The ECB: Under pressure

Judging by the recent data, the acronym PEPP that was introduced last year when the ECB launched its Pandemic Emergency Purchase Programme, could also be seen as a reference to the pandemic’s exceptional price pressures. The upcoming governing council meeting and the new staff projections are eagerly awaited. Whether PEPP will be prolonged beyond March 2022 ultimately depends on the inflation data. It seems likely that the ECB will postpone its decision until after the summer in order to have a better view of the inflation outlook.

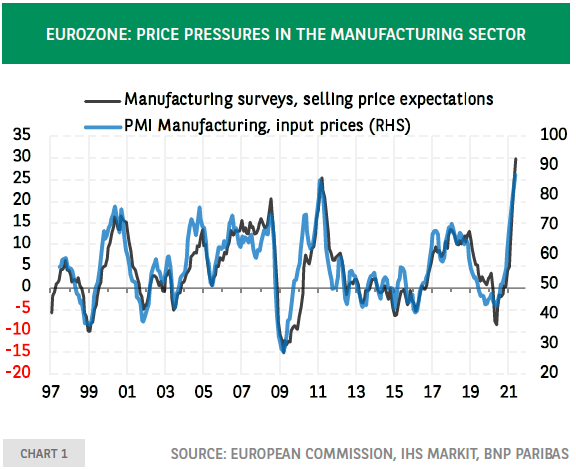

Judging by the recent economic data, the acronym PEPP that was introduced last year by the ECB when it launched its Pandemic Emergency Purchase Programme, could also be seen as a reference to the pandemic’s exceptional price pressures. Inflationary tensions have been rising as reflected in survey data on input prices and selling price expectations (chart 1). They are exceptional in terms of intensity – at least in manufacturing where they are at record highs- but also by their a-typical nature, due to the lifting of restrictions weighing on supply and demand.

The ECB is caught in the middle between the official meaning of PEPP and the alternative reading. The end date of March 2022 that has been set for the emergency asset purchases is slowly getting closer, forcing the ECB to provide guidance on its intentions, whereas rising price pressures create a perception that an extension is becoming less likely.

Prolonging the PEPP would send a signal that the ECB is convinced that the transmission of higher price expectations in the inflation numbers will be temporary and limited. Against this background, the upcoming governing council meeting and the new staff projections that will be published on the occasion, are eagerly awaited. On the latter, one would expect an increase in the inflation forecast for this year, much like the consensus forecast which has also been moving higher in recent months (chart 2). In March, the Bloomberg consensus expectation for average inflation this year was 1.5%. This moved to 1.6% in April and 1.7% in May. Importantly, the forecast for next year hardly moved (1.2% in March, 1.3% in April and May).

This is not very different from the recent forecasts of international institutions. According to its latest forecasts, the OECD expects inflation to reach 1.8% this year and 1.3% next year, which is in line with the European Commission’s forecast of respectively 1.7% and 1.3%. Judging by next year’s forecasts, which are far below the ECB’s objective, maintaining a highly accommodative monetary policy stance seems warranted, so the question is more about the mix of tools to be used rather than whether the overall orientation should change. The key debate is on what happens to the PEPP. Introduced to address the economic consequences of the Covid-19 shock, its flexibility has been used earlier this year to fight the tightening of financial conditions. The accelerated pace of purchases which was announced following the March governing council meeting has been successful, judging by the easing of financial conditions (chart 3). In the meantime, survey data show that confidence of the main economic sectors – industry, services, construction, trade – and amongst households has improved, sometimes significantly so. This would justify having a debate at the next meeting about extending the PEPP beyond March 2022 or replacing it with an increase in the traditional asset purchase programme. Such a substitution would be necessary to avoid a cliff-edge impact on bond markets and has been hinted at in the ECB’s introductory statement.

Whether this discussion will already take place is not a foregone conclusion. The governing council might prefer to have more data and have the discussion and decision after the summer. In a recent interview, Isabel Schnabel, a member of the executive board of the ECB, explains that the decision on PEPP will depend on the joint assessment of financing conditions and the inflation projection. The latter is the “ultimate yardstick” considering that “PEPP aims to offset the negative impact of the pandemic on the inflation outlook.” She considers that “we are not seeing this yet”. Investors will be keen to understand how this impact will be determined. A simple counterfactual analysis which consists of comparing the December 2019 Eurosystem projection for inflation in 2022 (1.6%) with the March 2021 projection for inflation in 2022 (1.2%) shows there is still a considerable gap. It is unlikely that this would narrow significantly in the new projection so for a decision on PEPP we will probably have to wait until after the summer.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.