The market on a sugar high

Outlook:

Today we get the US inflation data, likely to show a measly 0.1% gain in Jan (after -0.1% in Dec on the drop in energy prices, mostly gasoline) for a year-over-year of 1.5%. It was 1.9% in December…. implying that the data-dependent Fed can sit back and allow markets to continue to believe no hikes anytime soon. What about core inflation? It was 0.2% m/m in Dec for 2.1% y/y. Nothing to see here.

But just as we cannot trust the JOLTs report—fewer than one worker per job opening!—we don’t trust the inflation data, either. Again, we are not suggesting anything nefarious at the BLS. We have all complained about the way the data basket is put together, not to mention quality adjustments and other fiddlings. Of interest lately is the BLS sending its price-takers only to brick and mortar stores—no internet shopping at the BLS.

The important point is that the hypothetical household for which the BLS is measuring does not exist. We really have to stop considering the official CPI or core CPI as having much to do with actual behavior and real prices. The Fed already knows this, although its preferred measure is hardly any more accurate or representative. Data-dependence, my foot. Before we can hitch our wagon to that star, we should have some realistic data in the first place. Ranting about lousy data serves little purpose other than to warn us to be skeptical about market responses to what is really fake news. Assuming we get the low number expected, markets will rush to judgment that the Fed is on hold for at least one quarter and probably two, which may be true but not because inflation is nowhere to be found. The Fed doesn’t know any better than the rest of us what the level of inflation really is, or where it’s headed.

We call this stockbroker economics and most of the time, it suffices to contribute to a decent forecast. But periodically we get grouchy about bad data. It must be skewing our understanding of the state of the economy. It’s also a dangerous place to start when considering changes likely or sure to come, like oil prices and tariff effects. Bottom line, let’s not be too accepting of information known upfront to be false. We are, of course, going to forget all about CPI by Friday, when we get the delayed retail sales for December, almost certain to be excellent.

We smell a market on a sugar high. The S&P closed over the 200-day moving average. We have a complacent/compliant Fed. Trade war with China can be partly resolved and partly delayed. We’re not getting a second government shut-down. Corporate earnings are still pretty good and earnings season is almost over. There are no roadblocks to perfect harmony and endless market gains. Well, that’s exactly the problem. When you don’t know who is the sucker at the poker table, it’s you.

In other words, various markets overreacted last December to the doom/gloom outlook that included global recession, Brexit and Trump trainwrecks, chiefly tariffs. Now that the stock market drop scared Trump into a more reasonable stance, we are overreacting in the opposite direction. But he is still an erratic jackass and we still have genuinely scary conditions in the eurozone, if not in the US just yet.

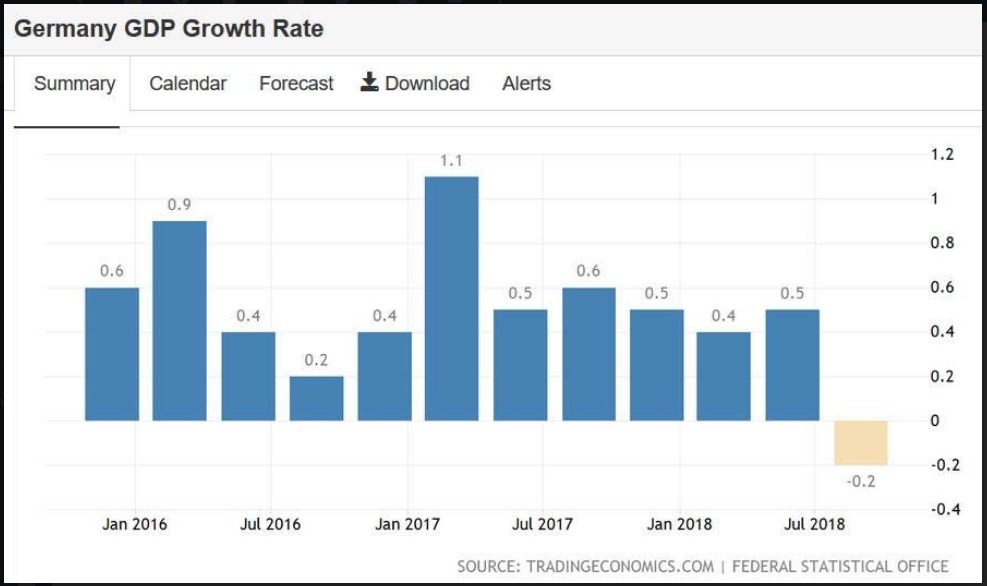

That makes tomorrow’s Q4 GDP from Germany more important than ever. The forecast is for a 0.1% rise after -0.2% in Q3—avoiding a technical recession by the skin of its teeth. A Bloomberg opinion piece has it that normalization should work in both directions, i.e., Germany should engage in fiscal stimulus. “The country's fiscal surplus is way out of whack, at almost 2 percent of GDP for 2018. Meanwhile, nominal yields on German bunds are near zero, and recession risk is rising, both domestically and across the euro area. So the bond market is offering Germany essentially free money, at a time of huge surpluses and persistently sluggish growth. It definitely sounds like there's a strong case for normalization.”

We wish we had a dollar for every occasion when somebody proposes Germany should do something about its giant trade and current account surplus, and/or diehard zero deficit stance. It has been going on for decades and Germany never budges. We can hardly expect a change now. We can’t expect a change even if Trump goes forward with a tariff on German luxury cars.

The Commerce Dept “investigation” report is due next Monday, and then Trump has three months to decide whether to impose tariffs on national security grounds. This is nonsense, of course; Trump just doesn’t like all those Mercedes and BMW’s on Fifth Avenue, which he somehow thinks he owns. The Commerce Dept is doing the investigation but no one has any doubt that the decision will be based on the mood of the moment and most of Trump’s moments are full of dissatisfaction. A 25% tariff on German cars would be a heavy blow to the German auto industry and likely a big euro-negative. The smart action would be to launch a public relations campaign on TV in the US—re-run those cute VW ads from the 1960’s or something, and then lobby Congress shamelessly. Trump could be stopped by public opinion and by Congress carving out the German auto industry as specifically not a national security issue. It would cost quite a lot but so will the loss of the US market.

In addition to the German car story, the WSJ reports the new Nafta isn’t actually in the bag. It is “threatened by a sharp divide between congressional Democrats and the Trump administration. Democrats want changes to ensure Mexico allows its workers to form unions freely and enforces environmental protections.”

Trump may have to give up the China trade war to prevent another stock market meltdown but he just loves to pick trade fights. So far we have identified three—German cars, Nafta and OPEC (see below). A sugar -high on everything going swimmingly is not justified given the nature of the Orange Menace. The implication is clear—the dollar can retreat a little more on the seemingly good news and drop in fear, but more fear lies right around the next corner.

Tidbit: We continue to think, without decent evidence but a fair amount of logic, that the price of oil feeds inflation in all kinds of hidden ways and more importantly, feeds inflation expectations. Now we have the Saudis trying to re-assert dominance—nay, control—over oil pricing. This takes the form of bullying OPEC and also Russia, and now investing in global oil and gas exploration and production everywhere in the world. Saudi oil minister Falih told the FT that the world will be Saudi Aramco’s playground and Aramco will become a top international player like Royal Dutch Shell or ExxonMobil. This is hardly weaning Saudi Arabia away from its addiction to oil, as the Crown Prince said last year, but rather doubling down. The clever FT reporter writes “Crude is now hovering near $60 a barrel, while Saudi Arabia’s budget requires levels closer to $80.”

As noted above, Mr Falih said output will be cut in March. The new Aramco investments will focus on gas, where demand is rising faster than in oil. “Saudi Arabia has eyed investments in Russia’s liquefied natural gas sector and is in talks about taking a stake in export facilities in the US. But Mr Falih also mentioned Australia as a possible investment destination.”

Falih said “We can stand shoulder to shoulder with anyone and outdo them.” Really? It couldn’t even manage a stock offering. The Saudis pretended the IPO failed because they didn’t want to disclose private data, but the world suspects maybe the data is not so hot. Whatever the reason, the market showed a distinct lack of demand. The Saudis find it hard to believe the rest of the world doesn’t find the country a desirable investment location. And the US is throwing up a roadblock that seems pretty silly at first but could turn into something serious—the lawsuit against OPEC for price manipulation, under consideration in Congress right now. Golly, maybe this is the next disruptive fight Trump is starting. Saudi Arabia has all but announced it is the new bully on the world stage. Current bully Trump won’t like that.

If there is going to be major federal lawsuit against anybody, it should be against Big Pharma and its outrageously predatory drug prices. So far we have only one of the many Democratic party presidential hopefuls putting Big Pharma in the crosshairs—the sensible and effective Amy Klobuchar. But we bet it’s going to become a major platform issue by all of them before long.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat