US Dollar Weekly Forecast: Sticky inflation keeps the higher-for-longer story alive

- The US Dollar ends the week with marginal losses.

- The resurgence of geopolitical tensions was the salient theme.

- Investors will now shift their attention to upcoming US CPI data.

The week that was

The US Dollar (USD) has traded in a volatile fashion this week, leaving the US Dollar Index (DXY) slightly positive around the 101.00 neighbourhood.

This week’s price action has been mainly influenced by the renewed tensions between the US and Iran and how that affects the Strait of Hormuz, pushing the ongoing concern about possible FX intervention by the Japanese Ministry of Finance (MoF) to the background, while expectations for more interest rate hikes by the Federal Reserve (Fed) have stayed strong.

In addition, the publication of the FOMC Minutes was kind of spot on with market expectations, leaving the eventual hawkish message largely anticipated and the Greenback’s reaction apathetic.

Fed doubles down on higher-for-longer stance

The Fed reinforced its higher-for-longer message over the past week through officials' remarks, the June FOMC Minutes and Friday’s Monetary Policy Report.

Fed Governor Christopher Waller reaffirmed the central bank's unwavering commitment to its 2% inflation target, arguing that stronger inflation and a stabilising labour market had shifted the balance of risks. He stressed that policy would not be used to help finance government deficits and said clearer communication was needed if the Fed's reaction function was not well understood.

New York Fed President John Williams echoed the hawkish tone, saying inflation remained too high despite improving prospects from lower energy prices. He described the labour market as stable, reiterated that policy was well positioned and data-dependent and argued that AI investment should eventually boost productivity even if it contributes to near-term inflation.

The June FOMC Minutes showed policymakers remained primarily concerned about inflation, with several officials warning that AI investment, tariffs and renewed Middle East tensions could keep price pressures elevated. While rates were left unchanged unanimously, a few participants judged that further tightening could eventually become appropriate if inflation proved more persistent, reinforcing the view that the bar for rate cuts remains high.

The Fed's Semiannual Monetary Policy Report delivered a similar message. The central bank said inflation accelerated further in the spring due to tariffs, the Middle East conflict and AI-related factors, while emphasising that longer-term inflation expectations remained anchored at 2%. The report also described economic activity and the labour market as broadly resilient despite elevated uncertainty, acknowledged tight credit conditions and a stagnant housing market, and concluded that the financial system remained sound and resilient.

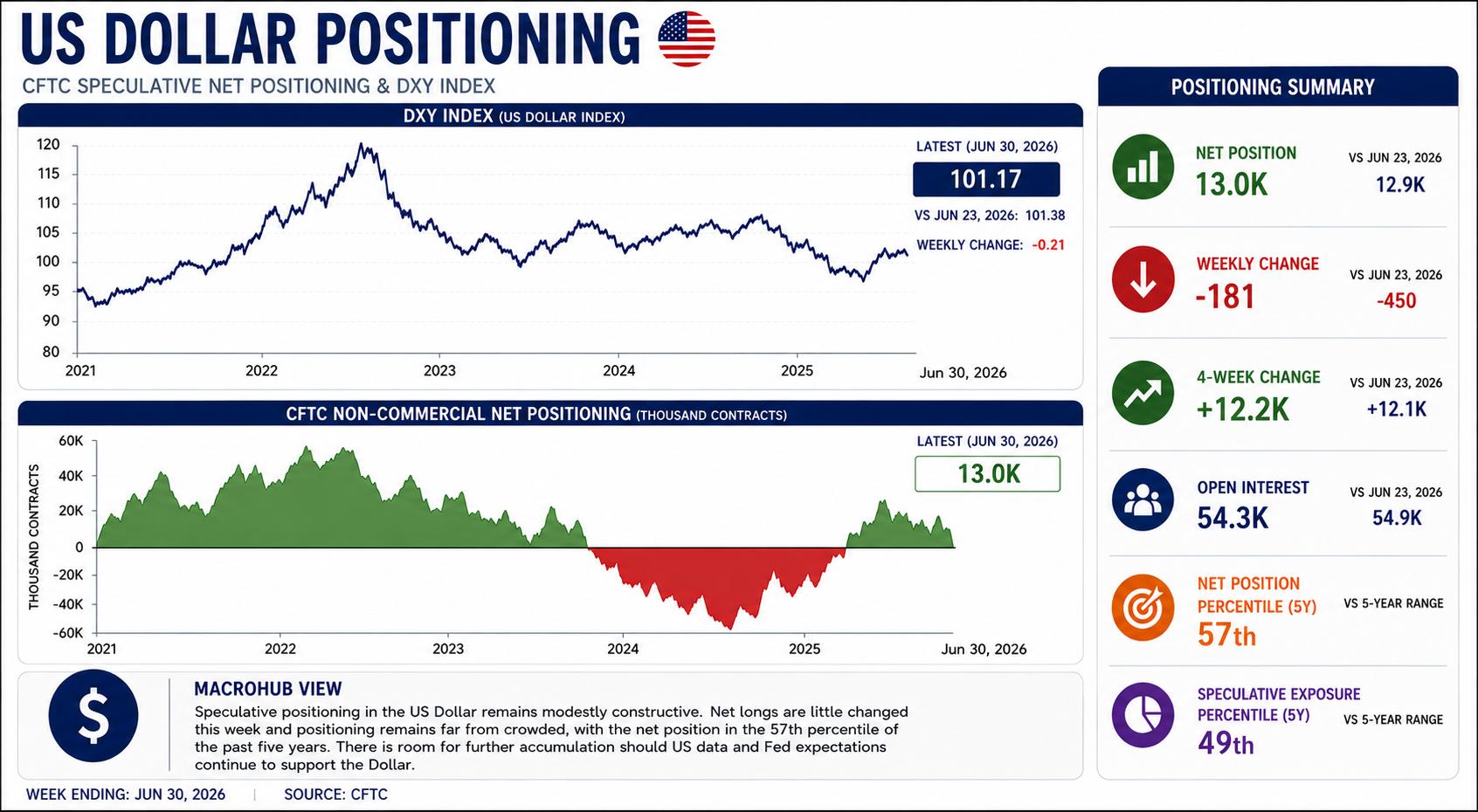

US Dollar: Positioning remains constructive as bullish momentum levels off

Speculative positioning in the US Dollar was little changed in the week to June 30, with net longs slightly higher at 13K contracts versus 12.9K last week. The latest Commodity Futures Trading Commission (CFTC) data suggests that the recent rebuilding of bullish exposure has largely run its course, with investors keeping their constructive stance rather than adding materially to Dollar longs.

Weekly positioning was basically flat, down a mere 181 contracts, while the 4-week change remained steady at just over 12.2K contracts. In addition, open interest also eased slightly to 54.3K contracts from 54.9K, indicating there was little change in overall market participation. Taken together, the figures point to a period of consolidation rather than a fresh shift in speculative sentiment.

Historical measures continue to show that the Greenback remains far from a crowded trade. The current net position ranks in the 57th percentile of its 5-year range, while the speculative exposure stands at 24%, corresponding to the 49th percentile. Both indicators suggest speculators’ positioning has recovered from the subdued levels seen earlier in the year but remains broadly in line with its historical average.

Overall, the latest CFTC data portray a market that remains modestly constructive on the buck without displaying strong conviction. Investors have rebuilt part of their bullish exposure over the past month, but recent positioning has stabilised, leaving ample room for further accumulation should incoming US economic data and Fed expectations continue to support the Dollar.

The US Dollar's dilemma: Inflation vs. employment

The US Dollar has been in the crosshairs of conflicting macro signals of late.

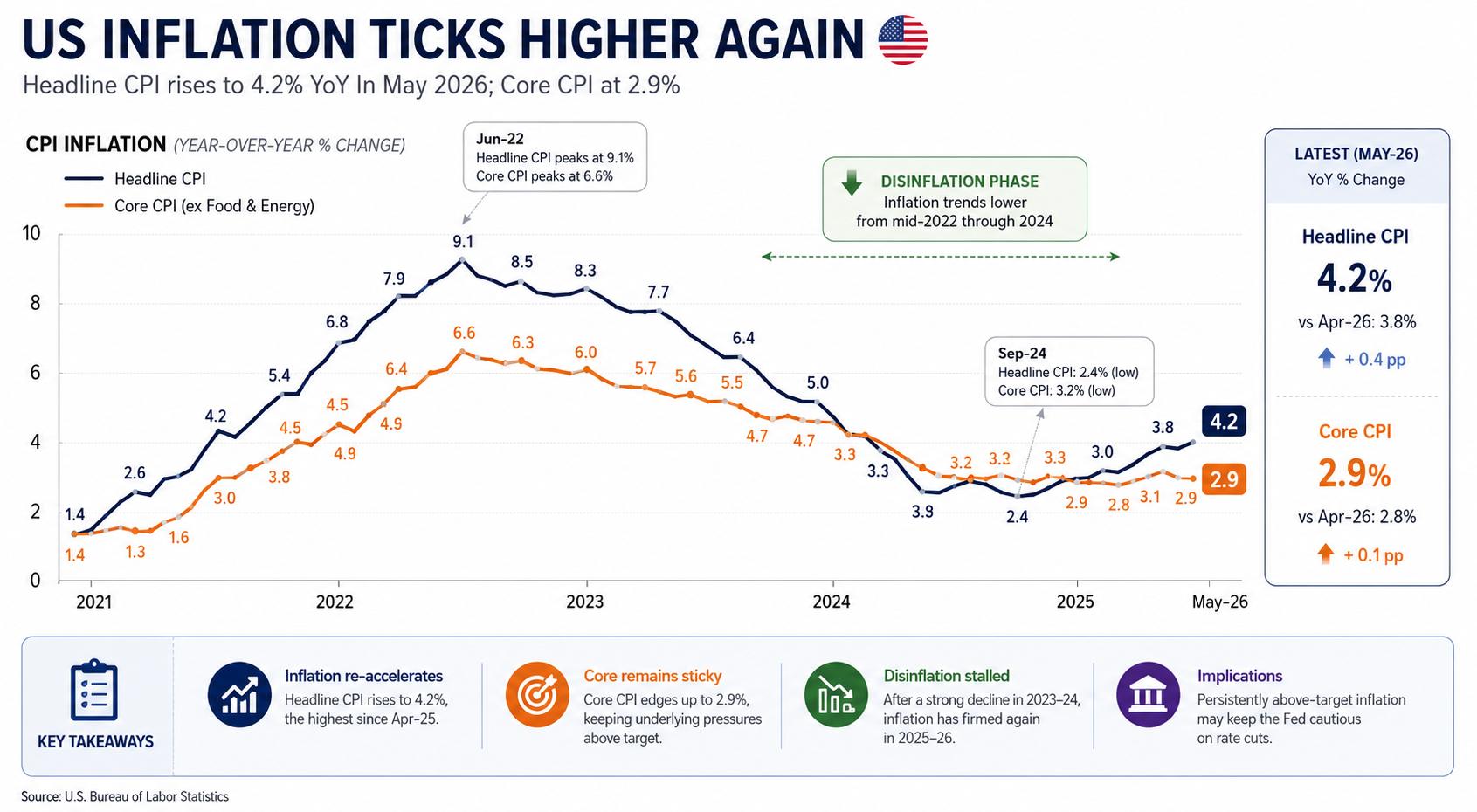

Inflation is stickier than expected: consumer prices surged in May, with headline CPI rising to 4.2% YoY from 3.8% and core inflation rising to 2.9% from 2.8%. The latest Personal Consumption Expenditures (PCE) report hammered home that point, suggesting underlying price pressures are sticky and strengthening the case for the Fed to keep policy restrictive for longer.

The Greenback has been under pressure following a disappointing June Nonfarm Payrolls report. Indeed, the US economy added just 57K jobs during the month, while the previous reading was revised down to 129K from 172K. Furthermore, the jobless rate edged lower to 4.2% from 4.3%, although the improvement appears to have been partly driven by a decline in labour-force participation.

Despite the softer labour-market data, Fed Chair Kevin Warsh has shown little inclination to shift the focus away from inflation, leaving investors to question whether the recent payroll weakness will be enough to alter the policy outlook.

More broadly, market sentiment remains cautious. Investors continue to weigh the uncertain outlook for the Middle East against the White House's still unclear strategy for resolving the conflict, while attention is increasingly turning to next Tuesday's US CPI report, which could provide the next major catalyst for both the US Dollar and expectations for Fed policy down the road.

What’s next?

Next up is the June Consumer Price Index (CPI), which could be a key factor for expectations regarding the Fed’s policy path. Investors will also be eyeing Chair Kevin Warsh’s semiannual monetary policy testimony before Congress on Tuesday and Wednesday, as well as June Retail Sales and the preliminary July University of Michigan Consumer Sentiment survey.

Besides the economic calendar, developments in the Middle East and fresh statements from Fed officials will be the main factors affecting market sentiment and the US Dollar.

The Dollar's best friend: Persistent inflation

If recent months have shown anything, it is that bringing inflation down from elevated levels is one challenge, while returning it fully to target is another altogether.

That could prove to be the US Dollar's biggest source of support in the months ahead.

Markets may have underestimated how difficult the final stage of the disinflation process was always likely to be. As long as underlying price pressures remain persistent, the prospect of interest rates staying higher for longer should continue to underpin the buck.

Employment FAQs

Labor market conditions are a key element to assess the health of an economy and thus a key driver for currency valuation. High employment, or low unemployment, has positive implications for consumer spending and thus economic growth, boosting the value of the local currency. Moreover, a very tight labor market – a situation in which there is a shortage of workers to fill open positions – can also have implications on inflation levels and thus monetary policy as low labor supply and high demand leads to higher wages.

The pace at which salaries are growing in an economy is key for policymakers. High wage growth means that households have more money to spend, usually leading to price increases in consumer goods. In contrast to more volatile sources of inflation such as energy prices, wage growth is seen as a key component of underlying and persisting inflation as salary increases are unlikely to be undone. Central banks around the world pay close attention to wage growth data when deciding on monetary policy.

The weight that each central bank assigns to labor market conditions depends on its objectives. Some central banks explicitly have mandates related to the labor market beyond controlling inflation levels. The US Federal Reserve (Fed), for example, has the dual mandate of promoting maximum employment and stable prices. Meanwhile, the European Central Bank’s (ECB) sole mandate is to keep inflation under control. Still, and despite whatever mandates they have, labor market conditions are an important factor for policymakers given its significance as a gauge of the health of the economy and their direct relationship to inflation.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.