The Fed is serious about inflation and perhaps at the expense of the labor market

Outlook: The calendar is full today, starting with the ADP forecast of private-sector jobs. Then it’s the final revision to manufacturing PMI, the ISM, and the Beige Book in the afternoon.

It’s not clear anything is going to alter the Omicron panic much, but payrolls on Friday and the ADP private-sector estimate today could have some effect. The forecast of the AFP forecast is 525,000, which would be a fall from 571,000 in Oct (before revisions).

Financial markets do not want to be sensible. They want to panic. As noted before, panic is literally physically exhausting and can’t last long. Uncertainty and fear can last a long time, though, hence our signal change in the dollar/yen and dollar/Swiss almost there, too. We have a strong warning in the peso, too. The dollar is down against the Chinese yuan on a gap.

Exhaustion from panic may stabilize FX today. Despite the OECD declaring the new variant will likely delay recovery and worsen inflation, emerging market traders think otherwise, hence the gain on the peso and some other EM currencies. At least this is an explanation offered by Reuters, although we might equally plausibly say those traders saw Omicron staying the hand of the Fed and leaving rates lower for longer. We do not have interviews with traders as in days of yore to find out.

Another questionable assertion is from ING, a big shot in the FX world, opining that “euro-dollar volatility has jumped as the Omicron variant is seen as positive for the euro (because it could slow the Fed's tightening), while Powell's remarks (suggesting inflation is the Fed's primary concern) are seen as negative for the euro.”

One of the nuances off on the side of yesterday’s noisy events was the apparent abandonment of the Fed’s employment objectives—not only low unemployment but also employment across the demographic span of the US, meaning women and minorities. But just as the Fed misjudged the supply problems and the resulting inflation, it misjudged the job market. Workers are not flooding back to their old jobs and instead choosing retirement or living on savings or starting small businesses—all the while spending like crazy on goods. As reported every month, we have an extraordinary, near-record high level of job openings—10 million. Wage increases are needed to deal with the labor shortage—and are not working yet. Quick, in what way do tapering or a rate hike change behavior to address huge consumer spending and this particular labor shortage? Answer: they don’t.

But tapering and rate hikes will influence some of the factors driving inflation, like overstocking by wholesalers and retailers alike, assuming that’s funded by debt, and capital spending. Powell said it will take some time to get back to a normal jobs market. “To get back to the great labor market we had before the pandemic we’re going to need a long expansion. To get that we’re going to need price stability.”

We like Powell. He is smart, courageous, and honest. But he doesn’t “get” the Average Joe and Josephine. It looks like many have not only saved more for a rainy day than anyone appreciated, they are also mad as hell about their former jobs and not going to take it anymore. It’s not surprising that the Fed chief cannot identify with the average citizen, but it’s conceivable some better policy decisions would derive from some inklings.

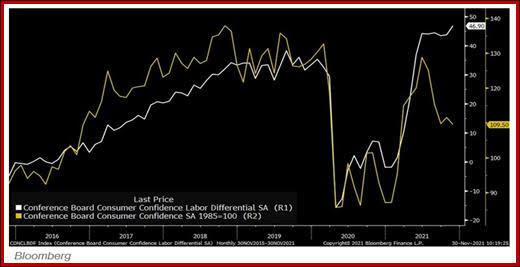

Surprisingly, the Average Joe is himself confused. The Conference Board consumer confidence index fell to a 9-month low in Nov at 109.5 from 111.6 (revised), more than the Bloomberg forecast. But more interesting is the detail that respondents see the job market as excellent (and actually at an all-time high) at the same time they see the economy faltering. See the chart. Bloomberg blames inflation for the divergence, especially in gasoline and food. This is parallel to the political polls showing Pres Biden’s approval ratings tanking despite getting the $1 trillion infrastructure bill.

Bottom line, here’s our take—the Fed is serious about inflation and perhaps at the expense of the labor market. Inflation comes first. Only if the Omicron variant is more lethal and requires shutdowns and other drastic measures will the Fed back off from accelerating tapering and an early hike. It may take a few weeks for this to become clear and it depends, of course, on what the scientists learn about the variant. We would not be in a hurry to dump the dollar (or equities). We can get a Santa Claus rally in both.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat