The FX market is paralyzed by conflicting sentiments

Outlook

The FX market is paralyzed by conflicting sentiments. This happens sometimes and we identify it when typing the new quotes into the spreadsheet. Today the euro was 0.0001 different from the day before. The AUD and CAD were the same. The dollar lost an interesting amount only against—the peso.

As we also see in equities, the absence of panic implies the majority feel sure Trump will not bomb Iran back into the Stone Age tonight (although the US just bombed military sites on Kharg Island, according to Axios). If he comes up with yet another excuse to delay, stocks will indeed rally as futures suggest. Yields will fall a bit more, as they are already doing. The outlier is oil, which has a big enough fear cohort to shove the price of Brent up overnight.

Bloomberg uses the word “frustration” rather than “screaming fear.” The WSJ reporter who recently interviewed Trump has three scenarios. First is no action, the least likely. Second is another postponement on the grounds that talks are actually happening. Third is those strikes. We find this a shockingly inadequate report. The reporters doesn’t confide in the reader that he perceives Trump thinks he knows what he is doing. Granted, that’s a subjective judgment, not reportable “news.” The liberal press thinks Trump is deranged and out of control, while the righties are laughing at his shenanigans and believe he knows what he is doing. They both can’t be right.

If the US does bomb Iran tonight, the economic effects globally will be huge. Another delay for those non-existent talks buys time, which does have the virtue of giving breathing room for companies to reconsider supply chains and central banks to chew on upcoming inflation.

We have days to go but the consensus is that the upcoming inflation data, central to the Fed outlook, could be a tipping point. The services PMI had “prices paid” jump to 70.7 from 62.0, ING reminds us. And March CPI on Friday will likely jump to 3.4% from 2.4% on gasoline alone.

It’s interesting that ING views CPI as more important than PCE/core PCE, which is the Fed’s preferred measure. The U Michigan consumer confidence that same morning will be influential. Let’s remember again that this survey is of only a few thousand people and honestly, not representative nor deserving of the attention.

A “good” outcome of Trump actually following though would be acceptance of Canadian PM Carney’s statement that the world order has changed forever. Tariffs, threats to leave NATO, threats to invade a NATO ally’s territory, in and out of Ukraine, invading Venezuela and kidnapping its president, insulting everyone in sight, lying and vulgarity, corruption on multiple fronts—the list goes on. Trump is breaking not just America’s self-appointed world leadership, but America itself, the land that no longer has decency norms and a working constitution.

Forecast

Markets expect another postponement of a US all-out strike on Iran, and that suggests the dollar can lose a few pounds today. But sane traders will be squaring up well before 8 pm, anyway, and the dollar can lose a lot more overnight on a delay. Still, the primary trend is up for the dollar and down for everything else, so don’t build to big or long-lasting a short position. For what it’s worth, we give the probability of 49% to the Trump strike, much higher than the market.

Food for thought one

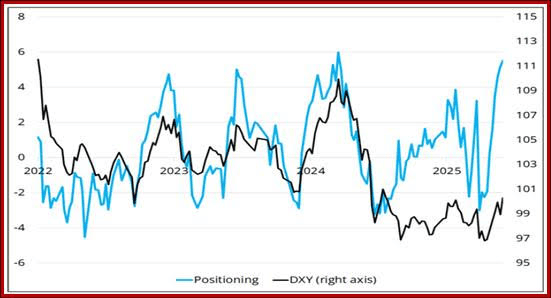

Last week Brent Donnelly had an interesting take on the dollar—that the Iran war “is actually a USD-negative macro event but the market was forced to buy USD to exit massive pre-war USD shorts and to hedge risky assets through EURUSD puts etc. Not a USD bull market, more like forced buying. And that forced buying didn’t have a huge impact on price.”

See his chart. This is a Donnelly’s remake of the CFTC Commitment of Traders report, presumably showing hedge fund positioning alone. Remember that the COT is released on Friday for data ending the previous Tuesday, so excluding Wed-Fri information. The goal is to find turning points.

Plenty of analysts use this data to scope out their next move, so even if the statistics are not that great, when a lot of traders are coming to the same deductions, you get a self-fulfilling prophecy.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat