The Governor [Video]

![The Governor [Video]](https://editorial.fxstreet.com/images/Macroeconomics/CentralBanks/BOE/Mark_Carney1_2016_XtraLarge.jpg)

The Day So Far…

Mark Carney set the record straight in his delayed Mansion House speech this morning stating that “now is not the time to raise interest rates given anaemic growth and mixed signals in consumer spending”. The news placed immediate pressure on the Pound as the commentary was in clear contradiction to the more hawkish elements of last week’s MPC minutes which showed a move towards a 5-3 vote split, the most hawkish divide seen in the voting pattern for several years. Prices soon bounced after briefly testing S2 (1.2704) in GBP futures with the move seen somewhat of an over reaction likely exacerbated by algorithmic systems in what was really the expected view of the governor and the majority of the Committee given the decision to not take action this month. However, the latest twist has been comments from S&P Managing Director Moritz Kraemer who has said that the rating agency does not have to wait for Brexit terms in order to take action on Britain, most likely to cut its rating.

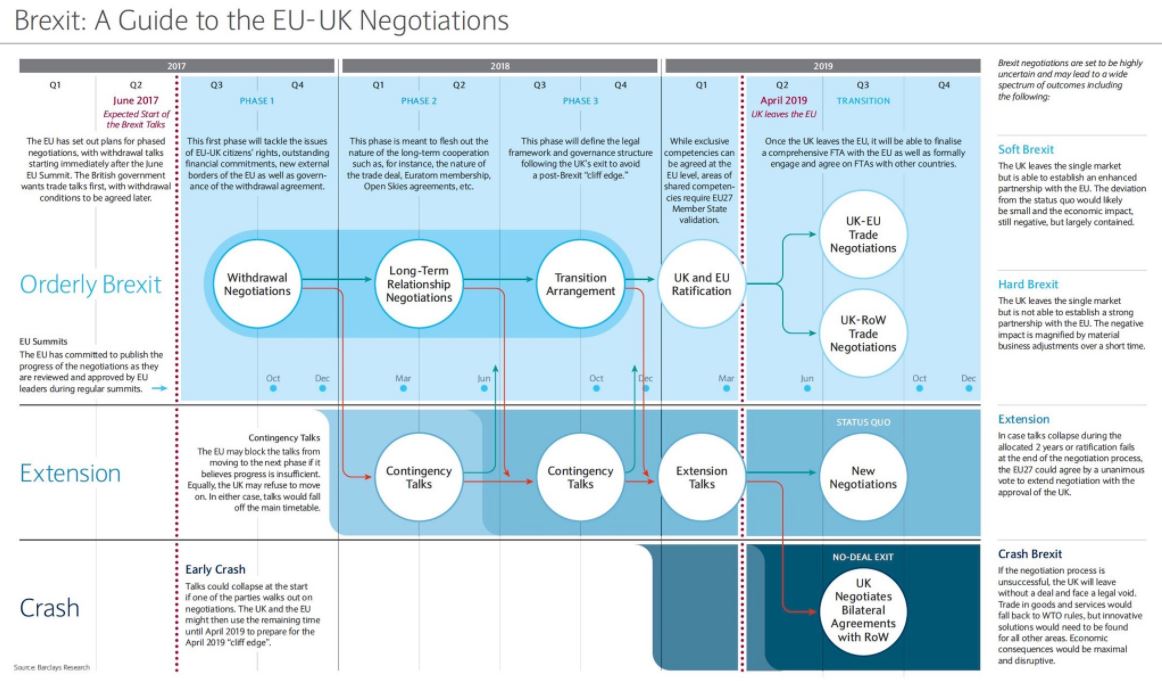

Meanwhile, Brexit talks have now commenced and the first day of discussions was fairly amicable with David Davis already conceding on sequencing by dropping demands for parallel trade negotiations. At this point in the process I would not be expecting anything other than a harmonious start to proceedings but with EU leaders meeting this Thursday and Friday the weekend’s new coverage should provide some further insight as to the sum Europe would be happy to accept in order to look beyond the settlement fee.

The Day Ahead…

As we head into the North American open WTI crude has taken another leg lower breaking key support level from yesterday to now print at the lowest level since November last year. It’s important to note that the last downside has not been driven by any new fundamental developments rather the on-going concerns of US output continuing to flood the market and question marks looming over OPEC long-term strategy. If prices continue to tick lower from here then the likelihood of a response from OPEC nations increases, whether direct or via sources, but I would not expect this to really intensify unless we drop towards $40/bbl. Elsewhere, although we maintain our preference for long entries in the S&P I would not be surprised to see a period of consolidation which has become quite typical behaviour post a fresh breach to new all-time highs as was seen yesterday.

Author

Amplify Trading Team

Amplify

Amplify Trading is a proprietary trading company specialising in the development of new trading talent offering direct experience in financial markets.