The volatility in commodities is excessive and not warranted

Outlook: The focus on US and global inflation is premature because the peaks and valleys in commodities are still unfolding. Worries about commodities are rife, especially copper and aluminum, where we can run out of stockpiles this year. Overnight in London, the Metal Exchange suspended trading in nickel after its price doubled for a second day. Bloomberg reports nickel had soared as much as 250% in two days and overnight, “Nickel more than doubled to $100,000 a ton before paring gains and eventually seeing trading suspended on the London Metal Exchange. The exchange said it’s calculating margin calls at the Monday closing price of $48,000 and is considering whether to adjust or cancel the trades made between then and the suspension.” Weirdly, Russia produces only 7% of the world’s nickel.

Wheat is another troublesome commodity, up “as much as 5.4 per cent to $13.63 a bushel in early trading on Tuesday before pulling back to be down 2 per cent, according to Bloomberg data.”

We are not sure that Russia can get away with continuing to sell oil for all that much longer. An increasing number of analysts are telling us to face up to reality—you can have solidarity with Ukraine or you can have green dreams, but not both: bring back coal. In Europe, a summit is planned for Thursday to talk about energy needs, supplies and alternatives. One idea is for Germany to hang on to its few remaining nuclear power plants instead of closing them this year as planned.

Exactly on schedule and exactly as expected, the Trumpy right blames Biden and the Dems for gas prices up over $6-7, but the truth is that it was Nixon in 1973 who called for energy independence and it was Reagan in 1980 who said oil alternative are silly (and result in over-regulation). To be fair, every president of both parties has called for energy independence whether believing in climate change or not, and all of them failed. Jimmy Carter installed solar panels on the roof of the White House (since removed). Nobody knows how much is oil industry obstruction via lobbying and how much is the real difficulty of alternative energy generation. Whatever happened to that bigshot who wanted most of Texas covered in wind farms?

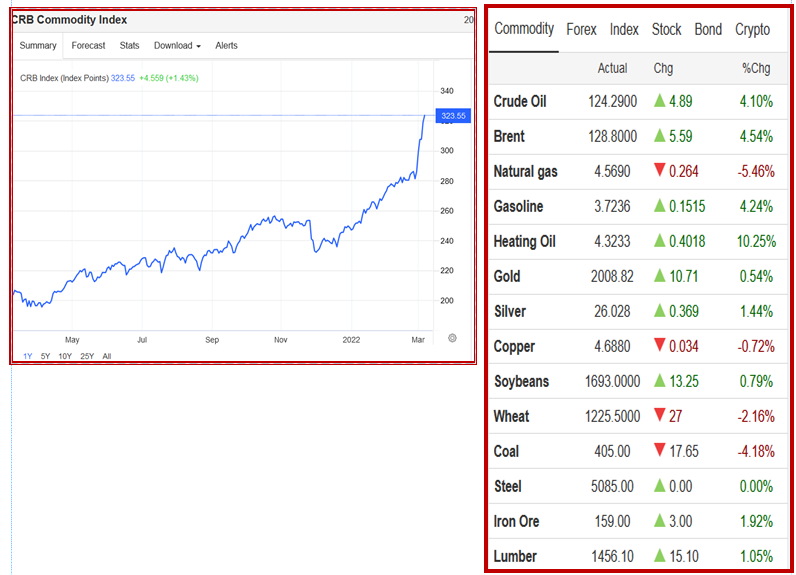

Overall, the volatility in commodities is excessive and not warranted. It’s traders going nuts and getting detached from fundamentals, as we see in nickel. The commodity price index and individual commodity prices shown in the TradingEconomics chart and tables are as of about 8:10 am ET today. Notice that wheat is now down 29%, a ridiculous number that makes sense only in the context of the price having spiked the day before.

This kind of unfettered Wild West speculation is what we imagine must be behind the weird crash in the AUD yesterday that hasn’t ended yet (but is nearing the 38% retracement level, so hope springs). The other big commodity currency is the CAD, and it’s going the other way. You can’t figure out whatever reasoning might be behind these outcomes because there is no reasoning—it’s the madness of crowds.

We feel the same way about bond prices and yields, and the expected inflation supposedly embedded in them. They do not necessarily reflect any such thing. Expectations about inflation cannot be formed rationally in the absence of hard data on input prices and industrial/consumer demand, and no economist worth his or her salt would dare forecast any of that as a major war is unfolding. To make matters worse from the forecaster’s point of view, classic chart-reading is mostly out the window. We saw the same thing with Brexit—technical analysis standards got busted with unhappy regularity.

So, in the absence of solid-base economic forecasts and the absence of reliable technical rules, what can anyone say about the fate of the dollar? Speak, history. The dollar tends to come out okay, but not in a straight line. The best advice is to forego fast juicy profits and pare positions, if only because your stops have to be enormous these days and that’s the super-high risk.

Ukraine Update: Update is the wrong word—we have such a flood of information that it’s hard to separate wheat from chaff. From Reuters: “Police detained more than 4,300 people on Sunday at Russia-wide protests against Putin's invasion of Ukraine, according to an independent protest monitoring group.” The WSJ had a count of more than 13,000 as of yesterday.

Lithuania’s President Nauseda warned US Sec of State Blinken that a failure to stop Russia’s aggression in Ukraine would lead to a global conflict. As though we don’t understand dominoes.

It took a while, but finally Deloitte, Ernst & Young, KPMG and PricewaterhouseCoopers are leaving Russia. Shell, after a barrage of criticism for buying that Russian tanker, vowed to depart. JP Morgan joined MSCI and S&P in removing Russian bonds from all of its indices. American Express joined Visa and Mastercard.

The list of companies removing themselves from Russia (“self-sanctioning”) or withholding their goods is growing by leaps and bounds. Russians won’t get the latest movies from Hollywood or Levi jeans. At some point, the 60-70% that believe the Russian government’s fictions about the war must begin to get suspicious.

Vanity Fair has an article by Sebastian Junger on why Russia may not win, despite its obviously superior size. With examples from history, the author says three factors together could do the trick. First, clear purpose. Second, leadership. Third, women (even Russians find it hard to shoot women). Ukraine has all three. If Russia doesn’t win fast, it may not win at all.

Separately, a military intelligence expert (Malcom Nance) says Ukraine has a real chance of winning militarily if only the West would supply it with enough equipment, especially aircraft and anti-tank equipment. Nance is impressive (and he thinks so, too.)

About Market Swings: From Ari Gilburt at Seeking Alpha: “As Robert Prechter outlined in his brilliant book The Socionomic Theory of Finance (which I suggest to anyone who wants to learn the truth of how markets work):

"Observers' job, as they see it, is simply to identify which external events caused whatever price changes occur. When news seems to coincide sensibly with market movement, they presume a causal relationship. When news doesn't fit, they attempt to devise a cause-and-effect structure to make it fit. When they cannot even devise a plausible way to twist the news into justifying market action, they chalk up the market moves to "psychology," which means that, despite a plethora of news and numerous inventive ways to interpret it, their imaginations aren't prodigious enough to concoct a credible causal story.

“Most of the time it is easy for observers to believe in news causality. Financial markets fluctuate constantly, and news comes out constantly, and sometimes the two elements coincide well enough to reinforce commentators' mental bias towards mechanical cause and effect. When news and the market fail to coincide, they shrug and disregard the inconsistency. Those operating under the mechanics paradigm in finance never seem to see or care that these glaring anomalies exist."

Gilburt subscribes to the theory that “natural law” dictates cycles and waves in securities prices, which scientists sneer at, but at their peril; Gilburt has a terrific track record. And these days he sees a rally in the major indices like the S&P. Just saying.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat