The eurozone 10 years after

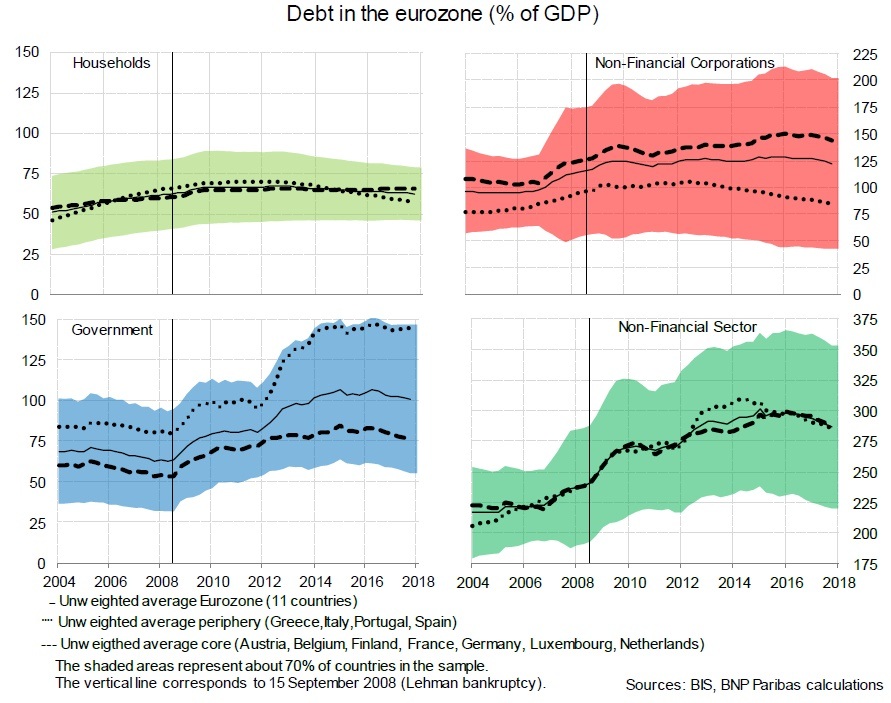

In the run-up to the financial crisis, low interest rates had stimulated real estate investment and economic activity, in particular in the periphery countries. Household debt increased rapidly and housing bubbles emerged. The Lehman Brothers bankruptcy made an abrupt end to the buoyancy. Property bubbles burst and bank lending dried up. Government debt increased rapidly because of automatic stabilisers, fiscal stimulus packages and support to the financial sector.

Ten years later, indebtedness of the non-financial sector in the core and the periphery countries is virtually the same, although substantially higher than before the crisis. The mix is quite different though. In the core countries, government, household and non-financial corporations have all increased their indebtedness as low interest rates make borrowing attractive. The periphery has seen deleveraging by households and non-financial corporations but government debt has risen very significantly. This increases the sensitivity of public finances to the cycle and bond yields.

Author

Raymond Van Der Putten

BNP Paribas

Expert in Japan, Australia, New Zealand, Benelux, Pensions and Long Term Forecasts.