The Iran war won’t save the US Dollar

The US Dollar is performing relatively well as investors have turned to it as the go-to place amid escalating geopolitical tensions. While the safe-haven card can work as a short-term tailwind, fundamental problems such as the US twin deficit problem remain untackled, and these could start to matter more as the year unfolds.

Short-term strength, long-term pressure?

The US Dollar remains within striking distance of the year-to-date high set in March amid inflationary concerns stemming from the Iran war. Recent data reflecting a resilient US economy has also supported the Greenback.

Inflation remains sticky, and the Federal Reserve is in no rush whatsoever to cut interest rates aggressively.

This is good for the US Dollar, but in the end, it is just a short-term driver. The broader structural trends point to a downfall by the year-end once the current geopolitical premium stemming from the Iran war unwinds.

The issue markets are currently ignoring: the twin deficit

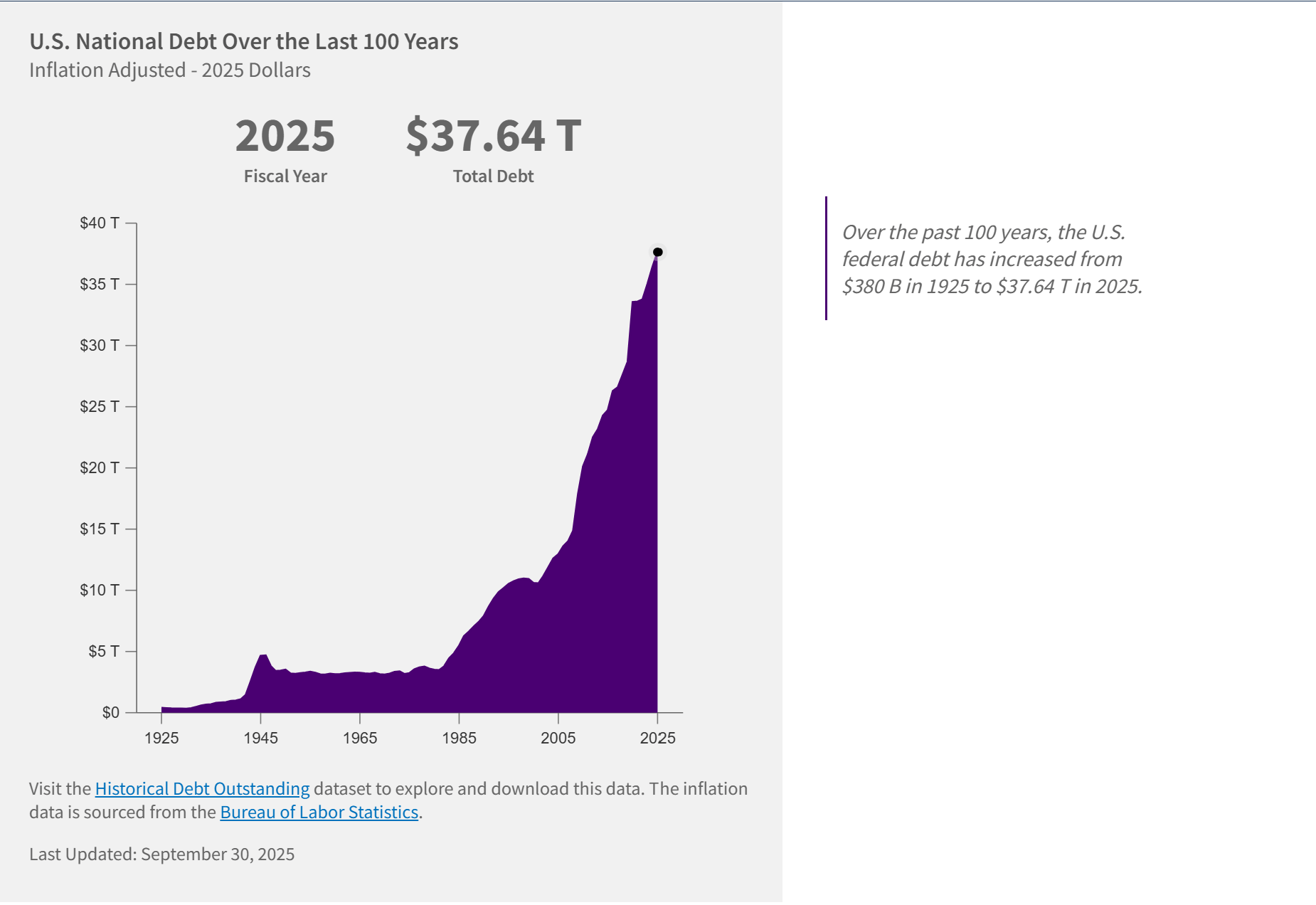

The US faces a textbook twin deficit that refers to the simultaneous occurrence of the fiscal shortfall and current account or trade deficit. The federal government's fiscal year 2026 budget deficit is about $1 trillion as of February, and major drivers include rising interest payments on the debt, which exceeded $38 trillion by early 2026 and represents a debt-to-GDP ratio of over 120%.

High debt reduces financial flexibility and poses economic risks as more resources are allocated to interest payments rather than productive investment.

This creates incentives for policymakers to constrain the central bank’s independence and lean on looser monetary and fiscal settings to boost nominal growth. As the economy expands, the debt-to-GDP ratio falls, and the real value of existing government bonds erodes.

A growing reliance on foreign capital adds to the vulnerability

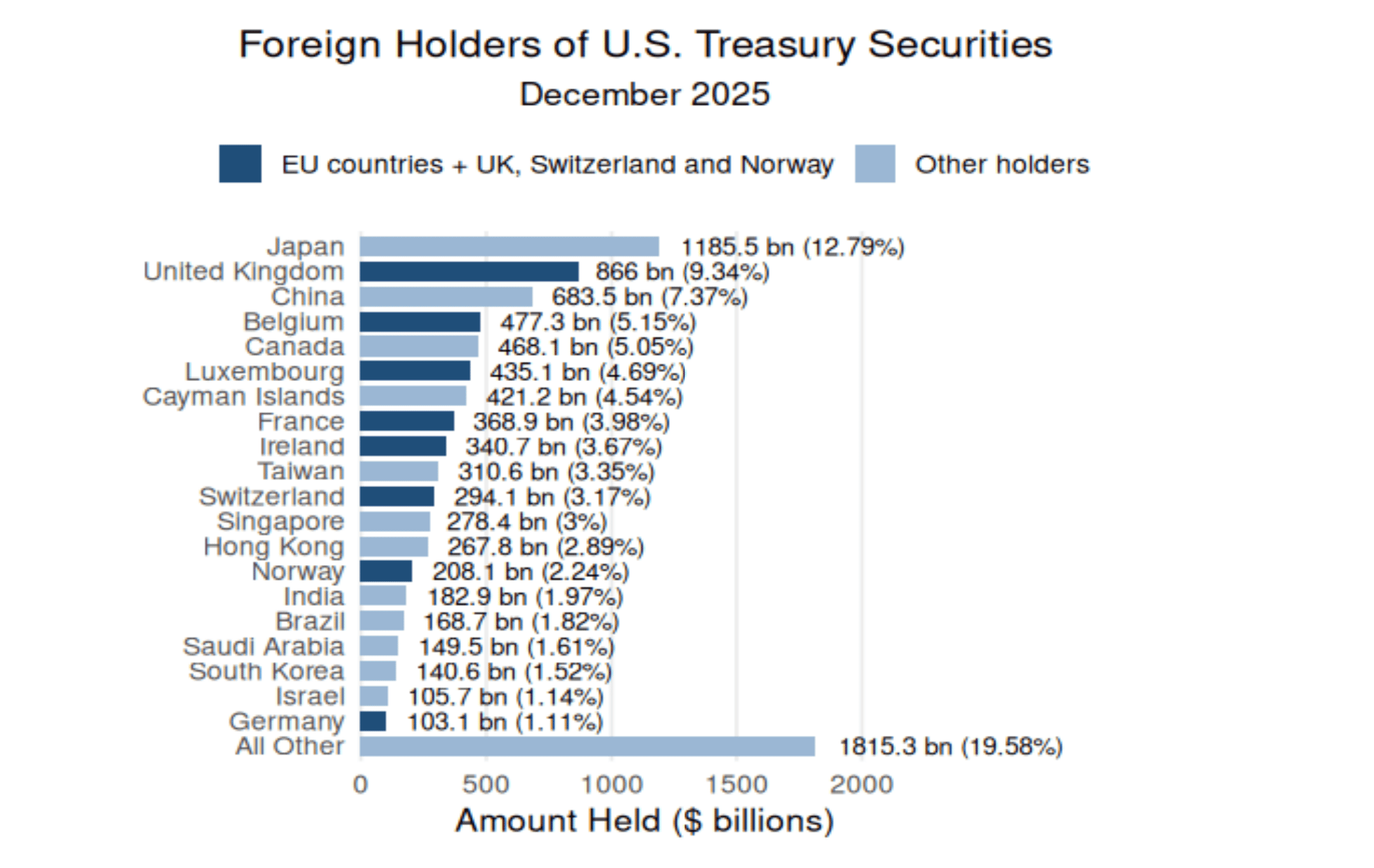

The US finances its deficits largely through the sale of Treasury securities and has the largest external debt globally, with China, Japan, and other nations holding a significant portion, around 25% of Treasury bills.

Although the US government is not currently experiencing a cash-flow crisis, the heavy reliance on foreign capital to fund the twin deficit increases vulnerability to sudden shifts in investors' confidence.

Why the Dollar is still holding up… and what could change the trend

The lack of a serious competitor to the Greenback's dominance as a reserve currency mitigates immediate risks. The Federal Reserve's hawkish stance and expectations of slowing rate cuts or an extended hold to combat persistent inflation support the buck.

However, if geopolitical tensions ease and the current risk premium fades, markets may begin to focus more on fundamentals. And then, the worsening fiscal math and faster rate cuts by the US central bank could trigger the resumption of the USD's steep decline from the two-decade high touched at the beginning of the century.

Technical Analysis: Bearish bias persists despite recent consolidation

The US Dollar Index (DXY), which tracks the Greenback against a basket of currencies, is holding above the 23.6% Fibonacci retracement level of the decline from the January 2025 swing high. The DXY, however, has been oscillating in a range over the past five weeks or so and lacks bullish conviction. Moreover, a breakdown and acceptance below the 200-week Simple Moving Average in April 2025 – for the first time since November 2021 – favours long-term bears.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.