The probability of the June hike is solid

Outlook:

The market expected a payrolls boost of about 180,000-185,000 but got only 138,000, made to appear worse by the silly ADP forecast of 253,000 for the private sector alone. No-body much cares if the unemployment rate ticked down to 4.3% from 4.4%--we all know it's not truly representative.

The probability of the June hike is solid—95.8% this morning vs. 91.2 on Friday, according to the CME FedWatch tool. Oddly, the Sept probability is a tad higher at 27.2% from 27.0 on Friday. We thought the low payrolls number would fire up talk of no hike in September. But the 10-year yield remains soft at 2.179% (from 2.110% on Friday morning). We don't have a lot of US data this week so we expect the near-term focus to remain on the yield divergence.

Meanwhile, the economic picture is a glass half-full. The Atlanta Fed revised its Q2 GDP estimate on Friday to 3.4% from 4% on June 1, based on a drop in expected real consumer spending from 3.6% to 3.1%, in turn based on the employment report. See the chart. We get the next forecast on Friday.

But regardless of where GDP is going, the dollar has serious underlying support from the Fed hike in two weeks as practically a fact while the ECB standing pat on Thursday is very nearly a certainty, too. Mr. Draghi says the eurozone still needs support and inflation has not proved itself sustainable. The BBK's Weidmann and a few others want to talk about tapering. This could help the euro a little but let's be realistic—talk about talk is not the same thing as action. We need to expect the euro to jiggle around but almost certainly to test support around 1.1207 today. A dip to the previous low (1.1107) would be catastrophic, ruining the usual pattern and forcing everything to draw new lines all over the place. Not everyone sees the US and the dollar as beating Europe and the euro. As the FT notes, the Trump boost is pretty feeble so far and "the economic story of 2017 has been the euphoric eurozone. Econom-ic growth in the single currency area was more than twice as fast in the first quarter of 2017 than in the US, raising the question whether its recovery is just a pleasant blip or whether it is more deeply rooted and self-sustaining. The answer is of more than academic interest. If the European Central Bank be-lieves the eurozone economy to be set fair, it can start to think about withdrawing the exceptional stim-ulus measures at its meeting in Estonia this week."

The Market composite PMI for Germany is at a 6-year high with some of the usual laggards (Spain, Italy, Portugal) not doing badly at all. Still, the majority see the ECB erring on the side of caution and not repeating the mistake of 2009 with a stupid and wildly premature rate hike. And is it true that Euro-pean political uncertainties are now behind us? But hopes springs eternal. While experts say the €60 billion/month program will remain in place until year-end, there's the official "outlook" to consider. A significant improvement in the official outlook on Thursday could go a long way to supporting the "talk about talk" story and provide support to the euro.

There will be tears.

And that's just from the usual stuff, especially divergent central bank policies. Off on the side, the Qa-tar isolation is a pretty big deal. Qatar has been making nice with Iran while the US has its Middle East military central command post there, not to mention a sovereign wealth fund of about $335 billion in-vested all through the US, UK and European economies. And on Thursday we get two big political events, the Comey testimony to Congress and the UK election, on top of the ECB meeting and Draghi press conference. Everyone will want to crawl into a cave on Thursday.

A key point of interest in the UK election is the erratic behavior of the voters, who already punched the world in the nose last year with Brexit and might well do it again with Labour. The best pollster on the planet, Nate Silver, points out that if the polls are wrong again, the Tories could lose their majority, setting the cat among the pigeons. Over the weekend, Silver published the chart below—the Tory lead averages only 7 points.

Silver is nothing if not brutally honest. "So to borrow our phrasing from the U.S. election, when we said that Donald Trump was only a ‘normal-sized polling error' away from winning the Electoral Col-lege, May's Conservatives are now only a normal-sized polling error away from a hung parliament. On average in the U.K., the final polling average has missed the actual Conservative-Labour margin by about 4 percentage points. (This is twice the average error in U.S. presidential elections.) If Labour out-performs its polls by that margin, Conservatives would win the popular vote by only about 3 points — and May would probably have to find a coalition partner to form the next government. If the polls were to miss by any more than that in Labour's favor, a variety of yet-more-unpleasant scenarios could crop up for May, including some where Labour leader Jeremy Corbyn tried to form a government instead."

Silver goes on to say the Conservatives usual outperform their polls going back decades, But we need to watch out for conventional wisdom, which gives rise to the "First Rule of Polling Errors, which is that polls almost always miss in the opposite direction of what pundits expect."

Let's say all the worst-case outcomes are what we get. The beneficiary is the dollar, despite it's Trump-size millstone around its neck and an equally heavy and recalcitrant bond market.

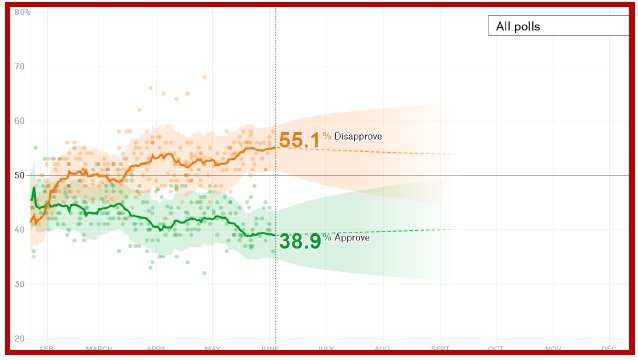

Political Tidbit: While we were surfing around in Silver's 538 site, we can across this poll summary on Trump's approval ratings. It's hardly a surprise that disapproval of Trump is rising, but what we really want to know is how Trump will respond to it. A narcissist hates to be embarrassed in public and we already saw Trump's fixation on crowd size and denying that he lost the popular vote. So what initi-ative will Trump take to get favorable news headlines? Health care and tax reform are probably ex-hausted for the moment. He has been outfoxed by China. With Comey testifying on Thursday, Trump needs a giant new distraction. Be afraid.

Note to Readers: RTS has launched a Trade Copier service. We place our trades from the Afternoon Traders' Advisory in the retail spot market and your MT4 account mirrors the trades taken in the RTS account. You don't have to lift a finger. You get to pick how much leverage and exactly which curren-cies you want to include.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 110.51 | SHORT USD | 05/18/17 | WEAK | 110.36 | -0.14% |

| GBP/USD | 1.2910 | SHORT GBP | 05/30/17 | STRONG | 1.2860 | -0.39% |

| EUR/USD | 1.1264 | LONG EURO | 04/13/17 | STRONG | 1.0643 | 5.83% |

| EUR/JPY | 124.48 | LONG EURO | 04/25/17 | STRONG | 120.15 | 3.60% |

| EUR/GBP | 0.8724 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 2.76% |

| USD/CHF | 0.9637 | SHORT USD | 04/13/17 | STRONG | 1.0043 | 4.04% |

| USD/CAD | 1.3461 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 1.17% |

| NZD/USD | 0.7139 | LONG NZD | 05/30/17 | STRONG | 0.7062 | 1.09% |

| AUD/USD | 0.7479 | SHORT AUD | 06/02/17 | WEAK | 0.7395 | -1.14% |

| AUD/JPY | 82.65 | SHORT AUD | 06/01/17 | WEAK | 82.19 | -0.56% |

| USD/MXN | 18.4032 | SHORT USD | 05/17/17 | STRONG | 18.7098 | 1.64% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat