The Great Divide in the bond market will heavily influence the FX market

Outlook:

The Great Divide in the bond market will heavily influence the FX market. One camp views Trump policies as a growth generator, especially fiscal spending and tax cuts. Growth may not get to 4-5%, but 3%+ is possible, along with some inflation that will light a fire under the Fed. Yields should easily reach and hold 3%, something we haven't seen since 2014.

The other camp sees the Trump trade as overdone. We are not going to get robust new growth from Trump policies, at least not any time soon. Instead various disruptions like trade are going to drive growth down, perhaps into recession or near-recession.

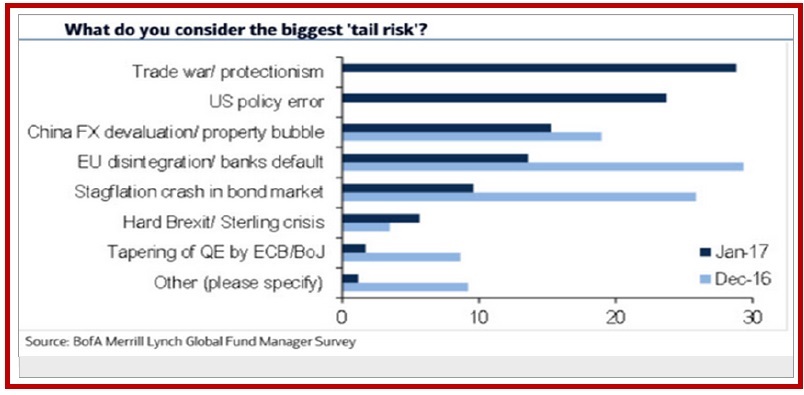

What are the risks, exactly? See the BoA ML survey results below (from the Daily Shot). Notice that protectionism is a growth-killer and these experts fear "policy error" almost as much. Also, tapering of QE is far down the list and less than 5%. This can't be right, can it?

It's tempting to buy into the negative interpretation of Trump's fair trade ideas, not only because of generally lower levels of activity but also the retaliation threat. And yet the first real case we will get comes this Friday when UK PM May visits Washington specifically to get a trade deal. Oh, yes, the two leaders are also going to talk about Nato and beating terrorism, but the biggie is trade. One idea is that the UK will get a "passport" deal with the US allowing UK banks to expand tremendously in the US. Here the backstory might be useful. Many big American banks, including Citibank, have written off Trump loans. They won't lend to him anymore. He might be in the mood to poke a stick in their eyes.

Besides, Trump views Brexit as akin to Trumpism and Bloomberg suspects he might be feeling gener-ous. One report has it that May wants to streamline labor flows between the two countries. Bloomberg writes "A Transatlantic trade pact, even if it couldn't be signed until after Brexit, would allow May to show her EU interlocutors that the U.K. can prosper outside of the EU and so demand more from the Brexit deal. On the flip side, EU officials could resent her cozying up to someone who predicted the breakup of their bloc, and seek to punish her for it."

Note that May next goes to Turkey—not Canada, which would be the logical choice. But Canada is busy doing a trade deal with the EU. Trouble in the Commonwealth, maybe. Meanwhile, it looks like the next Trump trade talk will be Jan 31 with Mexican Pres Pena Nieto. Yikes. And the FT reports that now TPP is a dead duck, Australia may be interested in a new trade deal with China.

We see a third implication lurking in the bushes—Trump is all too likely to say that allowing Brits into the US under a special passport deal is to accept good white people while still rejecting those terrorism-prone brown people. The good white people will only be temporary, anyway, and those terrorism-prone brown people seeking permanent residency must be kept out--permanently. Yesterday Trump met with Congressional leaders and repeated the lie that he lost the popular vote because of voting by illegal im-migrants. Two things: he is still obsessing about losing the popular vote. And he is still lying. Presi-dents are expected to lie about a few things pertaining to national security, for example, but not lies that undermine trust in our institutions. And the third thing is a hardening of the Trump stance against im-migrants. At least the brown ones. It's shameful.

