The solution to the surge in US cases is obvious: Resume the lockdowns

Outlook:

We get producer prices today, ho hum. Canada reports jobs, likely a hefty recovery, and Mexico reports May industrial production, likely a recovery like just about everybody else.

Sentiment in the US, from the average Joe to Wall Street, is negative because of the unhappy realization that we need a renewed lockdown in order to get selective relief from lockdown later this summer if we have any hope of getting recovery in the fall. Recovery might be postponed from Q3 to Q4.

But when recovery expectations resume, even if delayed a few months, we can expect the same market exuberance we saw in May.

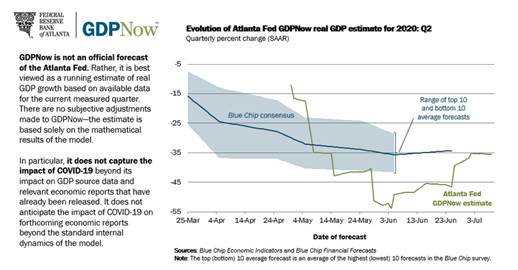

To recap: the bottom is in. See yesterday's chart from the Atlanta Fed, showing the most recent GDP forecast is for -35.5% in Q2, far less bad than over -45% only a few weeks ago. (We get another version next Thursday). You can just see the V-shape forming as the less-bad Atlanta forecast rises to match the Blue Chip consensus.

We may not be getting the full upward move to form a V-shaped recovery, but never forget: the market doesn't have a long-term orientation. The long-term is but a series of short-terms. Sometime soon, those now feeling risk averse will look around and see no alternatives for placing money—there's stock markets and commodities, and that's it. Nobody in his right mind aims to get tiny or negative returns.

Market participants don't have to believe any particular set of data to resume buying equities, and besides, some data is quite favorable. For the US market is slump over new Covid-19 cases on the same day that unemployment showed itself less-bad is inconsistent with its data-processing over the past few weeks. We can't find a compelling reason for March-level panic and/or gloom.

In other words, yesterday's equity index slump is an aberration. The drop in the 10-year yield to below the March level, when the S&P was tanking, is also an aberration. The equity index slide yesterday is nowhere big enough to justify that sizeable a drop in yields. It's disproportionate.

The dollar following along is likewise an aberration, especially in the context of growth. Here the reasoning gets a little tricky. On the whole, currencies track GDP over long periods of time. He who has more robust growth over the next guy gets an appreciating currency over the next guy's currency. This is due in part to inflation expectations running along in tandem with growth, and yields running along in tandem with inflation. That's assuming central banks do what we expect them to do, and it's hardly clear we have that condition today, especially after the Fed said, even before the pandemic, that it could safely allow a little overshooting.

Still, China, Japan and much of Europe are showing recovery in some critical sectors, especially industrial production and exports, that is going to be delayed in the US because of the surge in cases and new lockdowns. If we are looking at only the current quarter, that means a slower rate of growth in the US and thus the dollar should lose favor—unless there is a Shock or Crisis or Event (pick your poison), in which case the dollar becomes the safe-haven again.

But we don't have a Shock. We have a surge in US cases that was widely predicted by the scientists due to premature re-openings. The solution is equally obvious—resume the lockdowns. The market can easily digest this—it's simple. Having said that, it's not hard to imagine a genuine Shock, such as Trump refusing to leave office upon losing the November vote, calling it a rigged election and a hoax, his favorite new word. But that's the fourth quarter. Another source of a Shock can be the outrageous growth in collateralized loans, now bigger than the collateralized debt that brought misery in 2008-09. A financial market crisis would certainly qualify as a Shock. The Fed is acting as though everything is hunky-dory and its liquidity provisions worked, but there are bad undercurrents.

We may complain that the now-leading-edge stock market is flighty and inconsistent. It prefers the shiny new object over detail-laden reasoned argument. Finding order is always hard. Identifying aberrations is risky, and we may well be wrong about calling yesterday's outcomes aberrant. But here's one of our favorite quotes that we stick into every book the editor lets us use (from Bernard Baruch):

Have you ever seen, in some wood, on a sunny quiet day, a cloud of flying midges — thousands of them — hovering, apparently motionless, in a sunbeam? ... Yes? ... Well, did you ever see the whole flight — each mite apparently preserving its distance from all others — suddenly move, say three feet, to one side or the other? Well, what made them do that? A breeze? I said a quiet day. But try to recall — did you ever see them move directly back again in the same unison? Well, what made them do that? Great human mass movements are slower in inception but much more effective.

The developing anti-US and anti-dollar sentiment has hit a bump in the road, not a detour. Now if only we could untangle the safe-haven effect of the yen. If there is no need for a safe haven because recovery is okay, if delayed in the US, why would the yen be on the rise? This is a case where you follow the chart and forget what seems to be fundamental or mainstream sentiment. Judging from divergent currency outcomes on the same news, we don't have mainstream sentiment, anyway.

Tidbit: The US Supreme Court, waiting until the last day of the session, delivered two judgments of great importance. First is repetition of the principle that no man is above the law. This means the District Attorney of the State of New York can subpoena Trump's tax returns and financial statements in the course of a criminal investigation. The public won't get to see them until well after the election, but legal types find it interesting that the subpoena power is not restricted to the feds but extends to the states.

As for the three House committees getting the same information, the Court told them to go back and make a more refined and specific case for the legislative purpose, and take that to a lower court. This fails to acknowledge that the Ways and Means Committee is charged with the right to tax returns and the IRS "shall" turn them over. So the Supreme Court weaseled a bit on that one, but all the same, it's a Big Deal for the cherished rule of law so abused by Trump, and a big loss for Trump.

The big loss is mitigated by Trump pushing the rock down the hill until after the election, but it's not exactly a "victory" for him. The base was never going to drop him once they found out he's a fraud and a crook. They already knew that. They think cheating on taxes is "smart" and Trump is to be admired for gaming the system and sticking out the middle finger to the Establishment.

The other Supreme Court decision rules a big hunk of Oklahoma an Indian reservation, including a segment of Tulsa, a decision that is the most important for native Americans in decades and will re-shape a lot in that state, especially police and law enforcements matters, where native Americans have been persecuted. Social awareness and Indian rights are more in the public eye than in decades, including the right to shut down the oil pipeline on "stolen lands" and changing the names of sports teams.

Neither decision has anything directly to do with finance, but to the extent Trump has damaged the US' reputation, the Supreme Court shows the system still works. The rule of law over the rule of man is the basis of US exceptionalism. It's not gone, if a little soiled, and we go not have a king. And the Oklahoma decision shows, as Martin Luther King said, "Let us realize the arc of the moral universe is long, but it bends toward justice."

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat