The chains that bind: No relief for inflation until supply constraintsease

Summary

Supply chain problems are more severe and taking longer to work out than initiallyanticipated, causing the “transitory” factors that are bidding up inflation to last longer. This second installment in our The Chains That Bind series discusses how persistent supplypressures not only will keep inflation higher for longer but also have the potential to stoke inflation that is not so transitory.

No relief for inflation until supply constraints ease

The Delta variant is on the rise, and we are not turning a blind eye to rising COVID casecounts or of the belief that the pandemic is over. That said, inflation has edged out COVID as the predominant concern among financial markets, businesses and householdsfor the better part of this year. At this particular moment when the global economy iscoming back online, you cannot discuss inflation without understanding how supply chainproblems have precipitated or at least exacerbated these inflation dynamics.

In January when we discussed supply-side risks to inflation, we noted that bottlenecksand shortages would generate higher cost pressures temporarily, but upward pressureshould subside as businesses continue to adjust to the environment, demand growthcools and staffng challenges ease. We stand by this line of thinking six months later andnote this is essentially what the Fed has in mind when it characterizes current inflation as“transitory.” The rub, however, is that supply constraints have proved more severe and aretaking longer to work out than initially anticipated. Price pressures across the economycontinue to mount as a result.

Supply constraints continue to play a leading role in catching forecasters and policymakers off guard when it comes to recent inflation developments.The June FOMC meetingminutes revealed "more widespread supply constraints in product and labor markets" asa key contributor behind the upside surprise in inflation, which led offcials to significantly mark up their year-end forecasts. Forecasts for 2022 and 2023 were barely changed, however, consistent with offcials still largely viewing current inflation as temporary.

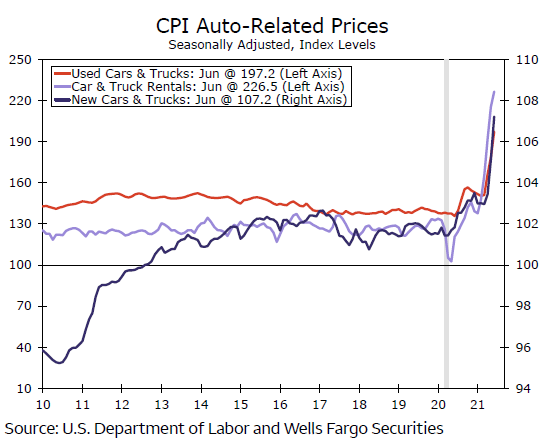

Sure, the rate of recent price gains due to supply issues in some sectors is unlikely to besustained. Autos offer the most pertinent example. U.S. auto production has declinedby 14% since February 2020 amid semiconductor shortages, putting prices well aheadof their pre-COVID price trend (Figure 1)1. At least a partial return toward Earth seemsinevitable. Even if prices stayed at current levels, the rate of change would slow to zero. Onthis basis, the Fed is at least partly right when it says that the current degree of inflation isonly temporary.

Author

Wells Fargo Research Team

Wells Fargo