The low volatility factor resumed its winning ways yesterday

Highlights:

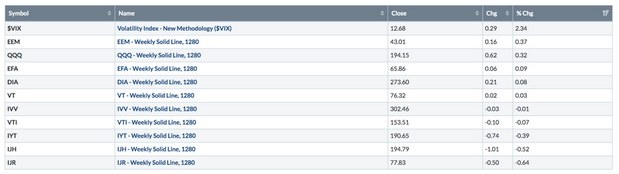

Market Recap: Emerging markets were the top performing broad market, up 0.37% on the day. Small caps were the biggest laggards, finishing down -0.64% on the day. The S&P 500 finished flat on the day.

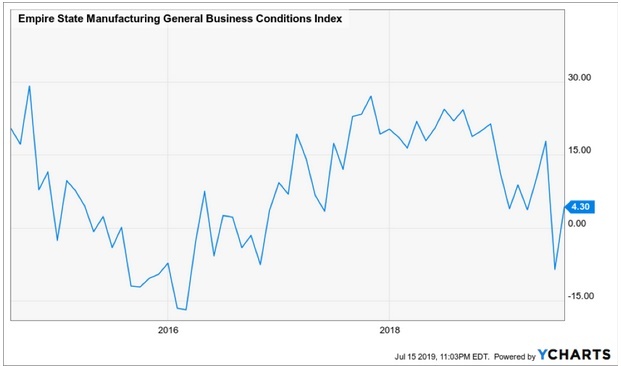

Economic Activity: The NY Empire State Manufacturing General Business Conditions Index came in higher than expected at 4.30. Expectations were for a reading of 2.

Volatility: The VIX closed higher by over 2% on the day. The VIX is making a series of higher lows as the broad stock market makes higher highs.

Low Volatility: The low volatility factor resumed its winning ways yesterday. It was the strongest performer, closing higher by over 0.23%. It remains in a positive trend and continues to hit new highs.

Momentum: Momentum also remains in a strong positive trend, closing higher yesterday by over 0.21%. It is encouraging for further upside in the markets, that the market continues to break to new highs.

Semiconductors: The Semiconductor sector was higher yesterday and is close to breaking to new highs. Semiconductors being at or near all time highs is conducive to further market upside.

Lumber: Lumber continued its decline yesterday, dropping over -3%. Lumber is signaling a heightened level of market risk. With markets approaching overbought levels, could volatility be on the horizon?

Philippines: The Philippines ETF rallied over 2% yesterday and remains in a positive trend. Momentum continues to strengthen, suggesting that at least a re-test of 2018 highs may be in the cards.

Emerging Markets: Emerging markets are back in a positive trend relative to international developed markets. Could a reflation trade be underway?

Futures Summary:

News from Bloomberg:

The bank earnings continue to roll in. Citi's equity trading miss lowers the bar for JPMorgan, and maybe even more so for Goldman, given its client mix, Bloomberg Intelligence said. They'll probably also get one-time pops from investments in Tradeweb. For Wells Fargo, the CEO issue lingers. There's potential for mortgage banking revenue to offset interest margin pressure, BI said.

The war of words between President Trump and the Democrats' so-called Squad continued. Alexandria Ocasio-Cortez, Ayanna Pressley, Ilhan Omar and Rashida Tlaib said his verbal attacks won't distract them from issues including immigration, health care, gun violence and drug prices. But Trump tweeted the Democrats have been "forced to embrace them. That means they are endorsing Socialism."

Google, Amazon, Facebook and Apple face a grilling by the House antitrust panel today. A key question is whether major tech companies can raise barriers to new entrants, strangling competition and innovation. It may be the biggest showdown between Silicon Valley and D.C. since Bill Gates faced questions about a potential monopoly in 1998. Here's a look at whether Big Tech is too big.

Amazon Prime Day update: Shoppers are snatching up potato chips and toilet paper, not just Echos. Sales of consumable products in the first nine hours were about triple the typical day, CommerceIQ said, showing its appeal stretches beyond big-ticket items. Shoppers will spend $5.8 billion over the two-day event, Coresight estimated. Prime Day is also providing package thieves with more opportunities.

Stocks and bonds struggled for direction before earnings and Fed talk. U.S. equity-index futures were little changed with European shares, while Asian markets drifted lower. Tokyo's benchmark dropped. The dollar rose against most major peers. Oil advanced along with most industrial metals.

Author

Clint Sorenson, CFA, CMT

WealthShield