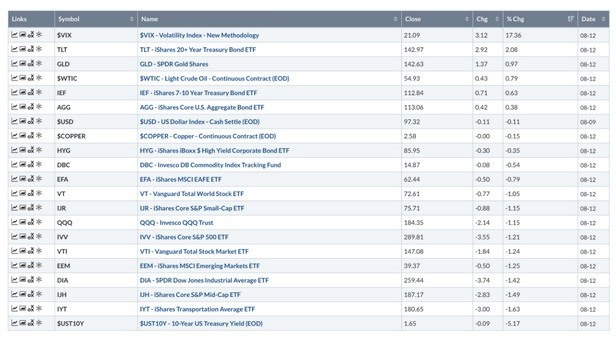

The US dollar was down -0.11%

Highlights:

Market Recap: Stocks dropped again yesterday as the S&P 500 fell -1.21%. The Vanguard total world stock market ETF (VT) dropped -1.05%. Safe haven assets rallied as Treasuries (TLT) rose 2.08% and Gold (GLD) moved up 0.97% on the day. The U.S. dollar was down -0.11%. U.S. 10-year yields fell 9 basis points.

Volatility: The VIX index moved higher by over 17% yesterday. Volatility did make a lower high. If volatility fails to make a higher high, this could be setting up for a bit of a rebound. However, if it continues to break out to the upside, equity market pain could follow.

Treasury Yields: The U.S. 10-year yield is now -34.7% below the 200-day moving average. We expect some sort of consolidation or pull back in yields at some point to clean up this oversold condition. However, the message is clear, growth is slowing and there is no second half rebound.

Transports: Transports are not moving enough goods obviously and are flashing a major problem from a cyclical standpoint. Transports weakness continues to suggest an economic growth slowdown. Transports are not oversold relative to the broad market index (IYT/SPY).

West Texas Intermediate Crude: Crude oil was a bright spot yesterday, moving up 0.79%. A move higher in oil could suggest upside in the markets in the short-run. The question is how long could this last. Positive divergence is also present as RSI has made a series of higher lows while oil held support at 51.

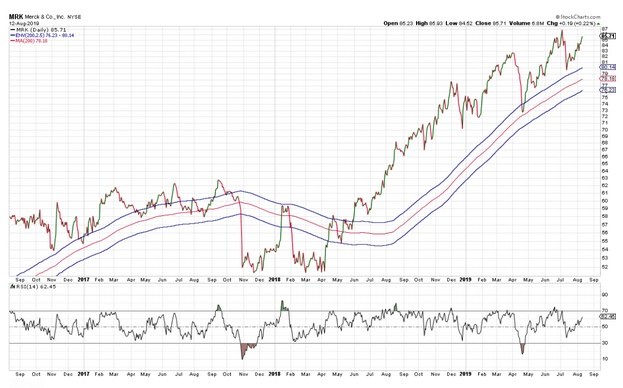

Merck: Merck & Co was the only Dow stock that was positive yesterday, up 0.22%. It remains in a strong positive trend and is close to breaking above previous highs.

Futures Summary:

News from Bloomberg:

Investors fled stocks for the safety of bonds amid global recession fears and growing risks in Argentina and Hong Kong. Asian equities tumbled and S&P 500 futures signaled more losses. The dollar rose with gold and Treasuries extended yesterday's big gain. Negative 10-year yields arrived in European credit markets and China's 10-year sovereign yields fell to 3% for the first time since 2016. Oil failed to hold on to gains.

Argentina's presidential front-runner Alberto Fernandez said he doesn't want to default on the country's debt, though he criticized incumbent Mauricio Macri for increasing short-term obligations to unsustainable levels. "The market is unwilling to give Fernandez the benefit of the doubt," Aberdeen Asset Management said. Citigroup doesn't expect "significant spillover" to the broader emerging markets.

As Hong Kong's embattled leader Carrie Lam warned that the city risks sliding into an "abyss," travelers were staring right into it. The airport canceled all remaining departures in the late afternoon for a second day as demonstrators continued to swarm the airport. Cathay Pacific shares extended losses. Plans for a march on Sunday were unveiled by the group that organized three large events in June and July. Follow the latest with our rolling coverage.

Economies are feeling the trade war pain. Singapore cut its growth forecast for the year to as little as zero, down from a previous projection of 1.5% to 2.5%. The economy expanded a mere 0.1% in the second quarter from a year earlier. Confidence in Germany's economic outlook worsened for a fourth month in July, with the ZEW index plunging to minus 44.1, the lowest level since 2011. And Japan's producer prices, machine tool orders and tertiary industry index were all in the red.

Wall Street watchdogs are about to cut banks some slack on their ability to trade with their own funds. Regulators may complete work next week on rewriting much-maligned aspects of the Volcker Rule that would give banks the benefit of the doubt about short-term trades being compliant, people familiar said. The changes would still require approval by five agencies led by the Fed.

Author

Clint Sorenson, CFA, CMT

WealthShield