Platinum trade idea: A long case with a timing problem

Platinum is starting to look like one of the more attractive commodities trades, but it is not yet a clean breakout. The better view is cautiously bullish: the fundamentals support a medium-term long idea, sentiment is not overcrowded, and the market still has a tight supply backdrop. The problem is timing. The chart has improved, but it has not yet confirmed a full bullish reversal.

That makes platinum a good trade idea, but only with discipline. This is not a market to chase blindly. The cleaner setup is either to buy a pullback into support or wait for price to break and hold above the first major resistance zone.

Trade idea summary

Bias: Conditional long platinum.

Preferred setup: Staged long or wait for confirmation.

Conviction: 72/100.

Time horizon: 3–9 months.

Current price area: Around $1,660.

Key confirmation: Break and hold above $1,685–$1,700.

First upside area: $1,760–$1,765.

Major resistance: $1,875–$1,900.

Higher resistance: $2,050–$2,100.

Key support: $1,607–$1,620, then $1,580–$1,600.

Invalidation: Sustained break below $1,530–$1,550.

The trade is stronger as a medium-term long than a short. The main issue is that the fundamental case is ahead of the technical confirmation.

The fundamental case is stronger than the chart

Platinum still has a genuine tightness story.

Supply remains highly concentrated, especially in South Africa. That matters because South African production carries recurring operational risks: electricity shortages, labour disruption, ageing infrastructure, cost pressure, water issues and political uncertainty. When one country dominates such a large share of global mine supply, the market does not have much room for error.

This is not a commodity where supply can quickly respond to higher prices. New platinum projects take years to develop, capital discipline across the mining sector remains tight, and much of the spending that is taking place is aimed at maintaining existing production rather than creating a large wave of new supply.

Recycling should improve as higher prices encourage more autocatalyst recovery, but the rebound still looks gradual. It may ease the deficit, but it does not appear strong enough on its own to remove the tightness risk.

Demand is also broader than platinum is often given credit for. Automotive demand remains the core driver, especially through catalytic converters in diesel and hybrid vehicles. Electric vehicles are a long-term challenge, but the shift is not happening evenly across every region or vehicle type. Hybrids and heavy-duty vehicles still support platinum demand.

Substitution has also helped the market. When palladium traded at a large premium, automakers had an incentive to use more platinum where possible. That has strengthened the demand base. The risk now is that platinum’s premium over palladium has widened again, so the substitution argument cannot be treated as one-way forever. If the spread stretches too far, demand could start to move back towards palladium in some applications.

Jewellery demand is mixed, but high gold prices give platinum some relative appeal. In markets where consumers are being priced out of gold, platinum can look more attractive. China remains uneven, but the relative value argument is not dead.

Industrial demand adds another layer of support. Platinum is used across chemicals, glass, petroleum refining, electronics, medical applications and pollution-control technology. Hydrogen and fuel cells are not yet big enough to carry the whole bull case, but they do provide long-term optionality. That theme should be seen as an upside kicker, not the core reason to buy platinum today.

The fundamental picture is therefore constructive: constrained mine supply, limited new investment, persistent deficits, thin inventories and a demand base that is more diversified than many investors assume.

Sentiment is mixed, which may be a good thing

The sentiment picture is not wildly bullish. That is important.

This does not look like a crowded long. Futures positioning is constructive, but not extreme. Investors are interested, but the market is not showing the sort of one-sided enthusiasm that usually makes a trade vulnerable.

ETF flows are the weak spot. Platinum ETF holdings have been under pressure, and that selling has helped cap the price despite the supportive physical story. In simple terms, the physical market may be tight, but investor liquidation has been adding supply back into the market.

That is also where the opportunity sits. If ETF outflows slow, stabilise or reverse, platinum could start responding much more cleanly to the deficit story. A turn back into ETF inflows would be an important bullish signal.

Options activity has cooled as well, which suggests speculative interest has faded from earlier highs. Again, that is not necessarily negative. Some of the best commodity opportunities appear when the fundamental case is improving but investor sentiment has not fully returned.

The sentiment setup is best described as mixed, not bearish. It is not euphoric, which gives platinum room to attract fresh capital if the chart confirms and macro conditions become less hostile.

Macro is the main short-term headwind

The main obstacle for platinum is not the supply-demand story. It is macro.

A firm US dollar, elevated real yields and a still-restrictive Federal Reserve are all short-term headwinds. Platinum may have industrial demand, but it still trades partly like a precious metal. When real yields are high and the dollar is strong, non-yielding metals usually struggle to build sustained upside momentum.

That is why the trade needs patience. A weaker dollar, falling real yields or a softer Fed tone would make the long setup much more attractive.

China is another important swing factor. Stronger manufacturing data, better industrial activity or improved consumer demand would help platinum. A renewed slowdown would weigh on both sentiment and demand expectations.

Relative value also matters. Platinum still looks historically cheap versus gold, which supports the idea of catch-up potential. Gold has already had a strong run, while platinum remains discounted on a relative basis. That could attract investors looking for value within the precious metals space.

Against palladium, the story is more complicated. Platinum still has a stronger structural deficit argument, but its premium over palladium should be monitored. If platinum becomes too expensive relative to palladium, the substitution tailwind could start to fade.

The technical picture has improved, but it has not turned fully bullish

The chart is the reason not to rush.

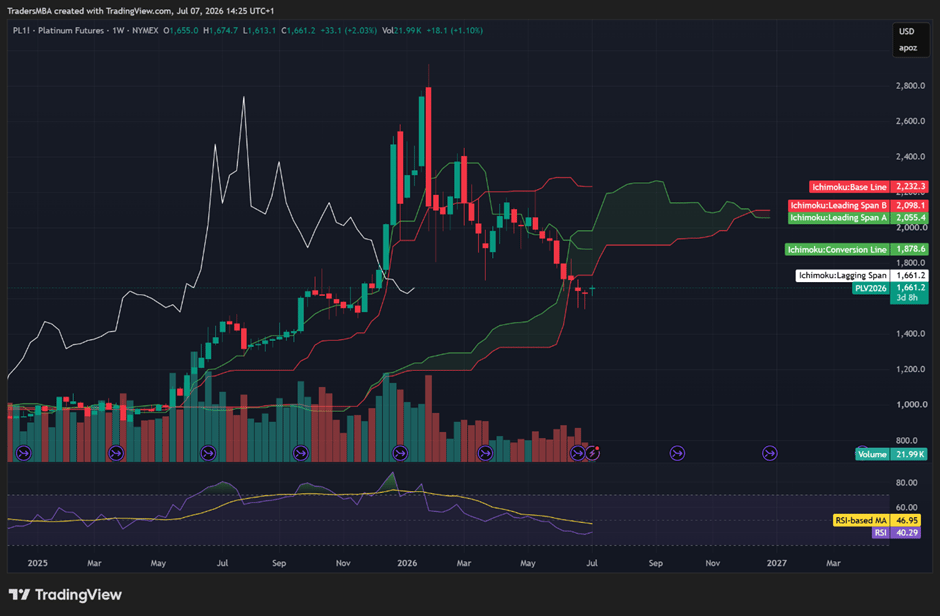

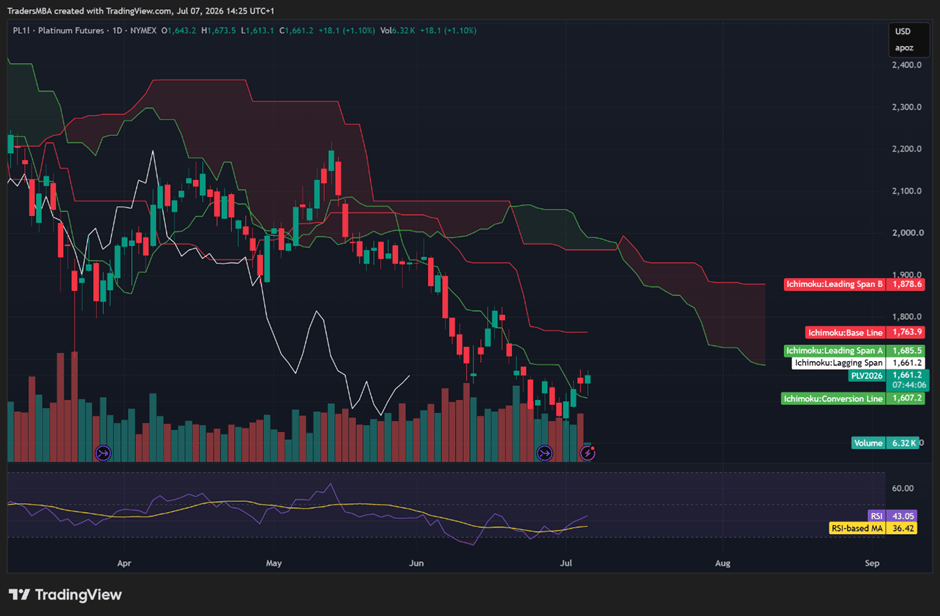

On the daily chart, platinum has recovered from the recent low area around $1,530–$1,560 and is trading near $1,660. Price has moved back above the daily Ichimoku conversion line around $1,607, which is a positive short-term sign. RSI has also improved and is now above its own moving average, showing that downside momentum has eased.

But this is still a recovery attempt, not a confirmed bullish reversal.

The immediate resistance zone is $1,685–$1,700. That is the first level platinum needs to clear. A daily close above that area, followed by a successful retest, would make the long trade much more credible.

Above that, $1,760–$1,765 becomes the next upside target. The more important resistance zone sits around $1,875–$1,900. A move into that area would suggest platinum is no longer just bouncing from oversold conditions, but potentially building a wider trend recovery.

The weekly chart is still less convincing. Platinum remains below the weekly Ichimoku conversion line, base line and cloud. That means the medium-term trend has not yet turned bullish. Weekly RSI is still in the low 40s, which shows stabilisation rather than strength.

This creates a clear split. The fundamentals are bullish, but the technicals are still repairing. That does not kill the long idea, but it does mean execution matters.

There are two cleaner ways to approach the trade.

The first is a breakout setup. Platinum needs to close above $1,685–$1,700 and hold that area. That would open the way towards $1,760–$1,765, with $1,875–$1,900 as the bigger test.

The second is a pullback setup. A move back towards $1,607–$1,620 that holds support would offer a better entry than buying just below resistance. If that area holds and price forms a bullish reversal, the risk/reward improves.

The key downside level is $1,530–$1,550. A sustained break below that zone would damage the recovery structure and suggest the market is not ready to price in the bullish fundamental case.

Catalysts that could unlock the trade

The first catalyst is simple: a break above $1,685–$1,700. That would show buyers are willing to take control above near-term resistance.

The second catalyst is a stabilisation in ETF flows. If investor selling slows or turns into buying, platinum could reprice quickly because the physical market already looks tight.

A weaker US dollar would also help. So would lower real yields or a less hawkish Fed tone. Platinum does not need a dramatic policy pivot, but it does need the macro backdrop to stop working against it.

China is another catalyst. Stronger manufacturing PMIs, better industrial production or signs of stronger consumer demand would support both the industrial and jewellery sides of the market.

Supply disruption is the upside risk that should not be ignored. Any meaningful production issue in South Africa, Russia or Zimbabwe would quickly remind the market how concentrated platinum supply really is.

Renewed tightness in physical indicators, such as lease rates, would also strengthen the case. If the physical market tightens again while investor flows stabilise, the long setup becomes much more attractive.

The main risks

The biggest risk is that macro stays hostile. If the dollar remains strong and real yields continue rising, platinum may struggle even if the physical balance remains supportive.

ETF selling is another risk. Continued liquidation would keep adding supply back into the market and could delay any upside move.

Recycling could also recover faster than expected. If secondary supply comes back strongly, the deficit could narrow and weaken the bullish story.

China remains a demand risk. Weak manufacturing data or poor jewellery demand would make it harder for platinum to sustain a rally.

Substitution risk also needs watching. Platinum’s premium over palladium cannot widen forever without raising questions about whether automakers will shift back where possible.

The technical risk is clear. If price breaks below $1,530–$1,550, the long idea loses its structure.

Final verdict: A good long idea, but not a chase

Platinum is a good commodities trade idea on the long side, but it is not yet a perfect setup.

The fundamental case is clearly stronger than the bearish case. Supply is constrained, mine growth is limited, market deficits persist, inventories are tight, and demand is broader than many investors assume. Sentiment is also useful because it is not crowded. ETF flows have been weak, but that gives the trade upside if those flows stabilise or reverse.

The technicals are the missing piece. The daily chart is improving, but the weekly chart has not yet confirmed a full trend reversal. Until platinum breaks and holds above $1,685–$1,700, the market is still in recovery mode rather than confirmed breakout mode.

The best approach is therefore disciplined bullish exposure. Either scale into a pullback near $1,607–$1,620, or wait for a confirmed break above $1,685–$1,700 before increasing conviction.

A move above $1,700 would strengthen the long setup. A move through $1,760 would add further confirmation. A push towards $1,875–$1,900 would suggest the market is finally starting to price in the tighter fundamental backdrop.

For now, platinum is a stronger long than short idea, but the trade should be entered with patience rather than excitement. The story is attractive. The entry still needs to be earned.

Author

Sachin Kotecha

International Trading Institute (ITI)

Sachin Kotecha is a multi-asset trader, Professor at the International Trading Institute, and creator of institutional trading frameworks, macroeconomic intelligence platforms, and professional trading education programmes.