The big news comes with PCE on Friday

Today the news is only the Chicago Fed January activity index and the Dallas Fed February manufacturing survey. Aside from whatever dreadful initiatives come out of Trump, the big news comes with PCE on Friday. Summary: inflation is not slowing enough to justify rate cuts, although growth is already faltering and may do the trick. We get the new Atlanta Fed GDPNow on Friday after the PCE data. It was 2.3% at the last reading in Feb 19, unchanged from Feb 14.

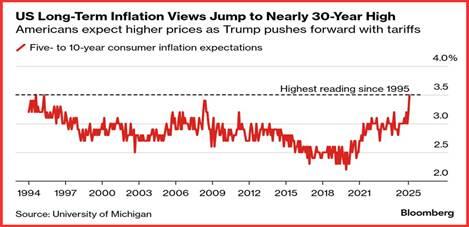

Over the weekend, TreasSec Bessent said the inflationary effects of the tariffs will be “transitory.” Where did we hear that before? Bloomberg doesn’t buy it and re-publishes the U Michigan consumer expectations chart.

Technical Question: The recent lowest low in the 10-year yield was 4.400% on Feb 5. On Friday, it was 4.406%. That is almost a match, if not a surpass. How do we interpret what comes next? If the numbers next week are consistently below 4.400%, we have to throw in the towel on a dollar recovery. We also have to acknowledge we don’t understand how inflation can be stalling and rates not rising. The term premium is nowhere to be seen, despite everybody and his brother predicting higher inflation.

If the yield stops falling and starts to creep back up, or even jump back up, that would meet the test of logic, but we would not know why—for sure. Analysts point to the prospect of slowing growth as overriding the equivalent fear of inflation.

Forecast

The dollar is teetering on the cusp of a revival, even if still down against just about everything. It’s one of those teeter-totter markets that delivers mixed signals—noise. We find it odd that the yields reflect growth instead of inflation and fear that pessimism is so rampant that the dollar continues to falter when it “should” be stronger on the idea of the Fed postponing cuts. Traders and hedgers alike should stand aside. The only two places where there is any confidence in the charts are the yen and the pound, with both escaping the Trump tariff notice. As for the CAD and peso, you just can’t buy into the firmness at all. A landslide looms.

Tidbit: We get the PCE and core PCE on Friday, Feb 28. The last reading was 2.8% y/y but notice the m/m chart fails to show the Fed’s ”durable” downward trend, no matter which version (q/q, 3-month annualized, etc.) you choose.

Whatever the mom and y/y numbers we get, there are plenty of things to worry about. The Fed likes supercore, which is sticky price CPI less food, energy, and shelter. That’s not bad, but who lives without food, energy and shelter? The BLS has a summary for January.

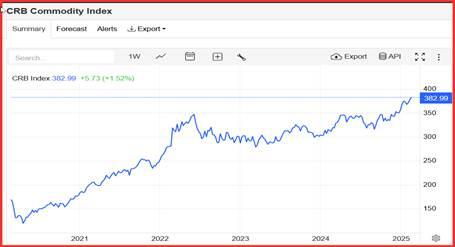

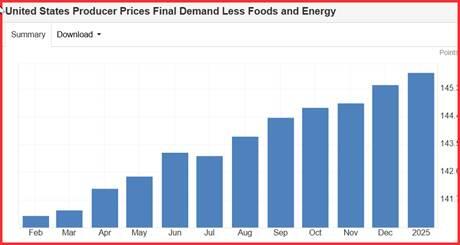

Shelter rose 7.9% y/y in Jan. Food rose 10.1% y/y in Jan. Energy fell 8.7% y/y in Jan. The net is a rise of 6.4% overall. First is commodity prices, which morph into “prices paid.” See the commodity price index chart and its cousin, producer prices.

Even if these components show a drop, inflation still stalks the land. And consider commodity prices, which morph into “prices paid.” See the commodity price index chart and its cousin, producer prices.

Can any reasonable person, including those at the Fed, honestly think inflation is falling to the extent that rate cuts are a good idea? The consumer does not see inflation falling. The only sane reason to embrace rate cuts is to get ahead of the extreme damage the tariffs are going to wreak.

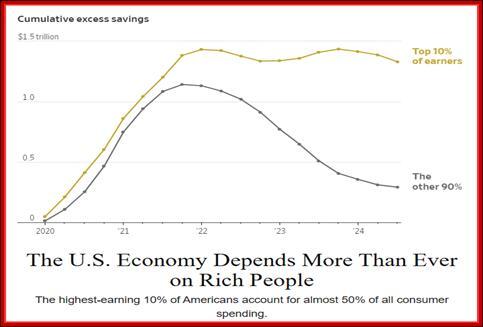

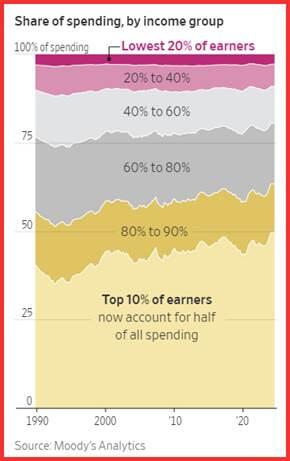

Tidbit: The front page of the digital WSJ has this dandy chart. The obvious inference—the slowdown plus inflation is going to hit the majority hard due to its lack of savings. But never mind—the rich are doing the majority of consumer spending.

“The top 10% of earners—households making about $250,000 a year or more—are splurging on everything from vacations to designer handbags, buoyed by big gains in stocks, real estate and other assets.

“Those consumers now account for 49.7% of all spending, a record in data going back to 1989, according to an analysis by Moody’s Analytics. Three decades ago, they accounted for about 36%.

“All this means that economic growth is unusually reliant on rich Americans continuing to shell out. Mark Zandi, chief economist at Moody’s Analytics, estimated that spending by the top 10% alone accounted for almost one-third of gross domestic product.

“Between September 2023 and September 2024, the high earners increased their spending by 12%. Spending by working-class and middle-class households, meanwhile, dropped over the same period.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat