The global knock-on from Japan’s policy change

The BoJ has been slowly moving away from its ultra-loose monetary policy but has been doing it in slow stages. First of all, we had the yield curve expanded and now we had rumours of a more hawkish BoJ Governor, Ueda, being lined up to take the reins. These moves have led to anticipation that the BoJ is going to let the reins go and allow rates to move higher. If we see inflation data coming in higher than expected over the next few weeks then that move could even come before the new BoJ Governor is in a situation for the March 10 BoJ meeting.

The implication for the bond market

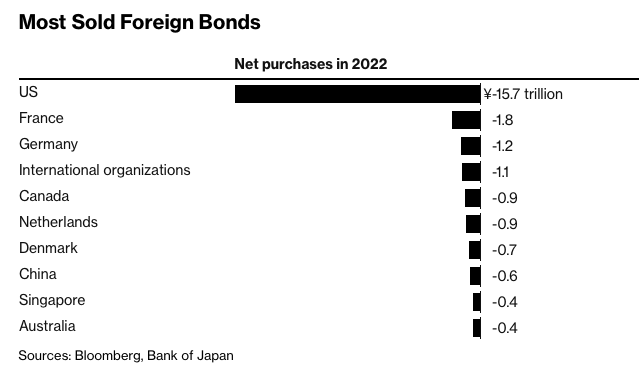

Bloomberg points out that last year Japanese investors offloaded $181 billion of foreign debt and put $231 billion into Japan’s domestic bond market. Look at the heavy amount of foreign bonds that Japanese investors sold. The majority of that debt was US bonds.

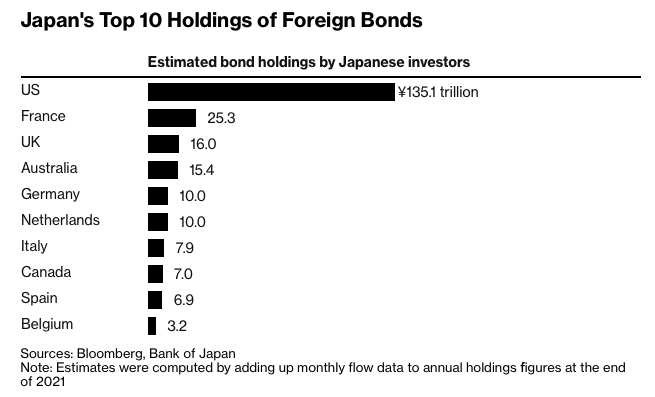

According to JPMorgan Chase & Co analyst Benjamin Shakil, this trend is set to continue. The risk here is that if the BoJ does exit its easy monetary policy program that will have spillover effects. That would strengthen the Yen, send US yields higher as more US treasuries find sellers, and send gold lower (on the higher rate and stronger dollar environment). The reason for this impact is that Japan still holds more than $1 trillion of US Treasuries as well as large amounts of bonds from France and the UK.

-638119669680333389.png)

When Japan does finally exist its easy monetary policy program then that could mean domestic bonds find buyers as foreign bonds are sold. Patient Japanese investors will likely buy JGBs on the more attractive yields. Watch out for this dynamic and the implications it could have moving forward across a range of markets. The first beneficiary would of course be the JPY.

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.