US is still feeling its way toward normalization

Outlook:

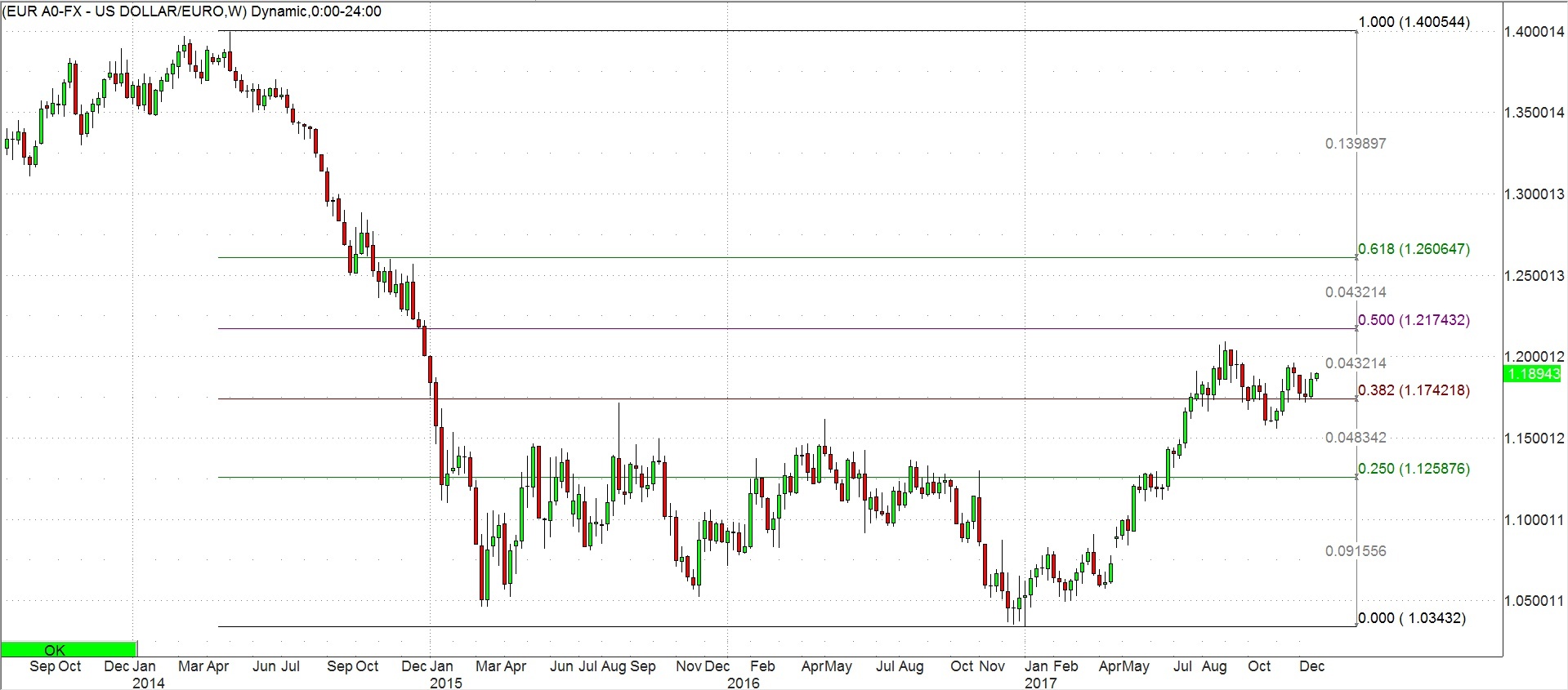

As the FT reports, the euro looks set to be the big G10 currency winner of 2017, up more than 12% against the dollar. Let's have a little perspective, please. On the weekly chart below, the euro is seen as not having recovered even half of what it lost from the high of 1.3993 in May 2014 to 1.0340 in Jan 2017. The big one-way move was from the high to 1.0459 in March 2015. In other words, the euro fell for almost a full year, recovered a little and then put in an even lower low before the current recovery. It spent most of 2015 and 2016 range-trading and now that the recent up-move has been disrupted, it can go back to range-trading for a prolonged period.

Besides, a euro recovery is probably not what the ECB wants. Recall that over the past year, we heard mutterings and rumblings from mostly unnamed ECB board members about a too-strong euro damaging the recovery. They might start complaining more loudly if the economic recovery accelerates to the point where inflation rears its ugly head. Then the ECB will have to follow its own rules and mandate, and accelerate exit from QE. Draghi has said rates are not on the table for discussion until the buying pro-gram is ended, but ending it could come sooner than he thinks. Or the ECB can keep the buying program and keep short-term rates off the table, but central bank influence over the longer end of the yield curve is, and always has been, less powerful.

The US is still feeling its way toward normalization. Nobody has ever done it before, so the ECB was hoping to be able to copy the US, and avoid whatever mistakes the Fed makes. But the BoE, Fed and ECB (if not the BoJ just yet) are facing bond markets that can develop a mind of their own, as the WSJ puts it. And "If longer-term rates suddenly rose, that could throw cold water on stock markets that have been hitting repeated new highs."

The WSJ notes that a new study by the Bank for International Settlements covering data from 18 coun-tries from 1870 finds "no clear link between rates and factors like demographics and productivity—it is mostly central-bank policy that matters." Rates can still creep up on investors when central banks raise rates solely to contain optimism. "Central banks in Canada, Sweden, Norway and Thailand are thinking along these lines, analysts said. The point is that central banks can raise rates to squash bubbles instead of trying to fine-tune inflation.

Well, no. Remember that former Fed chairman Greenspan said nobody can identify a bubble until it has burst. This was his reasoning behind not raising margin requirements for any sector. Raising margin requirements for individuals but not institutions would be unfair, and vice versa, too. It's not the job of the central bank to protect speculators from their own worst impulses.

We don't buy into the idea that the Fed or any other central bank would put the cart before the horse, i.e., raise rates solely or mostly to restrain equity or commodity market bubbles. If there is going to be an unexpected data set that sets central bank teeth on edge, it will be inflation, the central focus all along. Asset price inflation is not in that mix. It's price inflation for goods and services that counts, es-pecially the kind that affects households.

As we just saw in Japan, a surge in household spending by 1.7% was accompanied by a rise in inflation to 0.9% in the core measure. Meanwhile, the unemployment rate fell to 2.7%, the smallest in 24 years, although wage growth remains sluggish at only 2.1%.

Sound familiar? The US has the same conditions—low inflation, tight labor markets but weirdly, low wage growth. Unless new Fed chairman Powell choses U6 for the unemployment rate or makes some other change in the Fed's data matrix, we have to expect rampant household spending to push inflation upward. And we can complain again about the Fed disregarding two key factors, the price of food and the price of oil. By centering on the core inflation concept, the Fed and other central banks disregard the real conditions facing real households. If the Fed were magically to start looking at things like the savings rate (down to barely 3.2%), it would deduce that higher rates are for the greater good of the greater number, if only to induce savings and prevent spending like there's no tomorrow, which is what we are seeing this holiday season.

In a phrase, the Fed is out of touch with regular households, the very constituency it is supposedly pro-tecting.

If the dollar rise persists, as the consensus has it, imported inflation is on the way. Powell doesn't take over until Feb 3, but we are wondering if a sea-change at the Fed will not become the shiny new thing the market will worry about.

Tidbits: The holiday fun tidbits are a reprieve from thinking about N. Korea and central bank mindsets. In the UK, the press will be agog from now to the May wedding of Prince Harry and the American Meagan Markle, who is half-black. Wouldn't it be fun if the Palace invited Obama but not Trump? In the US, Trump is charging extra for Mar-a-Lago members to attend the New Year's Eve party. By dou-bling the membership fees upon getting elected, Trump made an estimated $7 million. Vulgar profiteer-ing from the office is disgusting but not illegal. For the emoluments clause to kick in, profiting has to derive from foreign governments (like White House staffers pressuring foreign governments to hold meetings and conferences at the Trump hotels and golf clubs).

The NYT has a lengthy article on the five thousand rules imposed by federal and state governments, not to mention retail stores, on an apple producer in upstate New York. Rules pertain to worker safety, cleanliness, pesticides and other contaminants, and on and on. False eyelashes are banned, along with chewing gum. It seems obvious that regulatory overkill is at work, and yet elsewhere, the Trump gang is allowing vast and serious pollution by oil, gas and minerals mining as well as opening up millions of acres of formerly forever-wild federal land to private gougers. The latest is rolling back offshore drill-ing rules, including worker safety rules. This is an Exxon Valdez in the making. You'd think an ad-vanced society could come to a saner mix of regulatory burdens.

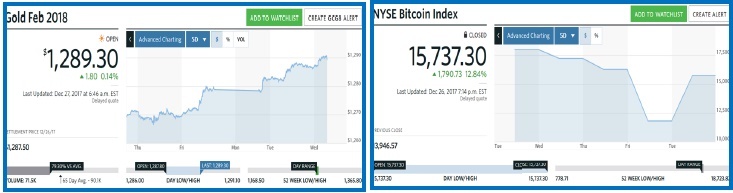

The FT reports that on Monday, bitcoin took a big hit "when the Israeli Securities Agency said it would bar companies trading in bitcoin from operating on the Tel Aviv stock exchange and investigate how to regulate the digital currency because of concerns about volatile prices. Yet bitcoin rallied sharply on Tuesday, and was hanging on to its gains on Wednesday morning, trading around $15,947 according to composite prices compiled by Bloomberg.

"The price of the cryptocurrency remains below its mid-December peak of nearly $19,666, but its rapid ascent since the start of the year when it was worth just $1,000 has alarmed regulators and financiers who fear the market shows all the signs of overheating."

The chief of the Isreali agency said "I think it looks like a bubble, smells like a bubble, acts like a bub-ble and feels like a bubble." Citibank agrees, naming "poor design" and wondering if government ac-tion itself could trigger a burst bubble. When Mt. Gox was hacked, investors lost an about $450,000, inviting interest from governments. The US has warned investors to be cautious and China had already closed bitcoin exchanges and banned initial coin offerings in September. The FT names big-shots who promote crypto-currencies. Do you take financial advice from Paris Hilton?

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat