The S&P 500 dropped -0.17% yesterday

Highlights:

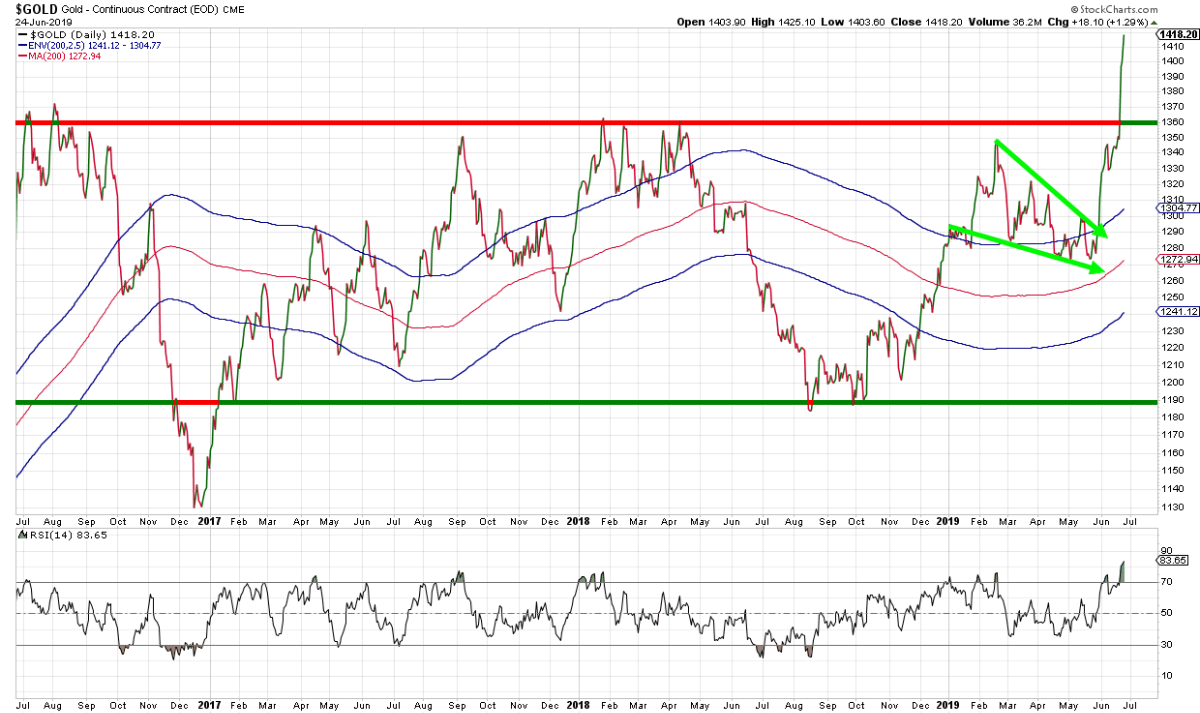

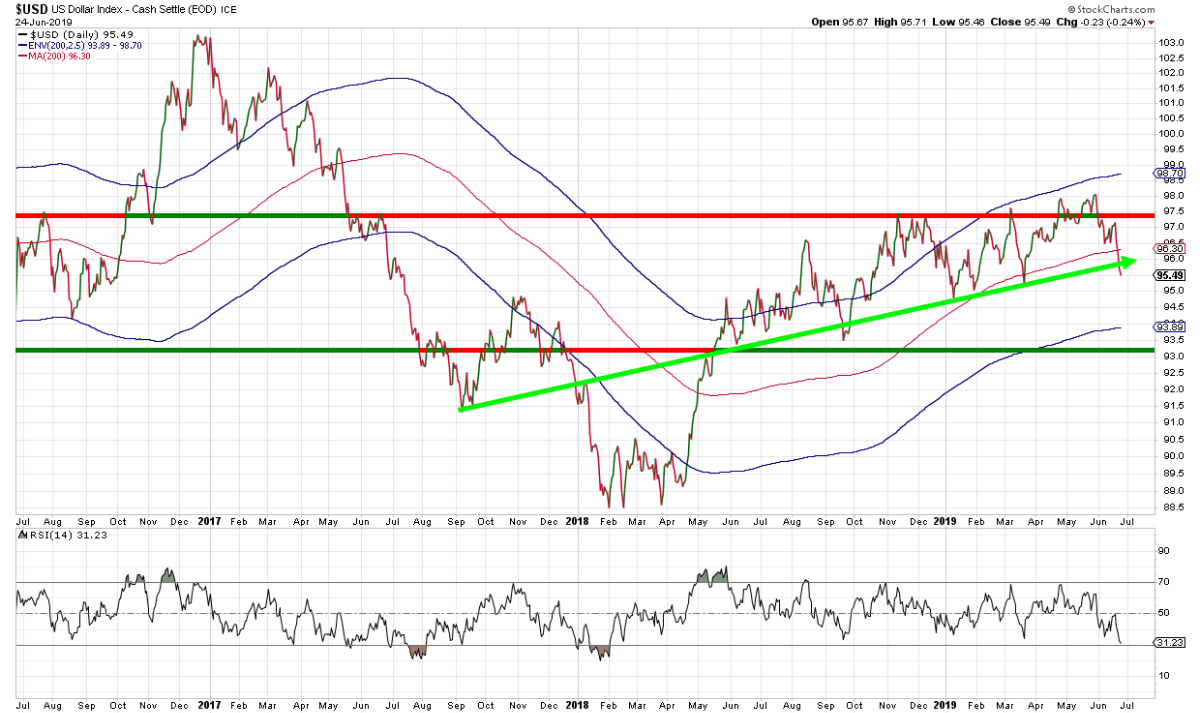

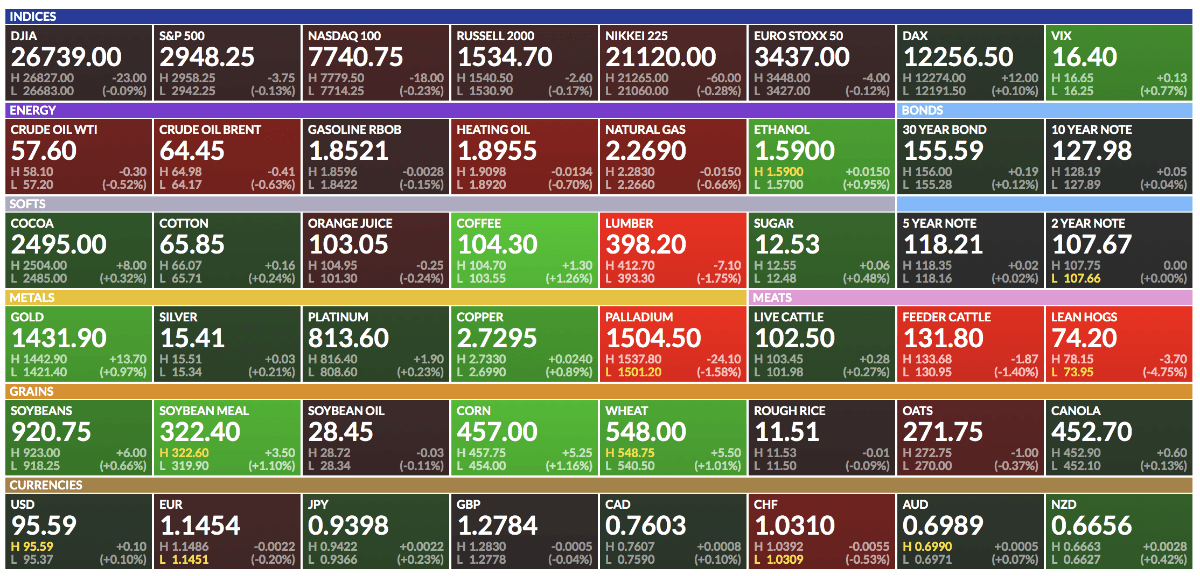

Market Recap: The S&P 500 dropped -0.17% yesterday. Gold surged, closing up 1.29%. The US dollar continued to break down, dropping another -0.24%. The benchmark 10-year yield dropped 5 basis points and bonds rallied.

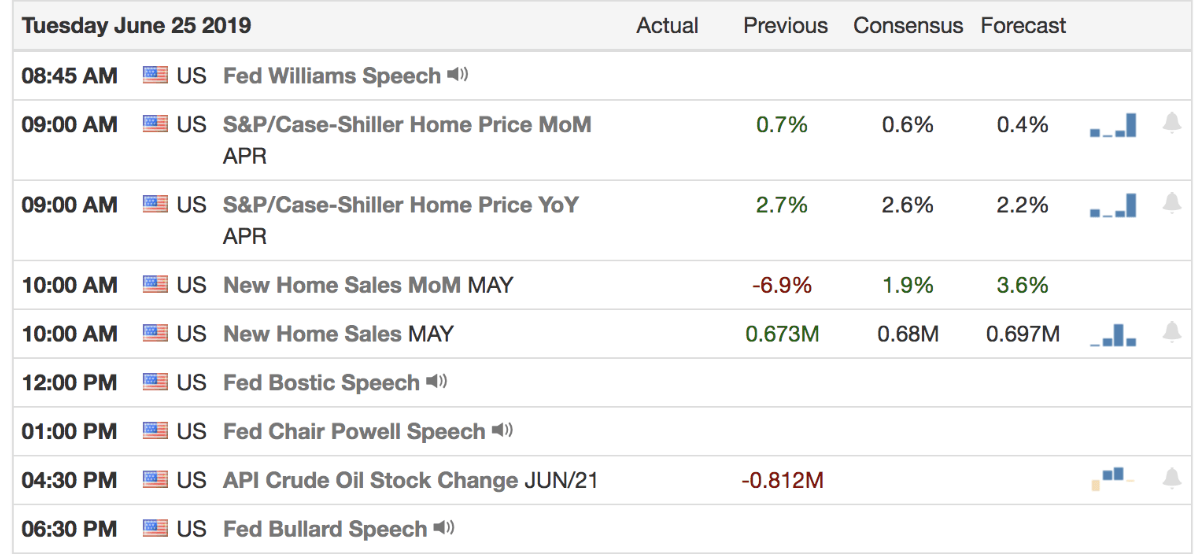

Economic Data: The Chicago Fed National Activity index disappointed yesterday, coming in at -0.05 versus consensus expectations of 0.10. The Dallas Fed Manufacturing Index dropped to -12.1 versus -1.0 expected and -5.3 previous. Today is a busy day on the economic calendar. The top items are housing related with the Case Shiller home price index, and new home sales.

Gold: Gold is continuing its breakout from last week. It is targeting over $1600 from a technical perspective. Gold is in a strong positive trend and has been helped recently by a dovish Federal Reserve and a weaker dollar.

U.S. Dollar: The U.S. Dollar broke below its 200-day moving average yesterday and major support. The dollar is close to oversold levels from a momentum perspective and remains in the 92-97 range that has governed price action for the better part of the last year.

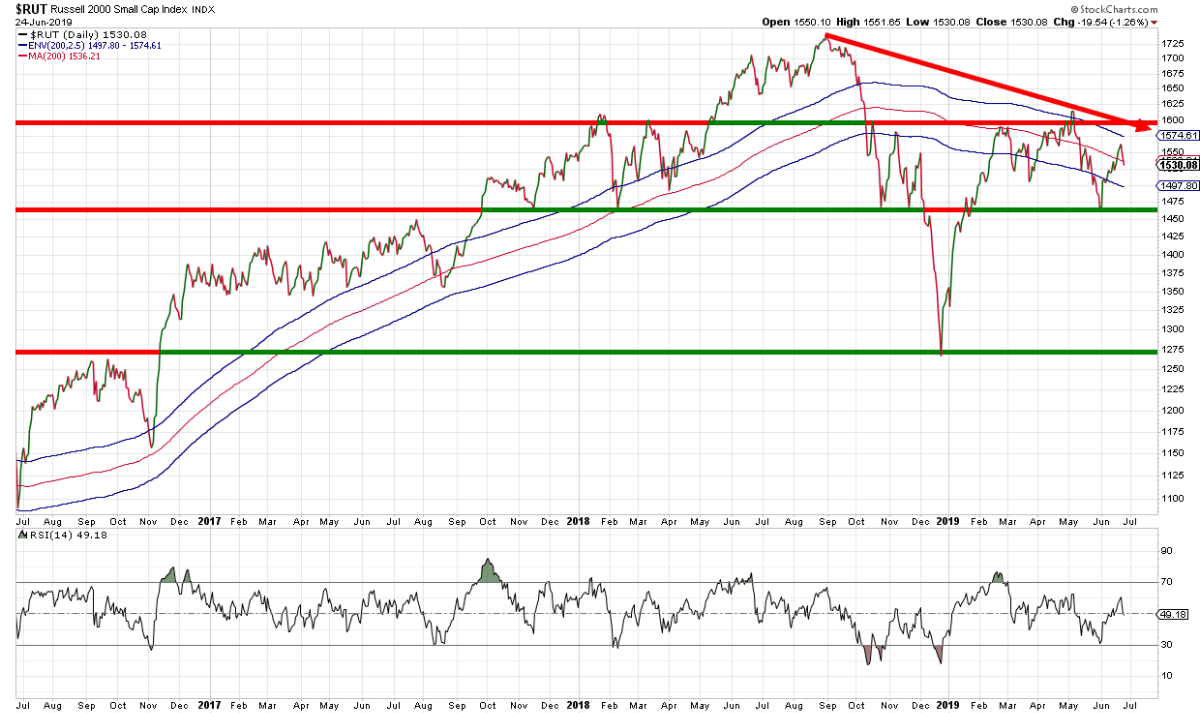

Russell 2000: The Russell 2000 stock market index is well below the 2018 highs and has yet to confirm the S&P 500 with a break-out to the upside. The Russell underperformed yesterday, dropping over -1%. The Russell 2000 remains in a negative trend and is a classic negative non-confirmation with the S&P 500.

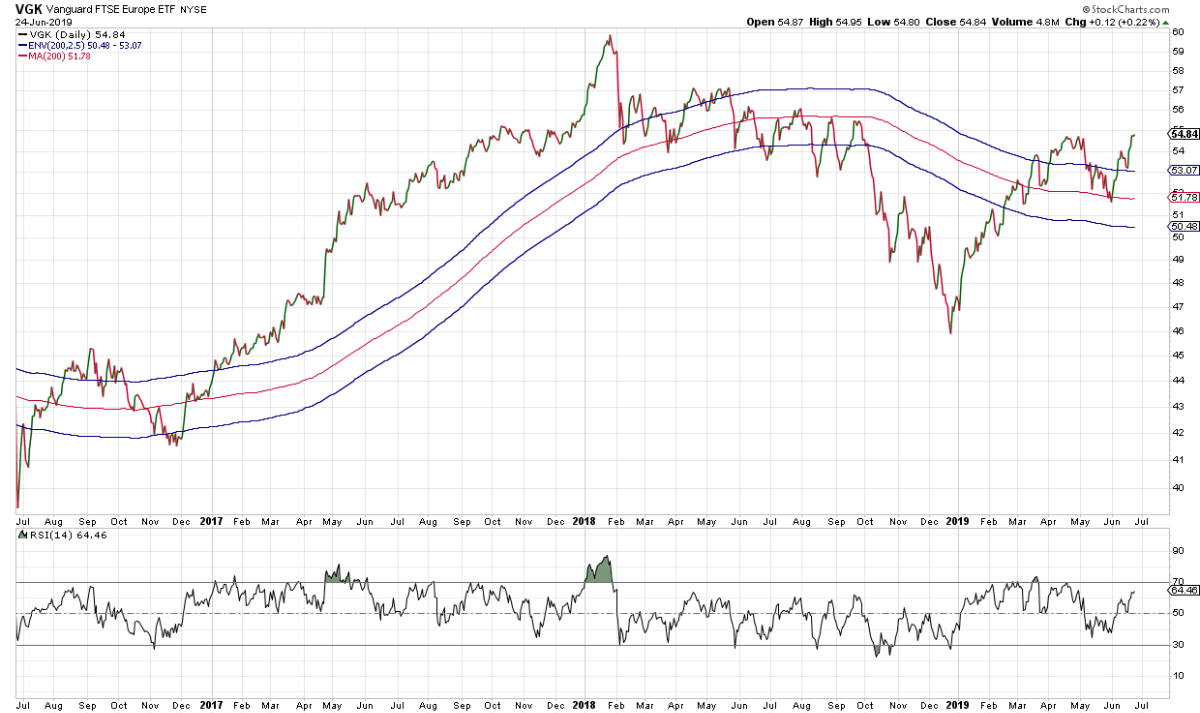

Europe: Europe (VGK) gained on the day yesterday, climbing 0.22%. It is close to breaking out to new highs for 2019. Will dovish comments from Draghi be enough to combat the weak economic activity? The Europe ETF is above its 200-day moving average, which it successfully tested as support several weeks back.

Futures Summary:

News from Bloomberg:

The path is closed. Iran said new sanctions against its supreme leader and other top officials mean there's no longer a path to a diplomatic solution with the U.S. President Trump put restrictions on Ayatollah Ali Khamenei and eight military chiefs that deny access to financial resources. Steven Mnuchin chimed in, saying financial sanctions will be imposed on Iran's foreign minister this week.

Trump has pondered withdrawing from a long-standing defense treaty with Japan, people familiar said. He thinks the accord is too one-sided because it promises U.S aid if Japan is ever attacked but doesn't oblige Japan to come to America's defense. Here's more about the treaty that forms the foundation of the postwar alliance between the countries.

U.S. officials downplayed expectations for the Trump-Xi Jinping meeting this week, insisting the president wasn't prepared to compromise on demands for meaningful Chinese economic reforms. They said he was focused on securing real structural change to address U.S. complaints about intellectual property theft and the widespread use of industrial subsidies, among other things.

Jerome Powell takes the stage today to speak on the economic outlook in New York. The Q&A session will probably be dominated by Trump's latest tirade. The chairman is "incorrect" to say he's entitled to a four-year term, Trump told The Hill. The Fed's John Williams, Raphael Bostic, Thomas Barkin and James Bullard also speak.

U.S. stock-index futures fell with European and Asian equities as investors sought havens. Chinese bank shares slid on concern the U.S. may sanction some lenders over North Korea. The yen and gold rallied, while the 10-year Treasury yield held at 2.01%. The dollar and oil were steady. Industrial metals were mostly higher.

Author

Clint Sorenson, CFA, CMT

WealthShield