The expectation of rate hike in June 'a no-brainer', says RBI Governor

USDINR 77.55 ▲ 0.05%.

EUR/USD 1.0671 ▼ 0.17%.

GBP/USD 1.2563 ▼ 0.19%.

India 10-Year Bond Yield 7.365 ▼ 0.28%.

US 10-Year Bond Yield 2.841 ▼ 0.64%.

ADXY 103.69 ▼ 0.13%.

Brent Oil 110.19 ▼ 0.53%.

Gold 1,853.58 ▲ 0.31%.

NIFTY 50 16,249.45 ▲ 0.21%.

Global developments

China announced a raft of fiscal measures to support the economy battered by the Zero COVID policy. These include postponing social security payments and loan repayments, broadening tax credit rebates, and undertaking new investment projects. Total tax relief amounts to USD 21bn.

ECB president Christine Lagarde said ECB is likely to raise deposit rates out of the negative territory by September end and could raise it further if it sees inflation stabilizing at 2%

President Biden on his Asia visit yesterday said the US would intervene militarily if China invaded Taiwan. The White House later downplayed the comments. This has not impacted risk much but China-Taiwan is a sensitive topic from a geopolitical point of view and one needs to keep it on the radar. Biden also said he would review the tariffs imposed by Trump on Chinese goods. This fuelled a rally in the Yuan.

Price action across assets

Euro has strengthened post-Lagarde's comments. Meaningful downside momentum would only build upon a break below 1.0480 now. US yields are up 4-5bps across the curve with a 10y yield at 2.85%. The Dollar has strengthened a bit in the early Asia session. US equities saw a pullback with S&P500 gaining 1.9%. Asian equities are a mixed bag. Crude prices have come off a bit with Brent now at USD 112.5 per barrel.

India’s fiscal deficit likely to shoot up to 6.9%: Barclays:.

Domestic developments

RBI governor in an interview yesterday said a rate hike in the next policy was a given. He also said the government may not have to resort to additional borrowing to fund the excise duty cuts on fuel. He added that the RBI would not allow runaway depreciation of the Rupee.

USD/INR

The Rupee strengthened yesterday on the RBI governor's comments that the RBI would not allow runaway depreciation of the Rupee. The rupee ended the session at 77.53. Vols came off with 3m implied volatility dropping 13bps to 6.25%. 1y forward yield inched by 2bps to 3.84%.

Bonds and rates

Bonds sold off as fuel tax cut was seen as adding to the fiscal burden. The yield on the benchmark 10y ended 7bps higher at 7.39%. Rates had rallied initially but gave up gains towards the end with 5y OIS ending at 7.01%.

Equities

Nifty gave up intraday gains to end 0.3% lower at 16214. While Auto stocks were the best performers on fuel tax cuts, Metal stocks sold off on account of the export duty levy on certain steel products.

Strategy

Exporters are advised to cover on upticks towards 77.90. Importers are suggested to cover on dips towards 76.50. The 3M range for USDINR is 75.50–78.30 and the 6M range is 75.00–78.90.

Oil settles nearly flat; recession worry vies with higher demand outlook.

FX outlook of the day

USD/INR (Spot: 77.60)

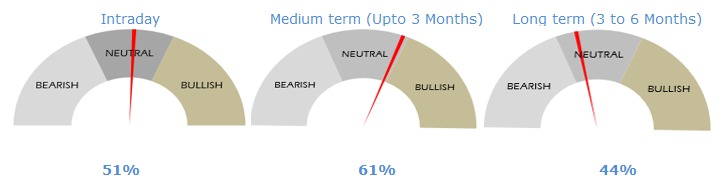

The Indian rupee strengthened yesterday on the RBI governor's comments that the RBI would not allow runaway depreciation of the Rupee. The rupee ended the previous session at 77.53. RBI governor in an interview yesterday said a rate hike in the next policy was a given. He also said the government may not have to resort to additional borrowing to fund the excise duty cuts on fuel. The Dollar has strengthened a bit in the early Asia session. The pair is expected to trade with a neutral to bullish bias on the back of global uncertainty and a broadly stronger dollar. The intraday range of the pair is expected the remain within 77.50-77.80.

EUR/USD (Spot: 1.0667)

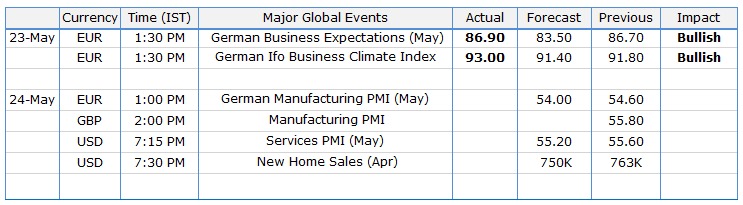

The EURUSD pair gained momentum at the start of the week and ended yesterday's trading around 1.0680. The US dollar remained weak as stocks advanced, despite concerns about inflation and growth remain the same. ECB President, Lagarde said she expects the facilities program to end “very early” in the third quarter of the year, leaving policymakers in a position to exit negative interest rates by the end of the quarter. Also, this would allow a rate hike to take place in July, in line with forward guidance. Macroeconomic data further supported the pair, the German Ifo Business Climate improved to 93 against the market expectation of 91.4. Today, the Purchase Managers Index (PMI) numbers will be released for Germany, Eurozone, and US. The pair is expected to trade in the range of 1.0620 to 1.0720

GBP/USD (Spot: 1.2560)

The British pound is extending its recovery after posting its first weekly gain in five and begins the beginning week on a positive note. In yesterday's speech, Bank of England’s (BoE) Governor Andrew Bailey sounded very “hawkish” aligned with most MPC members. He said that the central bank is ready to hike rates if needed and added that policymakers can and “must” take actions needed to return inflation to target over a period that avoids unnecessary volatility. Bailey said he rejected the argument that the BoE’s response let demand out of hand, thus stoking inflation. Investors are awaiting the release of the PMI numbers from the UK and the US. The pair is expected to trade in the range of 1.2470 to 1.2590

USD/JPY (Spot: 127.78)

The USDJPY pair witnessed some selling at the start of the week, though managed to find some support ahead of the monthly low, around the 127.00 mark touched last Thursday. The pair remained on the defensive through the day and ended trading near 127.80. The risk-on sentiment was supported after US President Joe Biden said he would consider trimming Chinese tariffs imposed by the previous administration, as it would reduce tax pressures and hence, help to tame inflation. The Quad Summit in Tokyo and the US PMIs for May, as well as a speech from Fed Chairman Jerome Powell, will remain in limelight. The pair is expected to trade in the range of 127.50 to 128.30

Eurozone plans fiscal policy shift from supportive to neutral.

Economic calendar

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.