Triple whammy for the US Dollar

Outlook:

The US economy was thrown off the cliff by an impulsive Trump imposing tariffs on Mexico with no advance notice. Nerves were already stretched thin by the China trade war, which is heating up in some odd ways (China warned against travel to the US because of gun violence and Chinese students in the US facing harassment).

A great deal of the negative response comes from that lack of advance notice, as noted by St. Louis Fed Bullard yesterday. It’s as close to a Fed rebuke of a sitting president as you can get and we do not recall ever seeing such a thing before. Everyone wonders whether this first mention of a cut will be echoed by NY Fed Williams and Gov Brainard later today at a Fed conference. Fed chair Powell speaks at the same conference. The Fed has an unwritten rule that each Gov can speak for himself. Powell may warn the others on the sidelines that too overt and obvious a poke at Trump threatens their jobs.

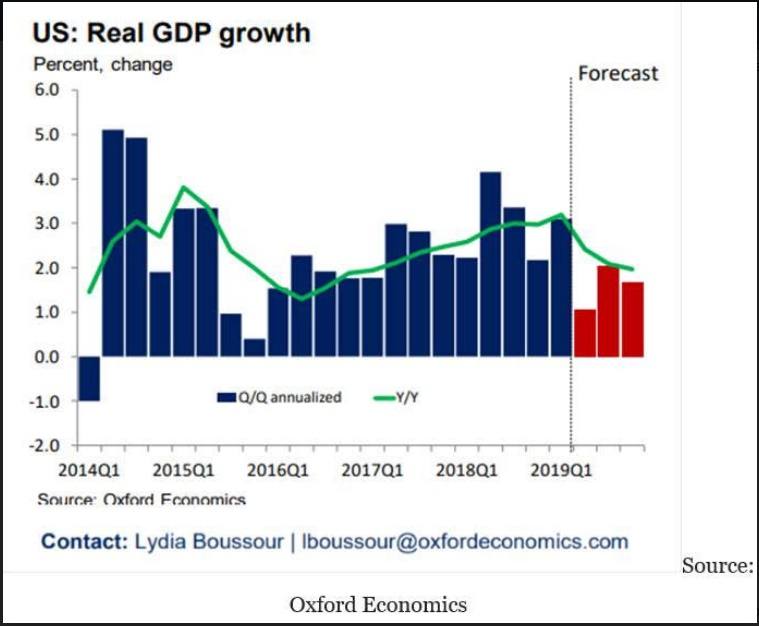

The fallout comes from all directions. We were already expecting slower growth but now the forecasters are out in force projecting conditions even worse than we thought. See the Oxford Economics chart below from The Daily Shot. Growth could be only 1-1.25%, led down by inventory drawdown, lousy business investment and weaker export growth. Export growth will be weaker because countries that buy US goods will be poorer from not being able to sell into the US (not to mention a too-strong dollar).

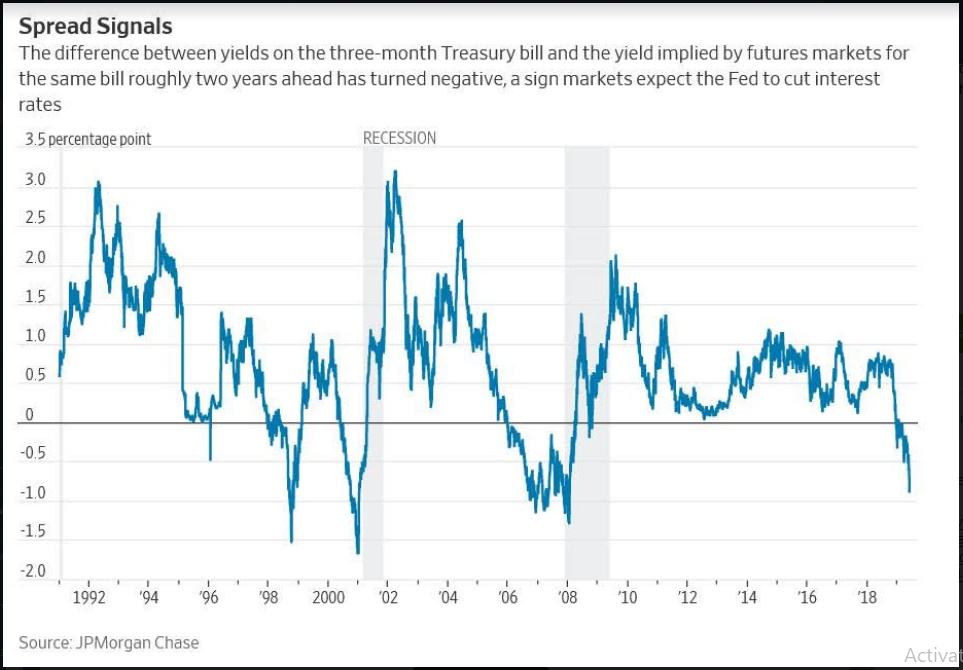

Fallout shows up in bond yields, too. The weaker dollar is due not so much to the 10-year falling to 2.10% from 2.45% only a month ago as to the Bund falling, as well, but by fewer points. You’d think positive would beat negative every time, but no so—the contracting yield advantage is movement, and traders watch movement. Then there is the Fed funds futures pointing to two cuts and the inverting yield curve, a triple whammy for the dollar.

And at the same time, as Bloomberg colorfully points out, Fed funds futures “Priced in a Whole Extra Cut in Just Two Days.” The current Fed funds rate is 2.40% and the January contract is at an implied yield of about 1.72%. “The implied yield on the same contract was more than 28 basis points higher on Thursday, before U.S. President Donald Trump’s tariff threats against Mexico and broader concerns about riskier assets roiled markets.” In other words, everyone including the Fed blames Trump. “Historically, the Federal Reserve has often moved in increments of 25 basis points, meaning that the market is now pricing in one more standard-sized cut than it was less than a week ago. Volumes on the contract have also increased in recent days.”

For its part, the WSJ reports economists at Barclays expect one cut in Sept by 50 bp and another cut in Dec by 25 bp for a total of 75 bp. This is a sea-change from no cuts at all. JP Morgan Chase sees 25 bp in both Sept and Dec. Morgan Stanley see a recession within three quarters if trade tensions persist. Sure enough, “Bond markets are signaling they expect the economy to slow more sharply than previously anticipated, with rising risks of a recession. Yields on long-term Treasurys have fallen below yields on Treasurys with shorter durations, a so called inversion of the yield curve that has often preceded interest-rate cuts and recession.”

But the WSJ asserts “most forecasters don’t see the Fed taking action at its June 18-19 meeting, in part because they expect the central bank will want to see if global leaders can ease trade tensions, particularly at the G-20 summit in Japan later this month.”

Okay, let’s keep calm and inject a little perspective here. The Fed funds market is overreacting to the comments of the Vice Chair Clarida (maybe, possibly) and St. Louis Fed Bullard (uncertainty will be long-lasting). Each Fed can speak his own mind. Yellen was the straightest of straight shooters when she was at the San Francisco Fed, but whole markets didn’t’ turn on a dime on her remarks (even though she was invariably right). Bullard is a single opinion. For all we know, we will get the opposite view at the Fed conference today (comments by three Feds, including Powell).

It’s important to remember that the Fed is behind the curve so much because it acts on hard data, not on Fed funds futures or any other signal the famously flighty market delivers. The Fed funds futures may be correct, but the implied probablities are not a Fed factor. Don’t forget we will have payrolls in a few days. The number is going to be consistent with the past several years—low unemployment. We said yesterday that Powell is a decent Fed chairman because he seems to be more responsive to sentiment in the market as expressed by some of these measures, but he is not a slave to them. Markets are wrong, a lot. There’s that old Samuelson quip about the inverted yield curve predicting 37 of the last three recessions. The Fed has to be independent of both the flighty market players and the political establishment, including the president.

That leads to another idea—that Bullard is wrong that rising uncertainty is here to stay. What is certain is that Trump will inject new shocks in a more or less continuous stream. He’s erratic. He’s impulsive. He doesn’t have a plan but operates on gut instinct. The Fed knows as well as anyone that Trump’s gut instinct led him into excellent investment opportunities (e.g. casinos) that he then botched and mismanaged into bankruptcy. Here’s the point—the markets can adapt to ever-increasing uncertainty. That’s one of the big points about markets—they are adaptive.

This is not to say the changes Trump is bringing down on everyone’s head are not horrendous. The economy will indeed go downhill to a growth rate of 1-2% and flirt with recession. The Fed will cut rates but probably only once and probably later. We had thought July but now that the Fed needs to rein in hysteria, we’ll move our forecast to September. But it’s true that the China trade war (too quiet!) and the Mexico trade war are destructive, even if they get dialed back (and Trump pretends he intended to dial them back all along).

The fallout on tariffs going as high as 25% on everything Mexican could be nuclear. See the chart from Statistica—the US imports more cars from Mexico than anywhere else. We just had to know what car we import from Finland—Finland? You learn something new all the time. “In manufacturing, Valmet Automotive’s customer references include Mercedes-Benz, Porsche, Ford, Saab, Opel and Fisker. Valmet Automotive has had electric vehicles in series production since 2009.”

As for the dollar, if the Fed reins in hysteria as we expect and Trump reins in the worst of the trade war aspects, the dollar comes back. Positive beats negative in the end.

Tidbit: One idea—and likely an unrealistic one—is whether a revival of American manufacturing could goose growth. This is the ideal outcome inherent in much of Trump’s tariff stories. Somewhere economists are working on whether this is even remotely possible. We have mostly considered the idea a classic uneducated, uninformed Trumpian pipe-dream.

Can US industries gutted by foreign competition come back, and if they can come back, how long does that take and how much does it cost? We have not seen this question posed in public, presumably because once an industry has moved overseas to take advantage of cheaper labor, historically, it never comes back. Domestic labor does not gets cheaper—wages are “sticky” downward.

Ah, but labor is not the only input. The auto industry may well become the poster child for restoring an industry. Or rather, it might be if Trump were to win re-election. The 518 days left in his term are probably not enough. To figure out whether any part of the auto industry can return to US shores, we found a dandy table at the WSJ that breaks out sales and share of total market by the top 20 manufacturers. It would take all day and all night to analyze this data (which is pretty interesting), but here are a few facts: GM’s imports of cars fell 67.4% from March 2017 to March 2018. Ford and Chrysler show no imported cars at all. Toyota’s sales of imports fell 6.5%. Honda’s imports fell 36.2%.

How many US cars are imports? Hard to say because of that intricate supply chain… but in 2016, American University writes that of the 17.5 million vehicles sold in the US, approximately 65% were produced in the United States. The University creates a “Made in America Index” that judges the domestic content of vehicles sold in the US. Criteria include where is the labor and the R&D location.

We couldn’t access the index itself, but never mind. The point is that at some price, the US can recapture a big chunk of the auto industry. In fact, it’s already happening. The American Auto Council writes that sales of imported cars were already on the ropes a year ago. Secondly, the top US producers—albeit with many imported parts—have been coming back since 2009. “While FCA US, Ford and General Motors are just three of the sixteen automakers competing in the U.S., they produce more than 54 percent of all of the automobiles assembled in this country; they purchase nearly two thirds of the auto parts manufactured here as well. …The total U.S. production in the automobile industry has been on an upward trend since the end of the financial crisis of 2009. This charge has been led by FCA US, Ford, and General Motors – the largest automotive manufacturers in the United States”).

It's no doubt too late for socks and sheets and other low-wage manufactured goods, but maybe the day can come when you can buy a refrigerator made in the US. The question remains: how long does it take and what does it cost? The auto industry has become a lot more nimble in recent years, so let’s say 2-4 years. And what does it cost? Ask Detroit. They will be glad to tell Washington how big a handout they would like. Theories like this are the stuff of the Swamp. But just wait—you are sure to hear this idea take hold any minute now. Trump has to offer something to counter Joe Biden’s deep support in the unions.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat