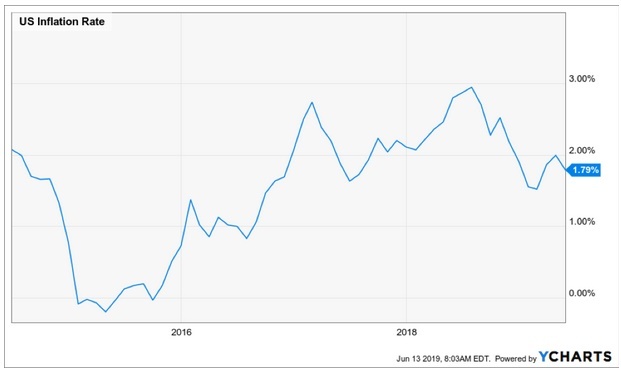

The inflation rate in the US picked up 0.1% month over month

Highlights:

Market Recap: The S&P 500 finished down -5.88 points or -0.20% on the day. The benchmark 10 year yield dropped 2 basis points to finish the day at 2.13%. Gold and the dollar were both up on the day.

Economic Data: The inflation rate in the US picked up 0.1% month over month, matching expectations. On a year over year basis, inflation is up 1.8%. This is considerably less than the peak of near 3% seen in 2018.

Transports: The Dow Industrials Transportation index outperformed broad markets yesterday. The IYT ETF gained 0.45%, while the S&P 500 was down -0.20%. Continued upside in the transports index could imply further upside in risk assets.

Oil: West Texas Intermediate Crude dropped -4% yesterday on a report of further inventory buildup. The drop yesterday broke to new intermediate term lows. There is psychological support around the $50 level. A break below that could suggest further downside to the 2018 low. Oil is up over 3% this morning due to a Tanker attack in the Gulf of Oman.

Lumber: The Lumber/Gold ratio rallied again yesterday, finishing up 2.92%. The ratio is still in a negative trend, but the bounce could signal further upside in equities markets if it continues.

Low Volatility: The low volatility factor remains elevated relative to high beta equities (SPLV:SPHB). We expect this relationship to turn downward in support of a continued upward move in equity prices. If it remains in favor of low volatility, this would suggest a more defensive positioning is present and could signal risk aversion. The trend is positive for this ratio, implying that the strength and leadership remains with the low volatility stocks. The trend moved positive back in October of 2018 and has not reversed course.

Growth: The growth factor remains strong relative to the broad market. This is quite divergent from the slowing economic data and defensive positioning seen within other market segments. It is almost as if the stock market is torn between the growth slowing trajectory or a late-cycle reacceleration. As long as growth remains strong and in a positive trend, the market could press higher.

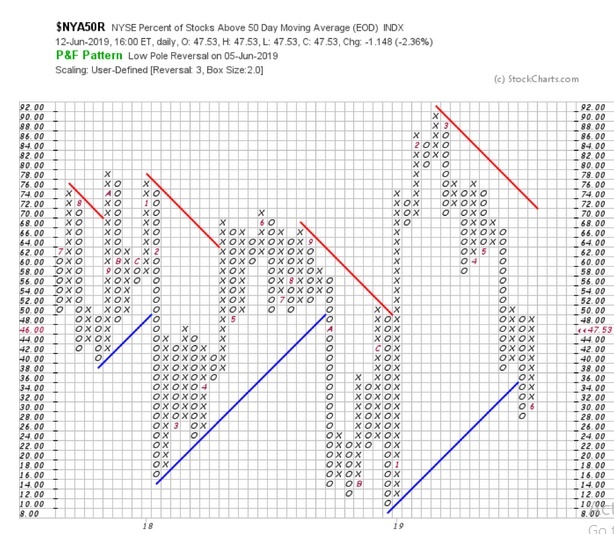

No longer oversold: The index that tracks the percentage of stocks in the NYSE that are above their 50 day moving averages signaled to us that an oversold rally could materialize. That same index has improved substantially since the beginning of the month. Markets are no longer oversold. A reversal of this index back into a column of O’s could be a signal that the oversold rally is over. However, the market is not overbought, so a continued advance would not be a surprise. If this index breaks above 52%, that would imply a buy signal (from the point and figure charting methodology).

Futures Summary:

News from Bloomberg:

Oil surged after two tankers were damaged in a suspected attack in the Gulf of Oman, near the Strait of Hormuz, just weeks after a previous incident in the region. One was on fire after being hit by a suspected torpedo, unconfirmed reports said. No one has claimed responsibility. Brent crude jumped as much as 4.5% in London on the prospects of further supply disruptions in the Middle East.

U.S. stock-index futures rose with European equities, while Asia's markets were mixed. Hong Kong shares halted losses triggered by massive protests. Gold climbed as Treasuries and the yen were marginally higher. The dollar was little changed.

China will "fight to the end" if the U.S. insists on escalating the dispute, Ministry of Commerce spokesman Gao Feng said, in a strong response to Trump's reiterated tariff threat. Beijing firmly opposes U.S. unilateralism and hegemony and warned that a trade war will trigger a recession in the U.S. and the global economy.

Russia's not happy either. Vladimir Putin hit back a day after the president slammed Russian gas supplies to Europe. "Our relationship with the U.S. is degrading, it's becoming worse and worse," Putin said. In the tariff war his sympathies are with "our strategic partners." Turkey is mad too. President Erdogan accused the U.S. of arming Kurdish militants in Syria in an effort to topple his government.

Hong Kong was calmer but tensions were high as lawmakers scrapped debate for a second day on legislation that would allow extraditions to China. Protest organizers called for a march on Sunday. Hong Kong's General Chamber of Commerce, which says it represents businesses employing a third of the local workforce, said the public has "serious apprehensions" about the bill and urged the government to engage in "meaningful dialogue."

Author

Clint Sorenson, CFA, CMT

WealthShield