Not to beat a dead horse, but Trump's bankruptcies (and unwillingness to disclose taxes and debt owed to international banks) should have disqualified him in the eyes of the voters. The intent to restrict im-migration to good white people while excluding Muslims is un-Constitutional and should have disqual-ified him in the eyes of voters. The Great Divide is a social one as well as a bond market one.

Critics complain that we have too much uncertainty about Trump's actual policies. This is because he has said contradictory and false things. But when it comes right down to the key campaign promises, we have no reason to suppose he will do anything other than what he said he would do—get rid of free trade in favor of fair trade, cut corporate taxes, raise infrastructure spending, and promote America First, which almost certainly includes a strong dollar. We await Trump's first use of the Rubin mantra, "a strong dollar is in the US best interests."

The fundamentals, if they don't run off the rails, favor higher growth arising from tax cuts and some fiscal stimulus. Assuming there is some inflation in there, the Fed will have to become more pro-active. As noted previously, we don't see it yet in rising expectations for that third hike this year, although hedgies are getting into TIPS. Higher returns support a stronger dollar.

One tidbit originating in a FT story about re-writing NAFTA comes from a guy at the Peterson Insti-tute, which knows a thing or two about trade. The thrust of the article is that NAFTA is a really big deal—over $1 trillion in trade among the US, Canada and Mexico. But the useful nugget is the econo-mist Hufbauer, who says "This is a president of symbols. But we have to distinguish between the sym-bol and the substance. What Trump needs for his base and to answer his political promises is to get rid of this five-lettered name [Nafta]. But underneath that name there are a lot of working parts."

Hufbauer's point is that "the 1987 deal could be one of the building blocks of a successor to Nafta should the latter collapse." Technically, Congress would have to repeal Nafta. Changing it is tremen-dously difficult. Hufbauer does't say so, but Trump lacks patience. Actually, Congress lacks patience, too. It took many years to build Nafta and the implications of changing just about anything reverberate and pin-ball around multiple areas, including FDI and various tricky legal things. It can't be done with the stroke of a pen.

We have signal vs. noise and now symbol vs. substance. We are going to steal that one.

Unless we continue to get sound-cites masquerading as policy, and that's a distinct possibility, at some point the dollar will be perceived as oversold. A problem bigger than Trump is really quite good data from Europe, like today's flash PMI's. Still, we think we see resistance looming over the euro up there in the stratosphere (1.0850) and we can easily revert back to the primary trend. The current correction is bigger and longer-lasting than the ones that came before so that remains a worry. Does it mean it should be ending any day now or is it a harbinger of continuation? We never had a president like this before, so we lack any history to consult. Gird your loins.

| Current | Signal | Signal | Signal | |||

| Currency | Spot | Position | Strength | Date | Rate | Gain/Loss |

| USD/JPY | 113.42 | SHORT USD | WEAK | 01/05/17 | 115.93 | 2.17% |

| GBP/USD | 1.2451 | LONG GBP | NEW*STRONG | 01/24/17 | 1.2451 | 0.00% |

| EUR/USD | 1.0727 | LONG EURO | WEAK | 01/10/17 | 1.0587 | 1.32% |

| EUR/JPY | 121.70 | LONG EURO | STRONG | 11/03/16 | 114.30 | 6.47% |

| EUR/GBP | 0.8615 | LONG EURO | WEAK | 01/09/17 | 0.8649 | -0.39% |

| USD/CHF | 1.0014 | SHORT USD | WEAK | 01/05/17 | 1.0113 | 0.98% |

| USD/CAD | 1.3292 | SHORT CAD | WEAK | 01/05/17 | 1.3253 | -0.29% |

| NZD/USD | 0.7209 | SHORT NZD | WEAK | 12/19/16 | 0.6963 | -3.53% |

| AUD/USD | 0.7555 | LONG AUD | STRONG | 01/05/17 | 0.7343 | 2.89% |

| AUD/JPY | 85.71 | LONG AUD | WEAK | 10/06/16 | 78.48 | 9.21% |

| USD/MXN | 21.4517 | LONG USD | STRONG | 10/31/16 | 18.9054 | 13.47% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat