The Daily Fix - Trader thoughts on the session

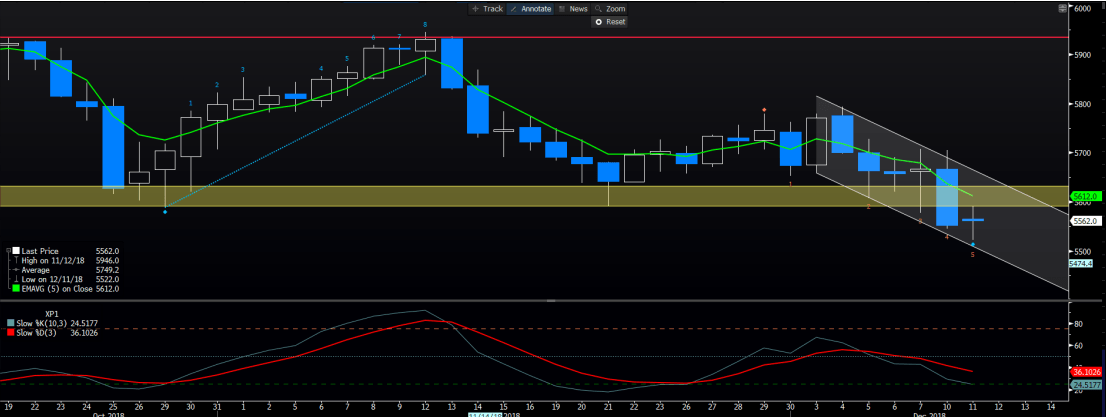

We’ve seen some signs of stability return to Asian equities after yesterdays dump and exodus to cash. That said, we are by no means out of the woods, and as we can see from Aussie SPI futures daily, the bulls have tried to push the index into the former floor of 5600 and failed miserably. What was support, is now resistance, and that seems to have been confirmed today even if there is some indecision in the price action.

(Source: Bloomberg)

The Aussie futures index needs to close back above the 5-day EMA (currently 5612), or the trend lower will play instead of the seasonal rally, and we could be looking at something far more sinister. Active managers will be hesitant to chase performance and step in front what is such an ugly market if they are in-line with their benchmark. Even if the ASX 200 cash index is trading on a consensus 12-month P/E of 13.9x, which is the lowest valuation since 2014 – where the obvious concern is that few trust the earnings side of the equation.

We see broader Asian markets stable, although S&P 500 futures are down 0.4% and that requires attention. Predominately, because if we look at price action in the S&P 500 cash index, we can see the bid that came in the market resulting in a bullish hammer candle, off strong horizontal support. Therefore, follow-through buying in the session ahead and we could see a rebound into 2708 and Fridays high. Of course, if the S&P futures move is an indication, we could be facing a weaker open and as such a close through 2628 (in the S&P 500 cash) will accelerate the selling and this will be the natural catalyst for the Aussie index to build on the developing bearish trend. The battle lines are drawn.

-636801001249547757.png)

We continue to watch crude closely, where US crude is oscillating around the 200-week MA (52.19), although the buyers are supporting at $50.66 (the 50% retracement of the 195% rally seen between 2015 to 2018). A weekly close through here and I am targeting $44.85, which would have further implications for inflation expectations and interest rate pricing. The daily chart of US crude shows consolidation between $49.41 and $54.50, with sellers fading moves into the October downtrend. The market still needs to see firm detail around the exact allocation of the announced production cuts, and of course, garner a belief that the quotas will be adhered to. It feels as though the price will chop around, but a weekly through $50.66 should be respected.

There has been such a focus on the repricing of the US and global interest rate expectations and rightly so. One dynamic getting focus here has been the lack of sustained USD selling despite US rate expectations for 2019 falling to just 18 basis points (effectively 72% chance of one hike) from 54bp on 8 November. This is true of the USD index, where the USD bears have little incentive to move out of USDs and into other G10 currencies. As a trade, I like the USD index in a range of 97.43 to 96.32, at least, until we see the US core CPI data tomorrow night (00:30aedt) and depending on the outcome relative to consensus (+2.2%). USDJPY has found sellers today, which is why we see small weakness in the Nikkei 225, with the 113-handle coming into the play. I had sell orders into ¥114, which has been the level to fade USDJPY since October, but I won’t be chasing the market here. Support is seen at ¥112.31 (20 November low), so I would expect this to be an obvious place to see stops.

(Top pane - US rate pricing in 2019 vs USD index, lower pane - US rate pricing in 2019 vs USDJPY)

-636801001804740551.png)

EURUSD tried to push through the 29 November high of 1.1402, and while we saw a session high print of 1.1443, the pair failed to close above this level. I continue to focus on a close through 1.1402, and subsequently 1.1456, before turning truly bullish on EURUSD and as things stand it seems like the Bollinger Bands should contain moves. So, on the session I would be looking at playing a range of 1.1436 to 1.1285 – this fits well with EURUSD overnight implied volatility, which suggests a 60-point move on the session.

Ahead of tomorrow’s ECB meeting (23:45aedt), we get German ZEW survey expectations (21:00aedt), and the market expects further deterioration in both the current situation (consensus sits at 55) and expectation sub-survey (-25). Expect the EUR to be sensitive to this, as they will the EU PMI series on Thursday.

AUDUSD saw good buying, trading from 0.7185 into 0.7208, and again off the 55-day MA (0.7184), which has contained sell-offs through the last few weeks. This medium-term average was also a good guide on where to sell the AUD from March until November. The focus today has been on NAB business confidence, which declined a touch in November, and more prominently on the Q3 house price index which has fallen slightly-less- than-feared at 1.9%. Although that said, the push higher in AUDUSD materialised some 45 minutes after the Aussie data was released, so it’s hard to attribute the move to that and wasn’t driven from domestic factors, and more about algo’s tracking the USDCNH cross. Tell me where USDCNH is going to trade in the next 48 hours and I’ll be fairly confident in telling you where AUDUSD will be headed.

-636801002398476119.png)

That leaves GBP, as we are seeing small buyers in GBPUSD after yesterdays break of the YTD low of $1.2662. Once again, the headline risk has scared anyone from being long GBP with any conviction, even if we take the view that the GBP is already partially pricing a no-deal Brexit. In the options market, we can see one-month risk reversals largely unchanged despite the move to 1.2507. Implied volatility did push a higher on news of the delayed vote, with the implied move over the coming month sat at 425-points (in either direction).

The delay in the vote through the Commons hasn’t achieved anything other than delay the evitable - that being, as long as the backstop is a core component of any deal, it will be voted down. Both the EU and UK should spend this week’s EU Summit talking more intently about how to navigate a no deal or hard Brexit in March. This saga has been painful, and I have deep sympathy for those living this in the UK, but there are more twists and turns to come, and as each day goes on, the prospect of the worst possible outcome grows every more likely – although that is the theatre of politics.

Author

Chris Weston

Pepperstone

Chris Weston recently joined Pepperstone as Head of Research.