The S&P 500 gained 0.12% yesterday

Highlights:

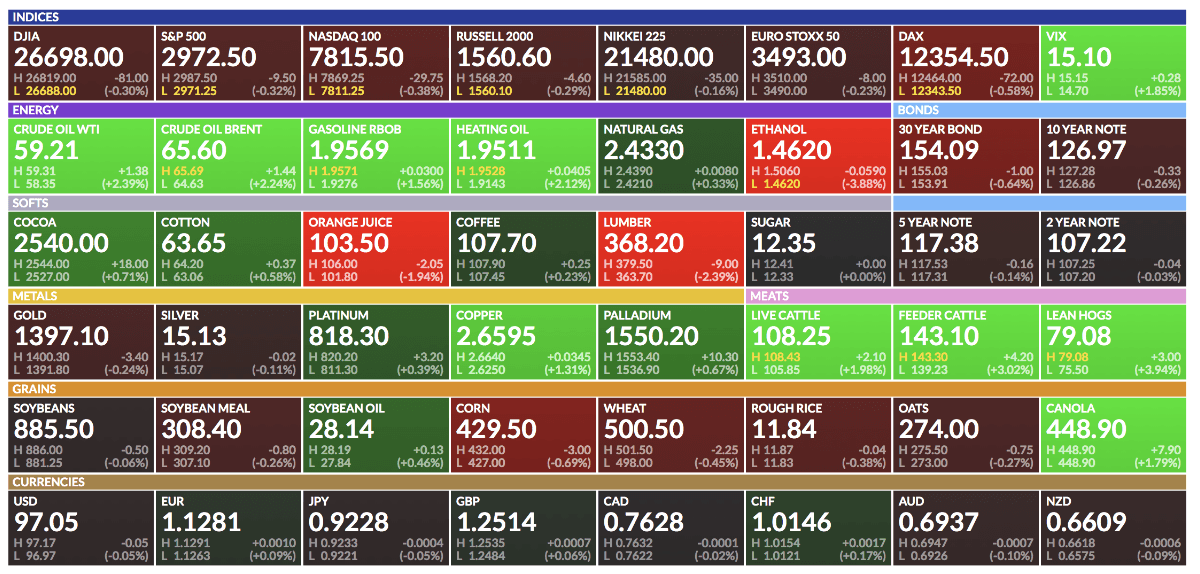

Market Recap: The S&P 500 gained 0.12% yesterday. The benchmark 10-year yield rose 2 basis points and the dollar was also stronger on the day. The Vanguard total world stock market ETF was down -0.16%.

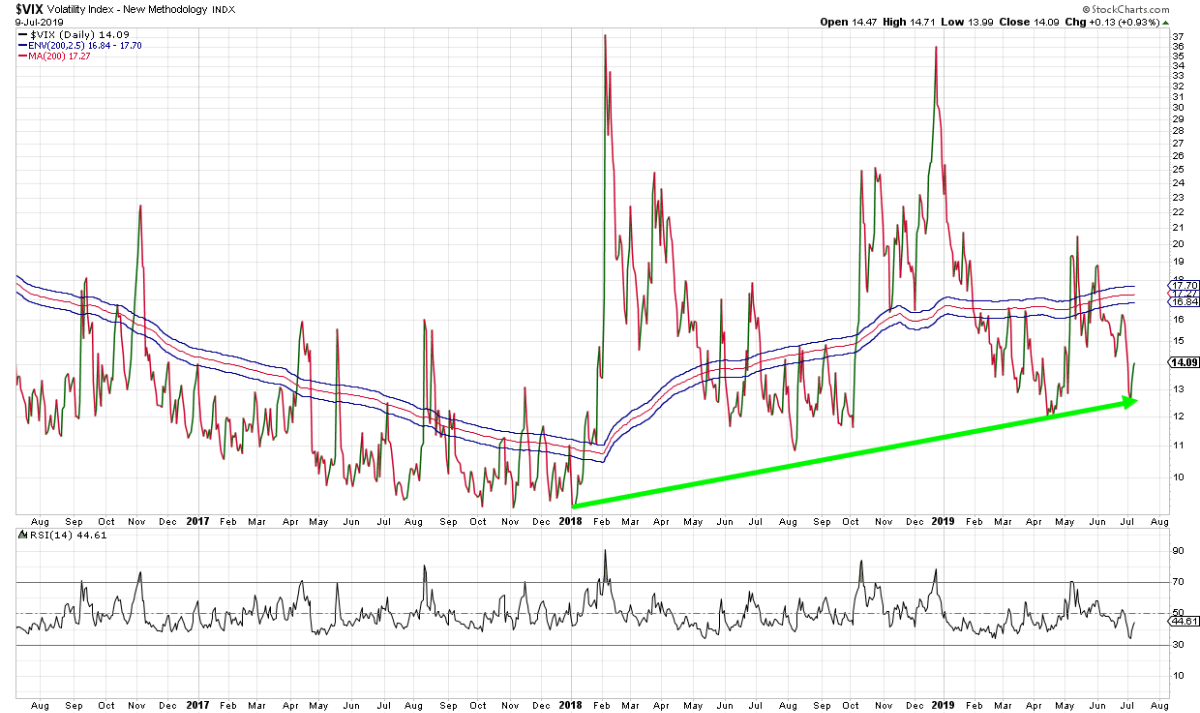

Volatility: The VIX was up almost a percent yesterday despite the stock market finishing higher. Volatility is making a higher low as the S&P 500 makes higher highs. This is another negative non-confirmation and divergence.

Telecom: The telecommunications sector was the strongest yesterday, finishing higher by over 1.85%. It remains in a negative trend however and has been in a wide trading range for several years.

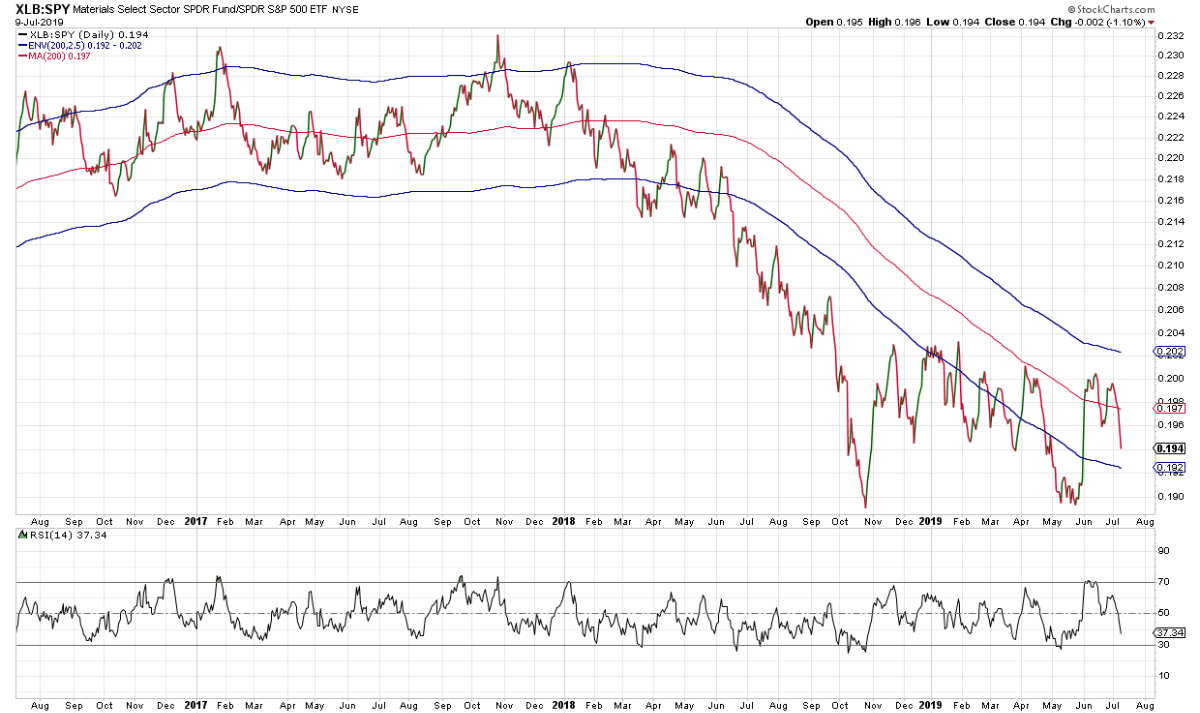

Materials: The materials sector was one of the weakest sectors yesterday. It has been in a negative trend relative to the S&P 500 since early 2018.

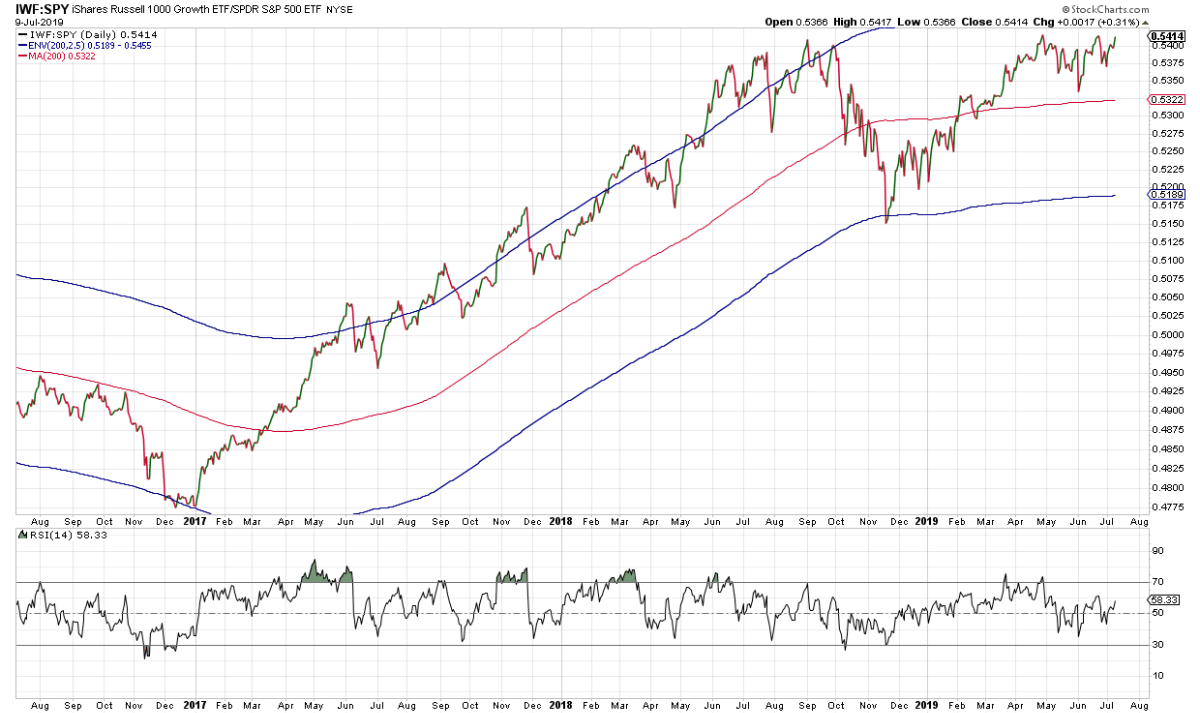

Growth: Growth was the strongest factor yesterday and has been one of the strongest factors over the last year. It is close to breaking out to new all-time highs relative to the S&P 500. It is in a strong positive trend on both a relative and absolute basis.

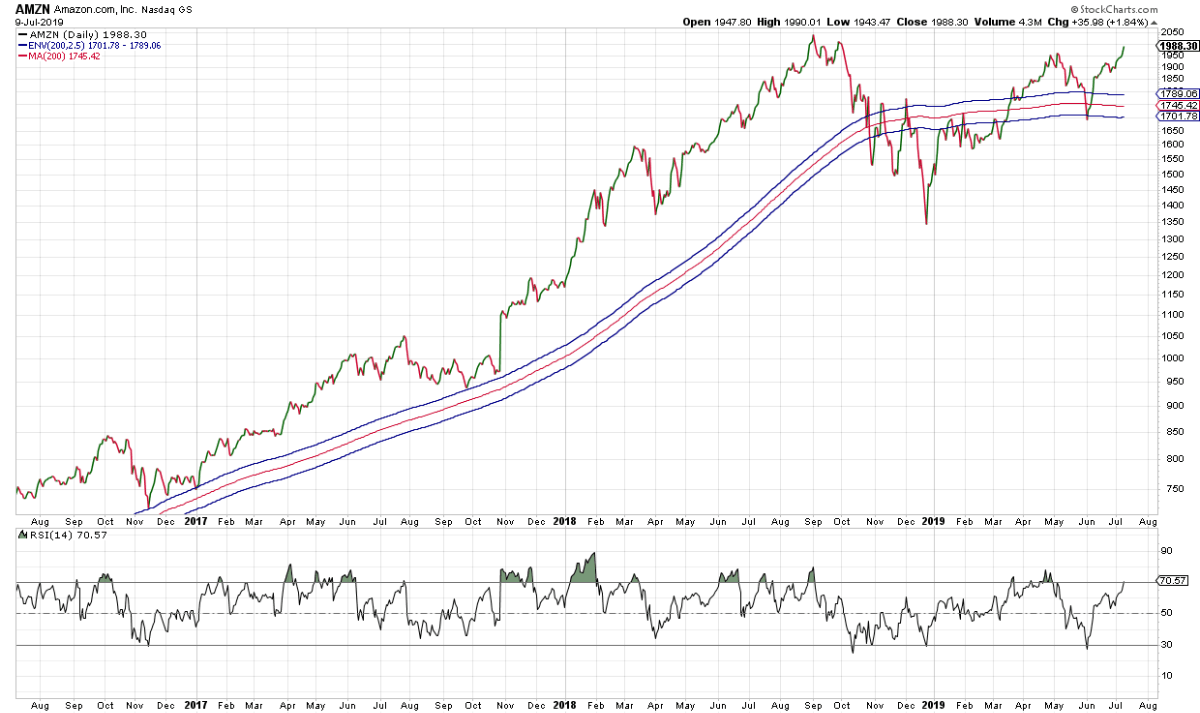

Amazon: Amazon is approaching all-time highs and is in a positive trend. It was the strongest performer in the S&P 500 yesterday. A breakout to new highs would be bullish for Amazon and the broader market.

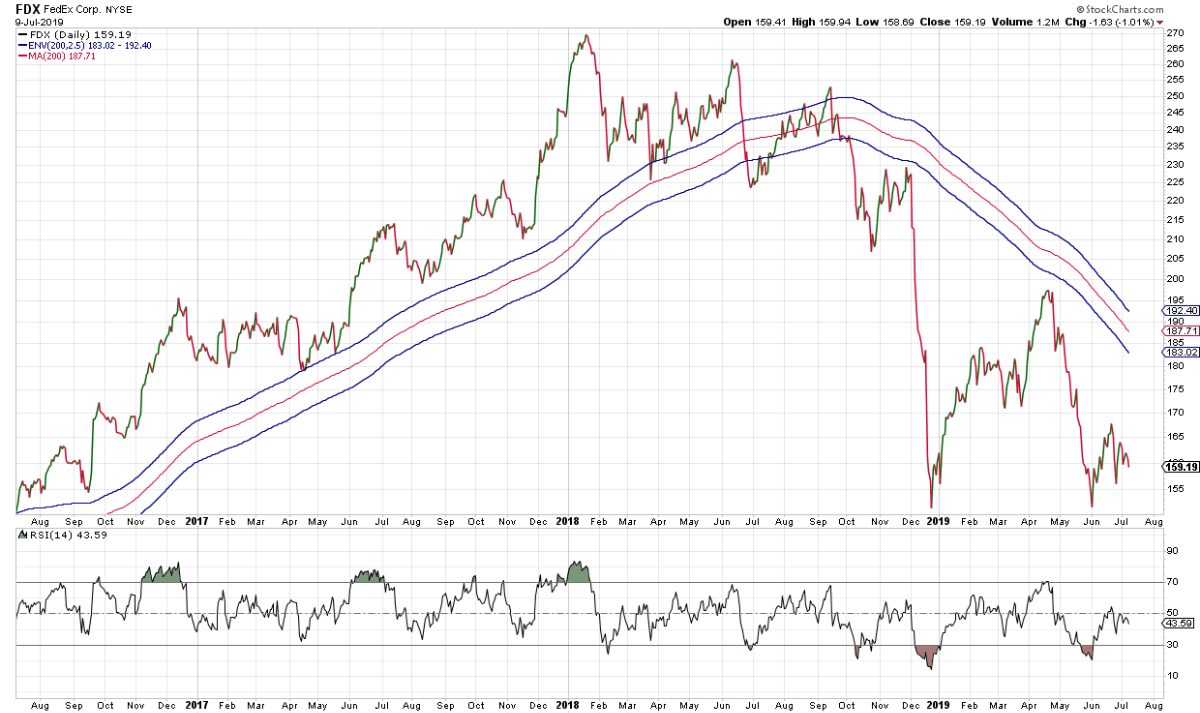

FedEx: The weakness in the Transportation sector has been a glaring negative divergence and negative non-confirmation for the broader stock market. FedEx has been in a strong negative trend and is near the lows it set in late 2018. Is FedEx a symptom of a rapidly slowing economy?

Futures Summary:

News from Bloomberg:

Jerome Powell testifies before Congress today and may leave interest rate cuts firmly on the table, even after the jobs report dialed down the urgency. Investors will also scour June meeting minutes for any sign that the central bank may pull back on policy easing. Traders are still pricing a full quarter-point reduction in July, but have scaled back views on how much easing will take place for all of 2019.

Donald Trump is concerned that the strengthening dollar is a threat to the economic boom he expects to carry him to a second term and requested aides to find ways to weaken it, people familiar said. He asked about the currency in job interviews with Fed picks Judy Shelton and Christopher Waller last week. But Larry Kudlow and Steven Mnuchin oppose intervening to weaken the dollar.

The census citizenship saga continued. A DOJ plea to assign a new legal team to challenge the lawsuit that blocked it from adding a citizenship question was rebuffed by a judge. The request was "patently deficient," the ruling said. The government provided "no reasons, let alone satisfactory reasons." Here's a QuickTake explaining the controversy.

Tesla told employees it's preparing to ramp up production at its Fremont plant after record deliveries in the second quarter. The email to staff from automotive president Jerome Guillen didn't give any specifics. Steps to build an assembly line in China—key to achieving 500,000 vehicle output this year—are also picking up pace, with many parts already in place, he said.

Treasury yields jumped, while U.S. stock futures slipped with European equities as doubts lingered about the pace of Fed policy easing. Oil rose and most industrial metals rallied. Gold slipped with the yen. The euro climbed on strong French economic data.

Author

Clint Sorenson, CFA, CMT

WealthShield