The Trump threats against Cuba and Greenland are very real

Outlook

Today we get the usual jobless claims, the New York and Philly Fed reports, and import/export prices. None of these have a history of being market-movers. The TICS report later might have some juice after the six people who can read the darn thing give their judgments. As we have already seen, the capital flow into US dollar assets has not abated, even if buyers are hedging the dollar. In the first 10-months of 2025, foreign purchases of stocks and bonds were $1.08 trillion, up from $970.5 billion in the same 1924 period and $560.6 billion in 2023.

We admit to not understanding the bond market. Yesterday yields fell across the board with the 30-year under 4.8% for the first time since early Dec. Bloomberg wrote “Catalysts for the rally included a slump in US equity benchmarks, additional haven demand tied to the prospect of the US military action in Iran, and delayed Supreme Court ruling on tariffs that have improved the US fiscal picture.

“Supply considerations were also at play, following strong demand for note and bond auctions over the past two days. Meanwhile, Wednesday’s routine Treasury buyback operation at 2 p.m. New York time targets bonds maturing in 20 to 30 years. Treasuries also drew support from gains for UK government bonds that drove the 10-year gilts to 4.35%, the lowest on a closing basis in more than a year.”

Why is this not silly? The Trump threats against Cuba and Greenland are very real, while the probability of something real happening against Iran is almost zero. On tariff rebates, should the Supreme Cout strike them down, it raises the US debt by definition and so should have the opposite effect on yields. And what does the Gilt market have to do with the price of bread? Around noon, the US 10-year had retreated from a high over 4.179% to 4.14%, leaving the Gilt with a small cushion.

As usual, the real threat lies in the White House. Trump gave an interview to Reuters and displayed the usual serious ignorance. He said “Iran's clerical government may collapse, blamed Ukraine President Zelenskiy for the stalemate in Russia talks and dismissed Republican criticism of a probe of Fed Chair Powell.” Not mentioning his six bankruptcies, he said "A president should have something to say about Fed policy. I made a lot of money with business, so I think I have a better understanding of it than Too Late Jerome Powell."

Forecast

The dollar gets a tailwind from Trump now saying he doesn’t plan to fire Powell and will await the Justic Dept outcome. This is backwards. The dollar should get relief from Trump firing Bondi and erasing the case, but markets can be short-sighted. This is not the TACO the dollar needs. Similarly, the dollar should not be getting relief from the Iran story getting tamped down. We believe Trump is the classic cowardly bully who will not instigate a major military action against anyone who can actually fight back. Venezuela, sure. Iran, no. But the uncertainty should be dollar-negative.

These and other issues are deeply, seriously dollar-negative. Equally disturbing is that nobody knows how to report any of this stuff and forge a narrative that makes sense and can be used to develop a strategy. We seem doomed to whipsaws.

From a trading perspective, this lack of clarity means cutting the amounts at risk.

Food for thought

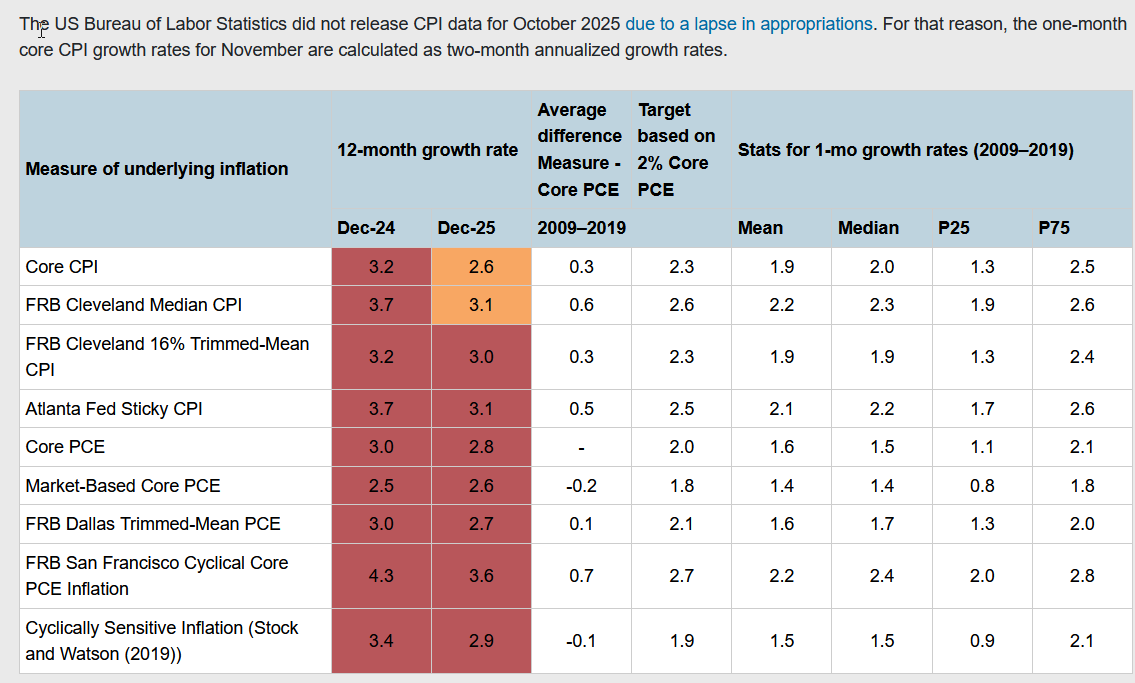

The Atlanta Fed has a report named the Underlying Inflation Dashboard. Mish reports on it so we took a look, too. Notice that none of the forecasters have anything better than 2.6% and the San Francisco Fed has 3.6%. Mish complains that the CPI we just got is a lousy number due to the process, which can’t be fixed. “Homeowners’ insurance, and property taxes, and food are three reasons the CPI is garbage.”

We can complain all day about the market seeing the inflation rate as sort of okay when it’s really pretty bad. The outcome lands in the CME Fed funds betting. If inflation really is okay and stays okay-ish, we can have rate cuts with no harsh worries. Remember that was the deduction by ING when the report came out.

But the CME bettors do not agree and seem to be adopting the Mish interpretation. Those betting no change at the April meeting are 59.2%, vs. 45.1% a week ago and 39.0% a month ago. Moving onto June, those seeing no change at all in rates is still a high 28.5%, with the interesting comparison that it was 18.1% a week ago and 18.6% a month ago.

No cut by June? That has two implications,. First, it’s dollar-supportive. Secondly, it’s a nightmare for Mr. Powell (unless PCE later this month shows something better).

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat