The main point we should take away is that the economy is nowhere close to stagnation or recession

Outlook: Payrolls were 428,000 and the unemployment rate, 3.6%. This nearly matches the original March print of 431,000 and beats most forecasts.

Some folks are still struggling to disambiguate the Fed’s comments, or rather Mr. Powell’s. Fed-watcher Ip at the WSJ has a spot-on summary: “Employment is the best contemporaneous indicator of the business cycle and it shows no sign of a slowdown. Indeed, job growth remains well above its long-run sustainable pace, suggesting the labor market is not just tight, but too tight.

“Moreover, recent gains in labor supply evaporated as the labor-force participation rate ticked down to 62.2% from 62.4%, although for people aged 25 to 54, it only edged down to 82.4% from 82.5%, not far from its pre-pandemic level.” The Journal is kind enough to note in the chart footnote that 2022 data is not really comparable with earlier data.

But in the end, the main point we should take away is that the economy is nowhere close to stagnation or recession, if we consider the jobs data has predictive value.

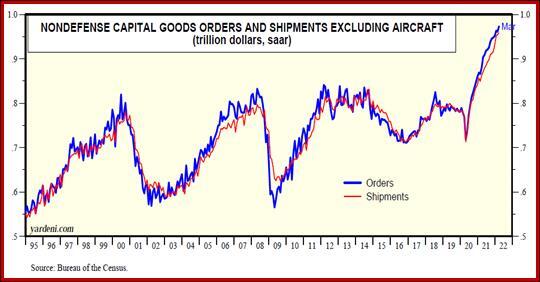

We suspect jobs and employment data to be inaccurate, to be polite, and while heed it we must, we like capital investment better. Broadly, capital investment can encompass consumer durables and things like housing and autos, while business capital spending is proxy for futures GDP. Last week the Atlanta Fed GDPNow forecast for Q2 was raised from 1.6% to 2.2% on the rise in auto sales that contributed to real personal consumption expenditures growth from 3.6% to 4.4%. We get another forecast today.

As for business capital spending, Capex itself is down a little, although annual rates after a pandemic shutdown are not the best data. The charts are from the Yardeni package and, as always, intriguing. Nondefense capital goods ex-aircraft and business owner expansion plans are definitely encouraging and suggest Q2 GDP will NOT be another negative and thus, technically a recession.

As for the equity markets, it’s not clear that the bubble has burst. It may be leaking, but we can’t say it has burst. The doom-and-gloom crowd are out in force, which contributes to additional losses, but the cycle gang thinks there is a chance the bottom is near. One reason equities can come back is that after a global fall of about 15%, traders will realize that cash and bonds are still delivering a low rate of return and it’s negative in real terms, while equities have the potential to deliver meaningful real return. It’s the highly speculative high0tech sector that is suffering the most and leading the pack down, but some companies are getting excellent growth (like the oil companies Buffett bought last week).

The wall of worry today includes China’s zero-Covid policy and lockdowns, crippled supply chains, high inflation, the Russian invasion of Ukraine and appalling conduct there, and the risk of slowing growth everywhere with recession in some places (like Europe). From a purely risk sentiment perspective, the dollar still wins hands down.

Strangely, the risk this week is that US inflation starts to abate. We get wholesale sales and inventories today, with accompanying price data, and CPI on Wednesday. According to Trading Economics, the consensus forecast for CPI is 8.1% from 8.5% in March, with its own forecast at 8.2%. Is the top in or almost in? A drop in US inflation and/or inflation expectations is not necessarily anti-dollar, but it might cause some reconfiguration.

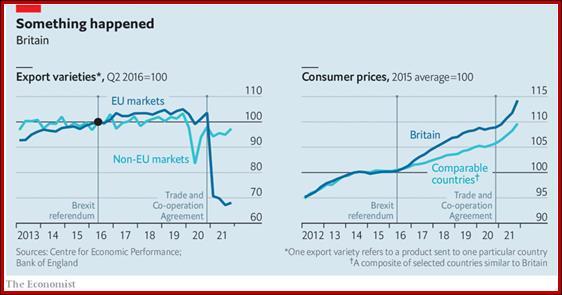

Tidbit: In a section titled “Left Behind,” The Economist decries the loss of exports by small businesses. See the chart. We already knew Brexit would harm the UK economy and we are getting some serious data to measure it. This double chart show the UK is also getting more inflation, in part because of tariffs.

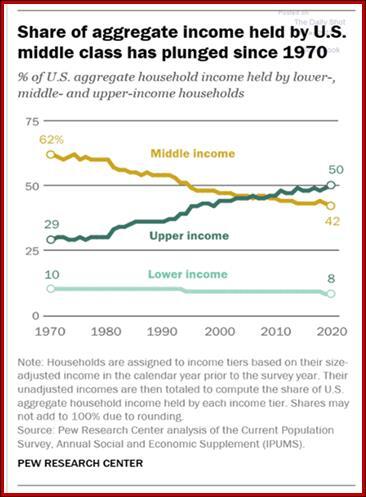

Tidbit: You don’t have to be a screaming pinko to have some concern for income inequality, which can have lasting effects on trends in consumer spending, housing, indebtedness, and more. Here is a chart from the respected Pew Research Center. Notice the crossover around the same time as the 2007-08 financial crisis. The article points out that who did the best over the past 50 years are Asians and white men, and anyone with a college degree.

Studies like this make you wish you knew more that demographics. As we see in Japan, with a near total ban on immigration and a contracting and ageing population, demographics can have a huge effect on the economy and financial markets.

Tidbit: On Friday, Euronews had a spendid video of Sweden building up its island of Gotland, which is halfway to Russia in the Baltic Sea. It has been repeatedly invaded by everybody since the early Middle Ages–Denmark, Russia–but has been disarmed since WW II. Now the Swedes are arming it again as they also contemplate joining Nato. Neighbor Norway is a member. One issue is that joining or thinking about joining could trigger an attack by Russia, as in Ukraine. Never mind that Nato is a defensive organization, not an offensive one. The video is enjoyable as much for the presentation of the Swedes as the geopolitical content–"sanity and common sense personified (the opposite of what we get in the US).

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat