The weak statistics increase recession risks

Weak macroeconomic data affected US stocks and the dollar rate

Retail sales in the US for December 2018 decreased by 1.2% compared with November. This is their maximum fall in the last 9 years. Negative has been added by a decline in the producer price index in January and the increase of unemployment over the week. A number of investors have a fear that such statistics indicate a slowdown in the growth of the American economy. Coca-Cola and American International Group (AIG) reporting for the 4th quarter of 2018 was released yesterday. It turned out to be weak, which caused a drop in shares of the manufacturer of soft drinks and the insurance company by 7.6%. Market participants lowered their growth forecast for the companies of S&P 500 index to 16.2% in the 4th quarter. Today at 16:00 CET consumer confidence indicator from the University of Michigan will be published in the United States. Yesterday The ICE US Dollar index slightly decreased , as weak macroeconomic statistics reduces the likelihood of a Fed rate hike.

The euro depreciation has not yet received further development

Eurozone GDP for the 4th quarter of last year grew by 1.2% in annual terms, as expected. This is worse than the 3rd quarter, in which it rose by 1.6%. At the same time, Germany’s GDP showed zero quarterly growth and was weaker than preliminary forecasts. This increases the risk of recession in the EU. Now EURUSD is below the psychological level of 1.13. Many European stock indexes updated 3-month highs yesterday due to the good quarterly reporting by Airbus manufacturer, the British pharmaceutical company AstraZeneca, food and beverage producer Nestle and Commerzbank. At the end of the day, European stock indices still fell due to weak macroeconomic statistics. Today Eurozone trade balance for December will be published. Investors will focus on ongoing US-China trade negotiations.

Japanese Nikkei ended up lower along with other global stock indices

At the end of the week, the Nikkei was still in positive rate by 2.8%. Weak macroeconomic data in the United States reduces the likelihood of further growth of the Fed rate. Due to this, the yield of government bonds of the United States and other countries may decrease. Accordingly, this negatively affected the quotes of Japanese financial companies Dai-ichi Life Holdings (-4.7%),T&D Holdings (-3.5%) and Mitsubishi UFJ Financial Group (-1.4%). USDJPY, Australian and New Zealand dollars strengthened in anticipation of the US-China trade negotiations outcome.

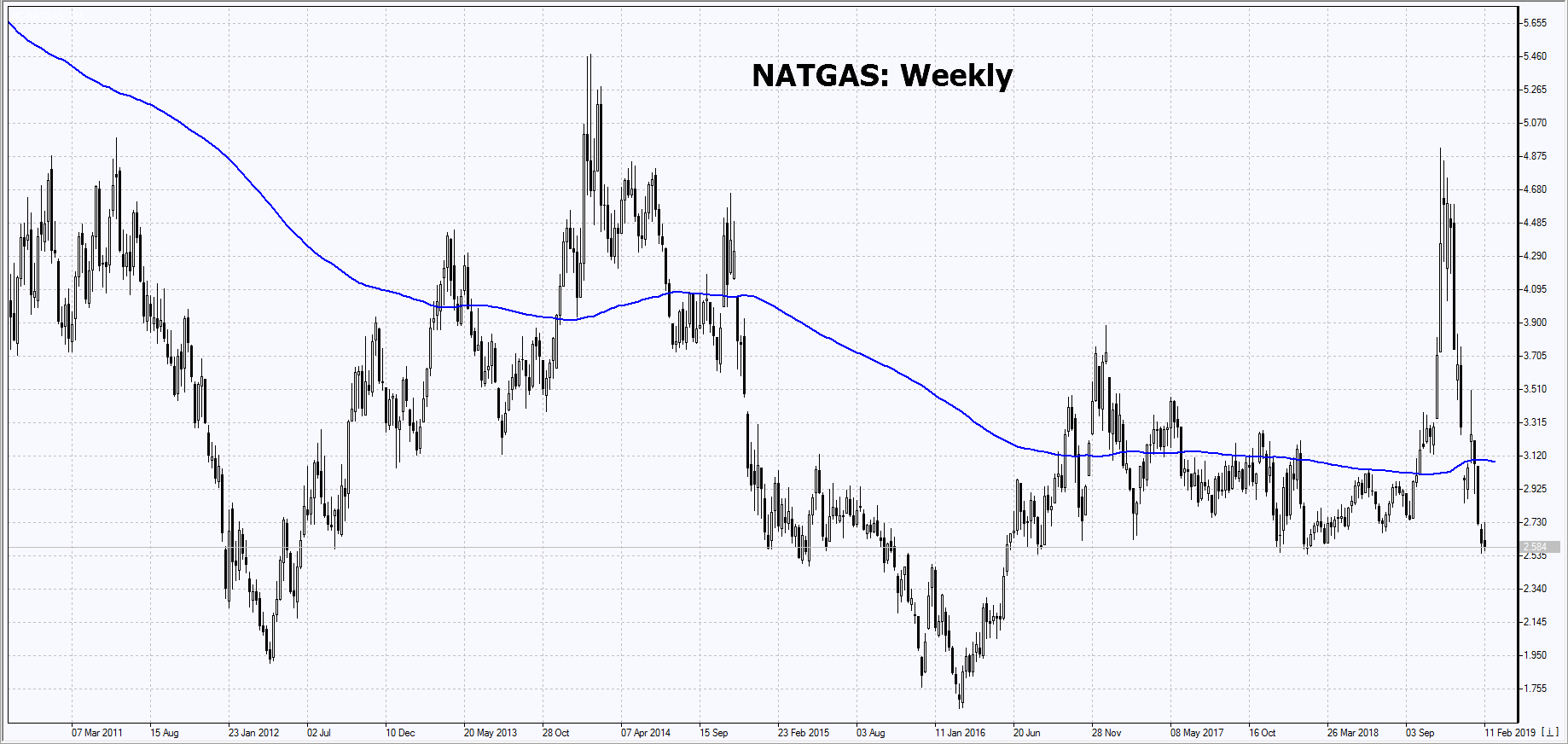

Quotations of US Natural Gas are near the minimum since June 2016

The cost of liquefied natural gas (LNG) in Southeast Asia has fallen to a minimum in 17 years due to the high competition of suppliers. In addition, China has slightly reduced its LNG purchases, waiting the start of Russian gas supplies by the Power of Siberia pipeline. All this reduces the demand for NATGAS. However, there is positive news. According to U.S. Energy Information Administration, gas reserves in the United States decreased by 4.1% over the week and amounted to 53.3 billion cubic meters. This is due to a cold snaps in a number of US states where gas is used for heating.

Want to get more free analytics? Open Demo Account now to get daily news and analytical materials.

Want to get more free analytics? Open Demo Account now to get daily news and analytical materials.

Author

Dmitry Lukashov

IFC Markets

Dimtry Lukashov is the senior analyst of IFC Markets. He started his professional career in the financial market as a trader interested in stocks and obligations.