President Lagarde at the ECON hearing before the Committee on Economic and Monetary Affairs of the European Parliament and US new home sales & building permits for October.

Tuesday – November 28

The highlight of the day will be the US CB Consumer Confidence data and a raft of Central Bank speakers led by RBA Gov Bullock and ECB President Lagarde, once again.

Wednesday – November 29

Australian CPI data, kicks the day off, quickly followed by the RBNZ Monetary Policy Decision and Press Conference, The European session has the German and Spanish CPI data, before finishing the day with the latest revision of US GDP and a speech from BOE Governor Bailey.

Thursday – November 30

The official China PMI for November is due on Thursday and analysts generally look for a small pick-up and maybe a reading above 50.0. A meeting of OPEC+ is also scheduled today. Eurozone CPI is due and forecast to dip back to 3.1%, with the core seen easing to 3.5%, its lowest since mid-2021. The key US personal consumption expenditure price index rounds off a busy data day.

Friday – December 01

Canadian jobs and ISM Manufacturing PMI data top the data. To round off the week, Fed Chair Jerome Powell will have a chance to push back against the doves at a Fireside Chat, to top a host of other Fed speakers this week.

Forex markets monitor

EUR/USD (27.11.2023, H1) chart summary

Price Movement

The pair continues to gain traction today, having breached the 109.00 level on Friday to post a new 56-day high. The next key resistance levels are the psychological 1.0950, 1.0975 and the key 1.1000. Initial support sits around the 1.0930-20 zone, the 50-hour moving average at 1.0925 and the 200-hour moving average at 1.0900.

Equity markets monitor

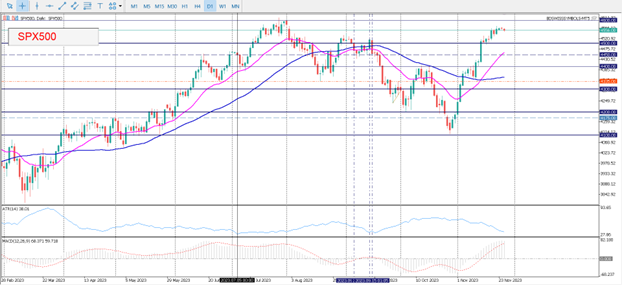

SPX500 – Daily timeframe - Chart summary

Price Movement

US stock markets closed relatively flat for the day on Friday but recorded strong gains for a fourth consecutive week. The S&P500 peaked at 4575 and the next major resistance area remains at 4600. November and December are traditionally positive for stock markets. If the breach of 4500, which is now into its 10th day, cannot be maintained, then the next major support is at 4400 and the 50-day moving average at 4335.

Commodity markets monitor

XAU/USD – H4 timeframe - Chart summary

Price Movement

Last week the gold price reversed significantly and broke the key $2000 zone, having first stalled at the key $1990 resistance. Next support is the 21-period moving average at, the psychological, $2000 and the 50-period MA at $1988. The higher time frame Daily and Weekly charts are both now biased to the upside.

Author

BDSwiss Research Team

BDSwiss

BDSwiss is a leading financial institution, offering bespoke CFD trading and investment products to more than 1.7 million registered clients, in over 180 countries.