The recession narrative

Inflation has been the dominant economic theme for months, but, under the influence of aggressive monetary tightening, one can expect this won’t last. At the same time, recession concerns are mounting. Central bankers acknowledge that their action may cause a technical recession, a huge majority of US CEO’s expect a recession and consensus forecasts show an increased recession risk in the US and even more so in the euro area. The recession narrative should lead to a wait-and-see attitude, of putting spending and hiring decisions on hold and creates a mutually reinforcing negative interaction between hard data and sentiment. A key condition for this to end is growing belief that central banks will have done their job and can afford to stop tightening. Whether reaching that point will really boost confidence will however depend on how the economy and the labour market have reacted to the rate increases.

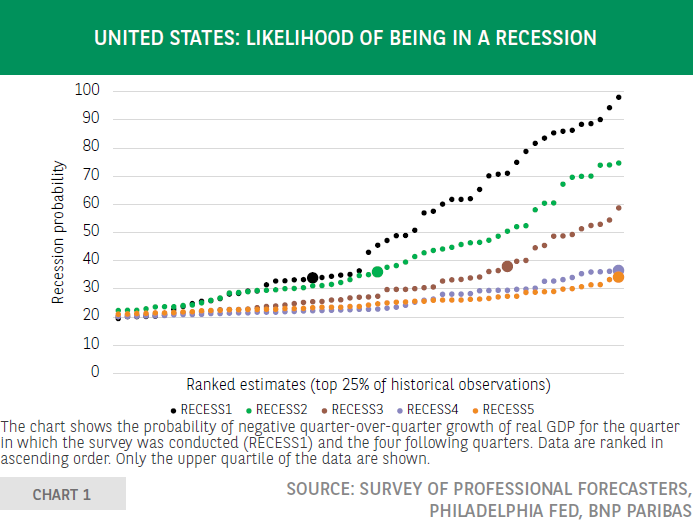

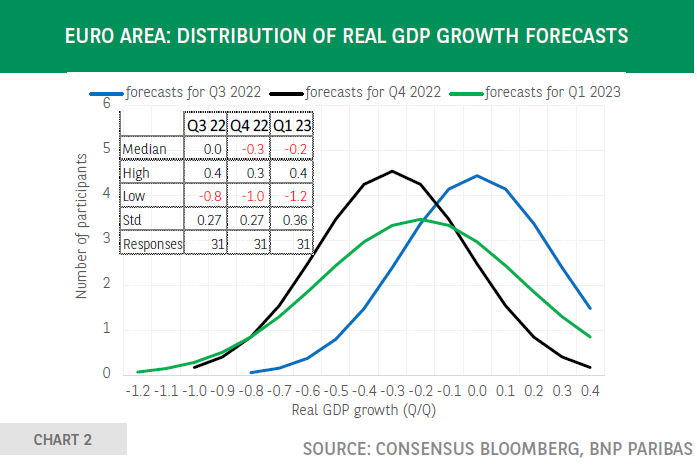

In the public debate about the economic situation, inflation has been the dominant theme for months, but one can expect this won’t last. Surveys show easing pressures in global supply chains and input prices, several commodity prices have declined recently and, although wage growth remains robust in the US and should accelerate further in the euro area, aggressive monetary tightening should be a key driver of gradual disinflation. In parallel, recession concerns have been increasing and, eventually, they will overtake inflation as the key topic of economic discussions. Federal Reserve Chair Jerome Powell has acknowledged that bringing inflation under control will cause some pain. According to a recent Conference Board survey, 81% of US CEOs are preparing for a recession over the next 12 to 18 months. They expect it to be brief, shallow and with limited global spillovers. 12% are gloomier and expect a deep recession with material global spillovers, whereas only 7% do not anticipate a recession. Growth forecasts have been revised downwards, although the Survey of Professional Forecasters conducted by the Federal Reserve of Philadelphia still expects positive quarterly growth in the US over the entire forecast horizon, which runs until Q3 2023. However, the assessment of the recession likelihood has increased significantly for the short run and is at a record high for the medium run (four or five quarters ahead, which corresponds to Q2 and Q3 2023) (chart 1). In the euro area, the Bloomberg consensus expects negative growth in the final quarter of this year and the first quarter of next year (chart 2). ECB chief economist Philip Lane, referring to the rate hikes, has recently stated that “we’re not going to pretend this is pain free”, adding that a technical recession cannot be ruled out.

The reasons behind the downward shift in the growth outlook are well-known. Inflation is eroding households’ purchasing power and corporate profit margins. In Europe, more and more firms are temporarily stopping production in reaction to high gas and electricity prices. Central bank rate hikes, as well as the anticipation of further rate increases, have raised the cost of borrowing, which is weighing on demand, especially in the housing sector in the US. Although the order books in the manufacturing sector are still well-filled, the trend of incoming orders is down, even more so with respect to new export orders. Subdued growth in China is playing an important role in this respect. Finally, the war in Ukraine has been an important factor, to a large degree through its impact on commodity prices.

The recession narrative makes people doubt and worry. Not only will they scale back their base case scenario of income, sales, profits, but their conviction level about the forecasts will also decline. Firms will increasingly adopt a wait-and-see attitude until a clearer picture emerges. Investment plans will be put on hold. Hiring intentions will be scaled back -this is already visible in EU survey data-, which eventually should give rise to increasing unemployment expectations of households. This in turn should weigh on consumer spending. At some point, this mutually reinforcing negative interaction between hard data -activity, demand, etc.- and soft data -confidence-, should stop.

A key condition is growing belief that central banks will have done their job and can afford to stop tightening. It implies that rate hikes, despite their aggressiveness, have a silver lining: the cyclical peak in the policy rate will come sooner than under a gradualist approach. Whether reaching that point will really boost confidence will however depend on how the economy and the labour market have reacted to the rate increases.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.